Master Budget

Chapter Six. Master Budget. Planning – involves developing objectives and preparing various budgets to achieve these objectives. Control – involves the steps taken by management that attempt to ensure the objectives are attained. Planning and Control. Control/Evaluate Performance.

Master Budget

E N D

Presentation Transcript

Chapter Six Master Budget

Planning – involves developing objectives and preparing various budgets to achieve these objectives. Control– involves the steps taken by management that attempt to ensure the objectives are attained. Planning and Control

Control/Evaluate Performance Communicate plans Compels strategic planning Coordinate activities Means of allocating resources Motivates employees and managers Advantages of Budgeting Advantages

Choosing the Budget Period Operating Budget 2003 2004 2005 2006 The annual operating budget may be divided into quarterly or monthly budgets. A continuous budget is a 12-month budget that rolls forwardone month (or quarter) as thecurrent month (or quarter) iscompleted.

Budgeting and the Organization:Responsibility Accounting • Responsibility Center – a part, segment, or subunit of a organization whose manager is accountable for a specified set of activities, along with their revenues and/or costs • Responsibility Accounting – a system that measures the plans, budgets, actions and actual results of each Responsibility Center

Responsibility Centers Cost center Revenue center Profit center Investment center

Participative Budgeting A budget is prepared with the full cooperation andparticipation of managers at all levels. A participativebudget is also known as a self-imposed budget.

Human Factors in Budgeting Budgetary Slack: Padding the Budget People often perceive that their performance will look better in their superiors’ eyes if they can “beat the budget.”

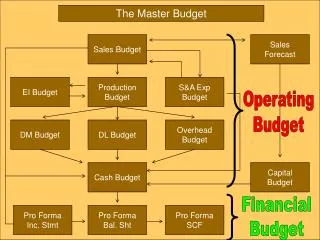

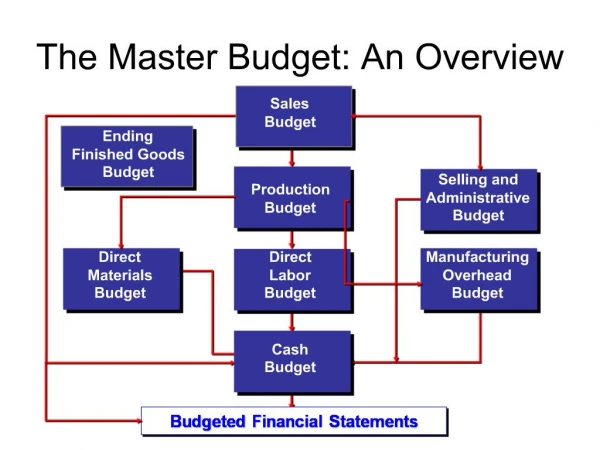

Types of Budgets Detail Budget Detail Budget Detail Budget Materials Master Budget Covering all phases of a company’s operations. Production Sales

SampleMasterBudget,Illustrated Stylistic Furniture Master Budget Example

Stylistic Furniture - Budget Details • Stylistic sells two models of granite-top coffee tables - Casual and Deluxe. Nonsales-related revenue, such as interest income, is zero. • Work-in-process inventory is negligible and is ignored. • Direct materials inventory and finished goods inventory are costed using the first-in, first-out (FIFO) method. Unit costs of direct materials purchased and unit costs of finished goods sold remain unchanged throughout each budget year but can change from year to year. • There are two types of direct materials: red oak (RO) and granite slabs (GS). Direct material costs are variable with respect to units of output - coffee tables. • Direct manufacturing labor workers are hired on an hourly basis; no overtime is worked. • There are two cost drivers for manufacturing overhead costs - direct manufacturing labor-hours and setup labor-hours.

Stylistic Furniture - Budget Details (cont) • Direct manufacturing labor-hours is the cost driver for the variable portion of manufacturing operations overhead. The fixed component of manufacturing operations overhead is tied to the manufacturing capacity of 300,000 direct manufacturing labor-hours that Stylistic has planned for 2010. • Setup labor-hours is the cost driver for the variable portion of machine setup overhead. The fixed component of machine setup overhead is tied to the setup capacity of 15,000 setup labor-hours that Stylistic has planned for 2010. • For computing inventoriable costs, Stylistic allocates all (variable and fixed) manufacturing operations overhead costs using direct manufacturing labor-hours and machine setup overhead costs using setup labor-hours. • Nonmanufacturing costs consist of product design, marketing and distribution costs. All product design costs are fixed costs for 2010. The variable component of marketing costs equals the 6.5% sales commission on revenues paid to salespeople. The variable portion of distribution costs varies with cubic feet of tables moved (Casual – 18 cu. ft. per table; Deluxe – 24 cu. ft. per table). This rate is $2 per cu. ft.

2010 Budget Data Direct materials Red Oak $ 7 per board foot (b.f.) (same as 2009) Granite $10 per square foot (s.f.) (same as 2009) Direct manufacturing labor $20 per hour

Schedule 1: Revenues Budget For the Year Ending December 31, 2010

Production Budget Total units to be sold Desired ending inventory Total units needed + = Total units needed Expected beginning inventory Units to be produced - =

Schedule 2: Production Budget (in Units) For the Year Ending December 31, 2010

Calculation of the Purchases Budget Desired ending raw material inventory Raw material needed for production Total raw material needs + = Total raw material needs Expected raw material beginning inventory Raw material to be purchased - =

Schedule 3A: Direct Material Usage Budget in Quantity and Dollars

Schedule 6A: Unit Costs of Ending Finished Goods Inventory Under the FIFO method, this unit cost is used to calculate the cost of target ending inventories of finished goods in Schedule 6B.