Summary of Last Lecture

470 likes | 748 Vues

Summary of Last Lecture. WACC (Weighted Average Cost of Capital). BUSINESS RISK FACED BY FIRM, OPERATING LEVERAGE, BREAK EVEN POINT& RETURN ON EQUITY. Learning Objectives:. After going through this lecture, you would be able to have an understanding of the following topics

Summary of Last Lecture

E N D

Presentation Transcript

Summary of Last Lecture • WACC (Weighted Average Cost of Capital)

BUSINESS RISK FACED BY FIRM, OPERATING LEVERAGE, BREAK EVEN POINT&RETURN ON EQUITY

Learning Objectives: • After going through this lecture, you would be able to have an understanding of the following topics • · Business Risk faced by FIRM • · Operating Leverage (OL) • · Breakeven Point & ROE

Overview • In this lecture, we are going to continue our discussion on weighted average cost of capital and we will begin our discussion on the concept of operating leverage. Both of these concepts are of the area which we have stated in the previous lecture called capital structure.

Overview • In capital structure we decide what the distribution of debt and equity should be in the firm and it is decided by the board of directors of the firm or company. The job of deciding what amount of debt and equity one has is difficult.

Overview • So, the first thing is to calculate the cost of capital. so, the company has the option that it may either go into money market or into the capital market to raise money either through debt or through equity . Now, you might think the equity the company might raise has no cost.

Overview • We all know that when a company takes a loan it has to pay interest or mark up on it but often people think when it raise fund through equity in stock exchange then there is no cost attached to it because they are not paying any fixed rate of interest with regular intervals .

Overview • But that is mistake because there is cost attached to it in form of required rate of return which your stock holder expects to receive that and if company does not pay that then the stock holder will sell their shares and the price of the share will go down. Therefore it is important to calculate the cost of equity.

Overview • Now, let’s combine all the cost associated with the debt, preferred stock and equity and calculate the weighted average cost of capital (WACC) of company that raise capital in all three possible ways.

Example: • Suppose company ABC has equal amounts of debts, common stocks and preferred equity 1/3 each .in previous lecture, we calculated what the cost of debt was that was 11.2% then we calculated the cost of preferred equity that was 16.7%

Example: • and we also calculated the cost of common equity which was 22.7% it was the most difficult part of the WACC calculation now, it is easy because we are to apply the % of three different forms of capital.

Example: • WACC= rDxD+rExE+rPEp • =11.2 %( 1/3) +16.5 %( 1/3) +22.7 %( 1/3) • =16.9%

Example: • Now, this is over all cost for a company . What does it mean? It means that it is the average cost that company has to bear in order to use the capital of investors.

Example: • The cost of debt or bond, preferred equity and common stock this is the average of all three securities cost. It means that the company should invest in a project where the rate of return is higher than 16.9% because it should be higher than the cost that it has to pay to the investors.

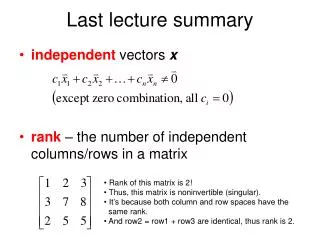

Example: • Let’s see the graph of weighted average cost of capital compared to the security market line we discussed in capital asset pricing model (CAPM).

Example: • It is important to understand this graph because it combines the market factors in the form of SML as well as the company’s internal cost in the form of WACC. It shows that what combinations of the risk & return for a particular company to invest in or not.

SML WACC Graph • The graph is a combine presentation of CAPM and WACC. It shows the expected return against the market risk or beta. In graph, the upward sloping line is SML and it is the requirement for bond and stocks in efficient markets where there are rational investors that are maintaining fully diversified portfolio and where knowledge spread very quickly through the markets.

SML WACC Graph • The risk and return combinations of all securities should lie on SML. The horizontal line is WACC which is fixed at 16.9% we have just calculated it.

SML WACC Graph • This represents required rate of return. In other words, if the company invests in any new project it should give a rate of return which is higher than 16.9% you see that the only feasible reason where that company made investment is the area which I have shown filled up with dots and this is higher then the SML and WACC.

SML WACC Graph • I have also made three crosses which represents that why will not company invest in these areas? The first cross on right side X1 is showing rate of return which is higher than WACC but lower than SML the company will not invest because it is not giving as much rate of return as efficient market is offering.

SML WACC Graph • The second cross x2 is lower than WACC and SML and cross three x3 is lower than WACC but it is on the SML again the company will not invest in these two projects or regions. • It will invest only in dots regions on these two regions the cost is higher and the return is lower.

Debt vs Equityfrom Firm’s Point of View • Remember, that it is mentioned that generally speaking companies want to keep the balance both in form of debt and equity. We have also mentioned that debt has a risk attached with it because when we have to service the regular loan mark up or interest which will eat away your income and the result will be net loss.

Debt vs Equityfrom Firm’s Point of View • You know that in income statement we deduct certain financial charges. It may be due to many reasons because the company has to serve the debt .the other reason is that if the company do not pay interest it may close down so, then why do companies take debt ?

Debt vs Equityfrom Firm’s Point of View • Issuing Debt (or Leverage) • Advantages of Issuing Debt:: • Limited fixed Interest payment - no share in profits • Limited Life Interest Payment is an Expense i.e. Tax Deductible • Can Improve (or Amplify) the Return on Equity (ROE)

Debt vs Equityfrom Firm’s Point of View • Disadvantages: • Debt adds to Company-specific Risk • If company doesn’t pay Interest, it can be closed down

Debt vs Equityfrom Firm’s Point of View • Issuing Equity (generally Common Equity or Ownership) • Advantages of Issuing Equity: • Not required to pay fixed regular Dividends • Capital Structure is a Firm’s Mix of Debt & Equity

Debt vs Equityfrom Firm’s Point of View • Risks Faced by Firm: • Total Stand-Alone Risk of a Stock (from Risk and CAPM Theory): • Stock’s Total Stand Alone Risk = Diversifiable + Market • Company-specific Risk: Unique, Diversifiable • Market Risk: Systematic, Not Diversifiable

Debt vs Equityfrom Firm’s Point of View • Total Stand-Alone Risk of a FIRM (New) • Firm’s Total Stand Alone Risk = Business + Financial • Business Risk: • It is defined as the Risk of All Assets & Operations (without debt). Includes both • Company-Specific (and Diversifiable) & Market Risks.

Debt vs Equityfrom Firm’s Point of View • Financial Risk: • Additional Risk faced by Common Stockholders if Firm takes Debt. It is a pure debt related Risk.

Financial Risk (Investor’s Point of View): • Suppose firm ABC had a Capital Structure of 100% Common Equity. Then the Management and Board of Directors of firm ABC then decide to reduce half of the equity and take a loan (or Debt) instead. This affects the distribution of risk & return to the common equity holders (or Owners).

Financial Risk (Investor’s Point of View): • In other words, the Management of firm ABC has added a new kind of investor. The debt holder faces almost no risk because he is “guaranteed” the Interest payment at all costs whether or not the firm is making profit or whether or not the equity owners are paid dividend.

Financial Risk (Investor’s Point of View): • Debt holders eat away at the owners’ (or equity holders’) money at almost no risk. So, naturally, the risk faced by equity holders increases because same Business Risk is now shouldered by fewer Equity Shares.

Firm’s Total Stand Alone Risk (Uncertainty in ROA & ROE): • Firm’s Total Stand Alone Risk measured by the Uncertainty or Fluctuations in Possible outcomes for Firm’s Future overall ROR.

If Business has Debt & Equity (i.e. levered firm): • Firm’s Overall ROR = ROA = Return on Assets = Return to Investors / Assets = (Net Income + Interest) / Total Assets Note: Total Assets = Total Liabilities = Debt + Equity

If Business is 100% Equity (or un-levered firm) • No Debt and No Interest. • Firm’s Overall ROR = Net Income / Total Assets. For 100% Equity Firm, Total Assets = Equity. So Overall ROR = Net Income / Equity = ROE! • Note: Net Income is also called Earnings. • Note: ROE does not equal rE (Required Rate of Return). ROE is Expected book return on Equity.

If Business is 100% Equity (or un-levered firm) • Used in Stock Valuation Formula to calculate “g” & “PVGO” • Fluctuations in ROE = “Basic Business Risk” • You should review Financial Accounting Ratios for better understanding of the above mentioned concepts.

If Business is 100% Equity (or un-levered firm) • Basic Business Risk (Not Considering Debt): • Causes of High “Basic Business Risk” or Uncertainty or Volatility or “Instability” or “Shocks” • Large changes in Customers’ Demand (seasonality) • Unstable Selling Price (unstable markets and retailers) • Uncertainty in Input Costs (raw material, labor, utilities)

If Business is 100% Equity (or un-levered firm) • Inability of Management to Change Operational Tactics and Strategy to Meet Changing Environment • Ineffective Price Stabilization • Poor Product R&D and Planning • High Operating Leverage (OL) • Many other causes

Operating Leverage (OL): • Formula = Fixed Costs / Total Costs • Concept: High OL Increases Risk: Customer Demand Falls but Fixed Costs remain high. So, Small Decline in Sales Can Cause Large Decline in ROE.

Operating Leverage (OL): • In financial management the term leverage refers to the little change in the amount of sales or quantity of sale that will affect the over all earning of the company . • Operating leverage (OL) =FIXED COSTS /TOTAL COSTS

Operating Leverage (OL): • A company supposes has operating leverage of suppose 50% or 0.5 it is considered to a high leverage. Generally, it is more risky for a firm and the fixed cost does not change. So, the companies that has high leverage are considered to be more risky.

Operating Leverage (OL): • Now, the companies have to hire the skilled people and technicians specially ,in the capital intensive industries . Now, let’s talk about the operating leverage .

Operating Leverage (OL): • Let’s take the example of cement industry there are two ways of technology if you want to set a cement plant one is the old technology and the other is drying process new technology .these two types have different costs.

Operating Leverage (OL): • We have learnt that NPV formula is best for investment decisions in which discount rate r is used which is the required rate of return .

Operating Leverage (OL): • When OL associated with a firm is higher then the risk also becomes higher .we need to understand the impact of operating leverage both numerically ,and graphically .please go over the concepts of WACC and NPV.

Summary • · Business Risk faced by FIRM • · Operating Leverage (OL) • · Breakeven Point & ROE