Download

1 / 34

610 likes | 1.77k Vues

Strategy and the Master Budget. Chapter Eight. Learning Objectives. Describe the role of budgets in the overall management process Discuss the importance of strategy and its role in the master budgeting process Provide an overview of the budgeting process

E N D

Strategy and the Master Budget Chapter Eight

Learning Objectives • Describe the role of budgets in the overall management process • Discuss the importance of strategy and its role in the master budgeting process • Provide an overview of the budgeting process • Prepare a master budget and explain the interrelationships among its supporting schedules

Learning Objectives (continued) • Identify unique budgeting characteristics of service firms, international firms, and not-for-profit organizations • Understand zero-base, activity-based, and kaizen approaches to budgeting • Discuss the application of integrated budgeting and planning tools • Discuss the role of ethics and behavioral considerations in budgeting

Basic Terminology A budget: • is a financial or nonfinancial expression of a plan of action for a specified period • identifies the resources and commitments required to achieve the organization’s goals for an upcoming period Budgeting: • The process of preparing a budget is called budgeting

Strategic Goals and Long-term Objectives • The starting point in the budget-preparation process is specification of the organization’s strategy • An organization expresses its strategic goals and long-term objectives in its capital and master budgets • Long-range planning often entails capital budgeting, which is a process for evaluating, selecting, and financing major projects, such as purchases of new factory equipment and construction of a new factory

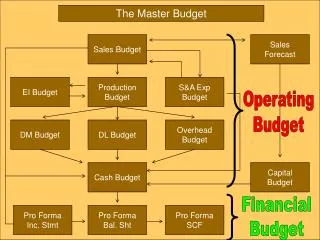

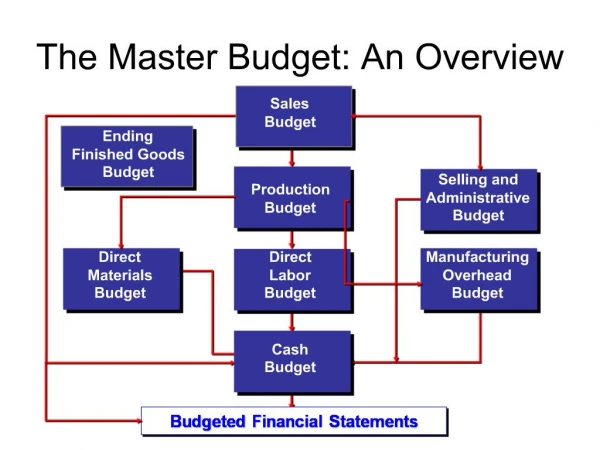

The Master Budget The master budget: • Represents the “grand plan of action” for an upcoming period • Translates the organization’s short-term objectives into action steps • Culminates in the preparation of a set of pro-forma financial statements • Communicates to employees and managers alike the expectations of top management • Helps coordinate subunit activities

The Master Budget (continued) The master budget is made up of operating and financial budgets: • Operating budgets are plans that identify resources needed to carry out the budgeted activities, such as sales and services or production • Operating budgets include production, purchase, personnel, and marketing budgets • Financial budgets identify sources and uses of funds for the budgeted operations • Financial budgets include the cash budget, budgeted statement of cash flows, the budgeted balance sheet, and the capital expenditures budget

The Budgeting Process • The budget committee is the highest authority in an organization for all matters related to the budget • Determination of the budget period: • Generally, a fiscal year with sub-period budgets prepared for each quarter or month • A continuous (rolling) budget is a budget system that has a budget for a set number of months, quarters, or years at all times–as one period ends another is added

Preparing Individual Budgets Three-step process: • Define the “bottom-line” information contained in the budget (e.g., sales for the upcoming period) • Determine what this information is a function of (e.g., budgeted unit sales, budgeted selling price/unit) • Put together information in a user-friendly way

Sales Budget The sales budget is often referred to as the cornerstone of the entire master budget The sales budget has two components: • Forecasted sales volume • Budgeted selling prices

Sales Budget (continued) Kerry Industrial Company Sales Budget For the Quarter Ended June 30, 2007 AprilMayJuneQuarter Sales in units 20,000 25,000 35,000 80,000 Selling price per unit x $30 x $30 x $30 x $30 Total sales $600,000 $750,000 $1,050,000 $2,400,000

Budgeted Budgeted Desired Beginning Production Sales Ending Inventory (in units) (in units) Inventory (in units) (in units) = + – Production Budget • After the sales budget, we prepare a production budget, which shows planned production for a given period • Budgeted production can be calculated through use of the following formula:

Production Budget (continued) • Kerry example: • Beginning inventory (April 1) = 5,000 units • Desired ending inventory (April 30th) = 30% of the following month’s projected unit sales • The sales budget has total sales for May at 25,000 units.

From the Sales Budget Production Budget (continued) Desired ending level at April 30: 30% x 25,000 units (May sales) = 7,500 units Budgeted production for April 22,500 20,000 7,500 5,000 = + – Inventory from April 1: 5,000 units

Production Budget (continued) July sales are budgeted at 40,000 units: 30% × 40,000 = 12,000 units. 30% of June’s budgeted sales

Direct Materials Budgets The direct materials usage budget: • Shows the amount (and cost) of direct materials required for budgeted production • The last line of the production budget = first line of the direct materials usage budget

Direct Materials Budgets (continued) The direct materialspurchasesbudget: • Contains budgeted purchases, in units and dollars, of direct materials for the upcoming period • Is needed to complete the direct materials usage budget (i.e., provides unit cost data) • Is a function of: materials required for production (from materials usage budget), target ending inventory of materials, beginning-of-period materials inventory, budgeted purchase price per unit of raw material

Direct Labor Budget • Enables the personnel department to plan for hiring & repositioning of employees, based on production needs • Is prepared for each class (type) of labor, e.g., skilled and semi-skilled • Is a function of: • Budgeted output (from production budget) • Standard labor hours per unit of output • Standard wage rate per hour

Direct Labor Budget (continued) • Kerry uses 0.5 hours of semiskilled labor and 0.2 hours of skilled labor per unit @ standard wage rates of $8 and $12 per hour, respectively

Direct Labor Budget: Kerry Company Each unit of output requires 0.5 hours of semi-skilled labor @ $8.00/hour, and 0.2 hours of skilled labor @ $12.00/hour 22,500 × 0.5 × $8.00 = $90,000 22,500 × 0.2 × $12.00 = $54,000

Cost of Goods Manufactured & CGS Budgets • The cost of goods manufactured and CGS budgets are prepared after the factory overhead budget is prepared • The income statement budget and the balance sheet use information from this budget

Kerry Company: Cost of Goods Manufactured & CGS Budgets, April 2007

Selling & Administrative Expense Budget The selling and general administrative expenses budget is now prepared: • This budget includes all the planned expenditures for selling and general administrative activities • Many of the expenses included in this budget are considered discretionary and are a likely place for spending cuts • Managers must be careful not to focus solely on short-term affects when making cuts in these areas (e.g., customer-service expenditures)

Cash Budget The cash budget brings together the cash effects of all budgeted activities--to ensure that the firm has adequate cash on hand: • This budget generally has three sections: • Cash available • Cash disbursements, and • Financing • Preparation of this budget involves careful review of all other budgets to identify cash inflows and outflows

Budgeted I/S and B/S The budgeted income statement (I/S) and budgeted balance sheet (B/S) can then be prepared using all the aforementioned budgets: • The budgeted I/S describes the expected operating income for the upcoming period • The budgeted B/S, the last budget in the budget-preparation process, incorporates the effects of all operations and cash flows during the budget period and shows projected ending balances in asset, liability, and equity accounts

Budgeting in Service Companies • These firms have different operating characteristics, operating environments, and considerations than those of manufacturing and merchandising firms • Service firms are different due to the absence of production or merchandise purchase budgets and their ancillary budgets–the focus of the budgeting process must be personnel planning: • Does the firm have sufficient staff and resources to provide the expected level of service output in the upcoming period? • Do staff members have the appropriate skills?

Budgeting in International Firms and Not-for-Profit (NFP) Organizations • International firms face additional challenges due to cultural and language differences, dissimilar political and legal environments, fluctuating monetary and exchange rates, and discrepancies in inflation rates of different countries • NFPs have no single bottom-line that serves as a verifiable goal in budgeting; there is no clear standard by which to measure performance • The budget shows estimated revenues and planned activities–the budget must show the organization can at least break-even

Alternative Budgeting Approaches Zero-base budgeting (ZZB) is a budgeting process that requires managers to prepare budgets from a zero base • This type of budgeting allows no activities or functions to be included in the budget unless managers can justify their needs • In-depth reviews and analyses of all budget items make managers aware of activities and functions that have outlived their usefulness • Can be a difficult and time-consuming process

Alternative Budgeting Approaches (continued) • Activity-based budgeting (ABB) is a budgeting process based on activities and cost drivers of operations: • Starts with the budgeted output and segregates costs required for the budgeted output into homogeneous cost pools • Can be a simple extension of a firm’s ABC system • Kaizen (Continuous improvement) budgeting: • Incorporates continuous improvement expectations into the budgets • Promotes active engagement in reforming and altering business practices and processes

Behavioral Issues in Budgeting • Budgetary slack, or padding the budget, is the practice of managers knowingly including a higher amount of expenditures or a lower amount of revenue in a budget • Spending the budget is another issue; managers often feel if they do not use all the resources they receive, next year’s budget may be cut • Goal congruence is a term that refers to the degree of consistency between goals of the firm, its subunits, and its employees • Involving employees in the budgeting process fosters goal congruence

Behavioral Issues in Budgeting (continued) • Difficulty levelof the budget target? • An easy budget may fail to encourage employees to give their best efforts, while a very difficult target can be discourage managers from even trying • A “highly achievable target” is suggested with incentives for exceeding the budgeted figures • Authoritative or participative budgeting? • Top-down budgeting is referred to as authoritative budgeting • Bottom-up budgeting is referred to as participative budgeting • Effective budgeting processes often combine the two types