Download

1 / 15

180 likes | 525 Vues

The Master Budget and Responsibility Accounting. Chapter Nine. What is a Budget?. A forecast or plan specifying how company resources will be acquired and used.

E N D

The Master Budget and Responsibility Accounting Chapter Nine ACG 2071 - Spring 2011

What is a Budget? • A forecast or plan specifying how company resources will be acquired and used Key Concept: Upper management should develop an overall strategic plan that guides and integrates the whole company and its individual budgets. Key Concept: Budgeting is a management task, not a bookkeeping task. ACG 2071 - Spring 2011

Budgets Used for Planning, Directing and Control • Planning – Developing Objectives and Goals • Directing – Day to Day Management Decisions • Control – Determining whether objectives and goals are met. Comparing actual results to budget. ACG 2071 - Spring 2011

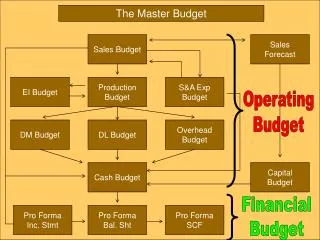

The Master Budget – Comprehensive Budget for all Phases of Operations • May Include: • Sales Budget • Production Budget • Direct Material Budget • Direct Labor Budget • Manufacturing Overhead Budget ACG 2071 - Spring 2011

The Master Budget (continued) • May Include: • Operating Expenses Budget • Capital Expenditure Budget • Cash Collections, Cash Payments, and Combined Cash Budget • Budgeted Income Statement and Balance Sheet ACG 2071 - Spring 2011

Sales Budget Sales Budget prepared first Budgets are future oriented and use estimates and forecasts Factors in sales forecasting: Prior years’ sales Economic trends (general and industry) Competitors Other ACG 2071 - Spring 2011

Production Budget Sales forecast (in units) + Projected ending inventory =Total projected production needs -Beginning inventory =Projected production in units ACG 2071 - Spring 2011

Material purchases budget Projected material required for production + Projected ending inventory of material - Projected beginning inventory of material =Quantity of material to be purchased x Purchase price =Purchases budget in dollars ACG 2071 - Spring 2011

Direct labor budget Projected production in Units x Direct Labor Hours per unit = Direct Labor hours for production X Labor Rate per hour =Projected labor cost ACG 2071 - Spring 2011

Cash Budgets Cash Collections budget: Budget must be prepared allowing for credit sales and subsequent lag in collection. Cash Payments budget: Budget must be prepared allowing for disbursements policy for accounts payable. ACG 2071 - Spring 2011

Combined Cash Budget The Cash Budget: Beginning Cash Balance xxxx Add: Budgeted Cash Collections xxxx Cash Available xxxx Less: Budgeted Cash Payments xxxx Ending Cash Balance before Financing xxxx ACG 2071 - Spring 2011

Budgeted Financial Statements • Budgeted Income Statement • Includes sales, cost of goods sold, and operating expense budget information • Budgeted Balance Sheet • Includes cash, accounts receivable, inventory, accounts payable and other budget information ACG 2071 - Spring 2011

Other Topics in Budgeting • Participative Budgeting – Middle and lower levels of management are involved in the budget process. • Zero-Based Budgeting – must justify each dollar included in budget. • Budgetary Slack – managers may overestimate expenses or underestimate revenue in budget numbers • Budget Committee – reviews and approves final budget numbers. Should include cross-section of managers ACG 2071 - Spring 2011

Responsibility accounting Responsibility Accounting – provide accounting information for areas under manager’s control to help evaluate performance Cost Center Revenue Center Profit Center Investment Center ACG 2071 - Spring 2011

Responsibility Accounting Performance Reports Performance Reports are often used as a key tool in the control function. This involves comparison of budget information with actual results to evaluate performance. Variances are differences between actual and budgeted amounts. Management by exception is a key to effective variance analysis and involves only investigating when actual results deviate significantly from budget. ACG 2071 - Spring 2011