Costs Analysis

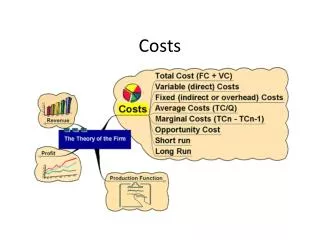

This analysis explores the distinction between fixed costs (FC) and variable costs (VC) and their impact on profitability. Fixed costs, such as rent and salaries, remain unchanged regardless of sales volume, while variable costs, like raw materials and labor, fluctuate with sales. The separation of these costs aids in determining the percentage-variable contribution margin (PVCM), showing how sales contribute to covering fixed costs and increasing profits. Additional focus is given to types of costs, methods for maintaining a low-cost position, and the concept of semi-fixed costs.

Costs Analysis

E N D

Presentation Transcript

Fixed Costs (FC) and Variable Costs (VC) • Separation into FC and VC helps to show which costs are affected by sales volume. • Fixed costs (FC) • Do not change as sales volume changes • eg rent, insurance, salaries • Variable costs (VC) • Do change as sales volume changes • eg raw material, labour, packaging

Types of Fixed Costs • Direct fixed costs • Costs incurred by specific products or services • Indirect fixed costs • Costs incurred to support the entire business

Types of Fixed Costs Continued • Two categories of indirect costs: • Traceable costs • Costs that could be allocated to various products on a non-arbitrary manner. • Eg storage space rental • Non-traceable costs • Cannot be assigned to individual products • OSH insurance • The profitability of individual products and services can be measured after separation of indirect fixed costs

Methods of Maintaining a Low-Cost Position • A no-frills product • Innovative product design • Cheaper raw materials • Innovative production processes • Low-cost distribution • Reductions in overhead

Semi-fixed Costs • Do not automatically increase as output increases. • May change if volume varies substantially. • Need more production facilitieshire more supervisors. • Increase number of phone linesmonthly rental increases

Cost of Goods Sold (aka cost of sales, COGS) • For a manufacturer • Includes fixed costs (FC) and variable costs (VC) • Retailer or Wholesaler • Includes only variable cost (VC)

Separation of Fixed Costs and Variable Costs • Enable managers to calculate percentage-variable-contribution-margin (PVCM) • PVCM shows how much of each sales dollar will be available to cover fixed costs (before BE point ) or to increase profits (after BE point), as a %.