Download

1 / 74

750 likes | 785 Vues

Explore new approaches to credit risk measurement, bankruptcy trends, disintermediation, and technology in financial institutions. Learn about credit derivatives, BIS risk-based capital requirements, and more. Dive into traditional and expert systems for credit risk evaluation.

E N D

“A bank is a place that will lend you money if you can prove that you don’t need it.” Bob Hope Saunders & Cornett, Financial Institutions Management, 4th ed.

Why New Approaches to Credit Risk Measurement and Management? Why Now? Saunders & Cornett, Financial Institutions Management, 4th ed.

Structural Increase in Bankruptcy • Increase in probability of default • High yield default rates: 5.1% (2000), 4.3% (1999, 1.9% (1998). Source: Fitch 3/19/01 • Historical Default Rates: 6.92% (3Q2001), 5.065% (2000), 4.147% (1999), 1998 (1.603%), 1997 (1.252%), 10.273% (1991), 10.14% (1990). Source: Altman • Increase in Loss Given Default (LGD) • First half of 2001 defaulted telecom junk bonds recovered average 12 cents per $1 ($0.25 in 1999-2000) • Only 9 AAA Firms in US: Merck, Bristol-Myers, Squibb, GE, Exxon Mobil, Berkshire Hathaway, AIG, J&J, Pfizer, UPS. Late 70s: 58 firms. Early 90s: 22 firms. Saunders & Cornett, Financial Institutions Management, 4th ed.

Disintermediation • Direct Access to Credit Markets • 20,000 US companies have access to US commercial paper market. • Junk Bonds, Private Placements. • “Winner’s Curse” – Banks make loans to borrowers without access to credit markets. Saunders & Cornett, Financial Institutions Management, 4th ed.

More Competitive Margins • Worsening of the risk-return tradeoff • Interest Margins (Spreads) have declined • Ex: Secondary Loan Market: Largest mutual funds investing in bank loans (Eaton Vance Prime Rate Reserves, Van Kampen Prime Rate Income, Franklin Floating Rate, MSDW Prime Income Trust): 5-year average returns 5.45% and 6/30/00-6/30/01 returns of only 2.67% • Average Quality of Loans have deteriorated • The loan mutual funds have written down loan value Saunders & Cornett, Financial Institutions Management, 4th ed.

The Growth of Off-Balance Sheet Derivatives • Total on-balance sheet assets for all US banks = $5 trillion (Dec. 2000) and for all Euro banks = $13 trillion. • Value of non-government debt & bond markets worldwide = $12 trillion. • Global Derivatives Markets > $84 trillion. • All derivatives have credit exposure. • Credit Derivatives. Saunders & Cornett, Financial Institutions Management, 4th ed.

Declining and Volatile Values of Collateral • Worldwide deflation in real asset prices. • Ex: Japan and Switzerland • Lending based on intangibles – ex. Enron. Saunders & Cornett, Financial Institutions Management, 4th ed.

Technology • Computer Information Technology • Models use Monte Carlo Simulations that are computationally intensive • Databases • Commercial Databases such as Loan Pricing Corporation • ISDA/IIF Survey: internal databases exist to measure credit risk on commercial, retail, mortgage loans. Not emerging market debt. Saunders & Cornett, Financial Institutions Management, 4th ed.

BIS Risk-Based Capital Requirements • BIS I: Introduced risk-based capital using 8% “one size fits all” capital charge. • Market Risk Amendment: Allowed internal models to measure VAR for tradable instruments & portfolio correlations – the “1 bad day in 100” standard. • Proposed New Capital Accord BIS II – Links capital charges to external credit ratings or internal model of credit risk. To be implemented in 2005. Saunders & Cornett, Financial Institutions Management, 4th ed.

Traditional Approaches to Credit Risk Measurement 20 years of modeling history Saunders & Cornett, Financial Institutions Management, 4th ed.

Expert Systems – The 5 Cs • Character – reputation, repayment history • Capital – equity contribution, leverage. • Capacity – Earnings volatility. • Collateral – Seniority, market value & volatility of MV of collateral. • Cycle – Economic conditions. • 1990-91 recession default rates >10%, 1992-1999: < 3% p.a. Altman & Saunders (2001) • Non-monotonic relationship between interest rates & excess returns. Stiglitz-Weiss adverse selection & risk shifting. Saunders & Cornett, Financial Institutions Management, 4th ed.

Problems with Expert Systems • Consistency • Across borrower. “Good” customers are likely to be treated more leniently. “A rolling loan gathers no loss.” • Across expert loan officer. Loan review committees try to set standards, but still may vary. • Dispersion in accuracy across 43 loan officers evaluating 60 loans: accuracy rate ranged from 27-50. Libby (1975), Libby, Trotman & Zimmer (1987). • Subjectivity • What are the optimal weights to assign to each factor? Saunders & Cornett, Financial Institutions Management, 4th ed.

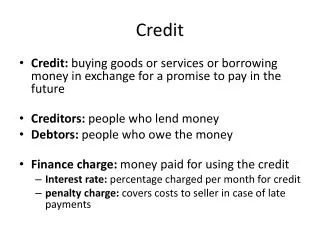

Credit Scoring Models • Linear Probability Model • Logit Model • Probit Model • Discriminant Analysis Model • 97% of banks use to approve credit card applications, 70% for small business lending, but only 8% of small banks (<$5 billion in assets) use for small business loans. Mester (1997). Saunders & Cornett, Financial Institutions Management, 4th ed.

Linear Discriminant Analysis – The Altman Z-Score Model • Z-score (probability of default) is a function of: • Working capital/total assets ratio (1.2) • Retained earnings/assets (1.4) • EBIT/Assets ratio (3.3) • Market Value of Equity/Book Value of Debt (0.6) • Sales/Total Assets (1.0) • Critical Value: 1.81 Saunders & Cornett, Financial Institutions Management, 4th ed.

Problems with Credit Scoring • Assumes linearity. • Based on historical accounting ratios, not market values (with exception of market to book ratio). • Not responsive to changing market conditions. • 56% of the 33 banks that used credit scoring for credit card applications failed to predict loan quality problems. Mester (1998). • Lack of grounding in economic theory. Saunders & Cornett, Financial Institutions Management, 4th ed.

The Option Theoretic Model of Credit Risk Measurement Based on Merton (1974) KMV Proprietary Model Saunders & Cornett, Financial Institutions Management, 4th ed.

The Link Between Loans and Optionality: Merton (1974) • Figure 4.1: Payoff on pure discount bank loan with face value=0B secured by firm asset value. • Firm owners repay loan if asset value (upon loan maturity) exceeds 0B (eg., 0A2). Bank receives full principal + interest payment. • If asset value < 0B then default. Bank receives assets. Saunders & Cornett, Financial Institutions Management, 4th ed.

Using Option Valuation Models to Value Loans • Figure 4.1 loan payoff = Figure 4.2 payoff to the writer of a put option on a stock. • Value of put option on stock = equation (4.1) = f(S, X, r, , ) where S=stock price, X=exercise price, r=risk-free rate, =equity volatility,=time to maturity. Value of default option on risky loan = equation (4.2) = f(A, B, r, A, ) where A=market value of assets, B=face value of debt, r=risk-free rate, A=asset volatility,=time to debt maturity. Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Problem with Equation (4.2) • A andAare not observable. • Model equity as a call option on a firm. (Figure 4.3) • Equity valuation = equation (4.3) = E = h(A, A, B, r, ) Need another equation to solve for A andA: E = g(A) Equation (4.4) Can solve for A andA with equations (4.3) and (4.4) to obtain a Distance to Default = (A-B)/A Figure 4.4 Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Merton’s Theoretical PD • Assumes assets are normally distributed. • Example: Assets=$100m, Debt=$80m, A=$10m • Distance to Default = (100-80)/10 = 2 std. dev. • There is a 2.5% probability that normally distributed assets increase (fall) by more than 2 standard deviations from mean. So theoretical PD = 2.5%. • But, asset values are not normally distributed. Fat tails and skewed distribution (limited upside gain). Saunders & Cornett, Financial Institutions Management, 4th ed.

Merton’s Bond Valuation Model • B=$100,000, =1 year, =12%, r=5%, leverage ratio (d)=90% • Substituting in Merton’s option valuation expression: • The current market value of the risky loan is $93,866.18 • The required risk premium = 1.33% Saunders & Cornett, Financial Institutions Management, 4th ed.

KMV’s Empirical EDF • Utilize database of historical defaults to calculate empirical PD (called EDF): • Fig. 4.5 Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Accuracy of KMV EDFsComparison to External Credit Ratings • Enron (Figure 4.8) • Comdisco (Figure 4.6) • USG Corp. (Figure 4.7) • Power Curve (Figure 4.9): Deny credit to the bottom 20% of all rankings: Type 1 error on KMV EDF = 16%; Type 1 error on S&P/Moody’s obligor-level ratings=22%; Type 1 error on issue-specific rating=35%. Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Monthly EDF™ credit measure Agency Rating Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Problems with KMV EDF • Not risk-neutral PD: Understates PD since includes an asset expected return > risk-free rate. • Use CAPM to remove risk-adjusted rate of return. Derives risk-neutral EDF (denoted QDF). Bohn (2000). • Static model – assumes that leverage is unchanged. Mueller (2000) and Collin-Dufresne and Goldstein (2001) model leverage changes. • Does not distinguish between different types of debt – seniority, collateral, covenants, convertibility. Leland (1994), Anderson, Sundaresan and Tychon (1996) and Mella-Barral and Perraudin (1997) consider debt renegotiations and other frictions. • Suggests that credit spreads should tend to zero as time to maturity approaches zero. Duffie and Lando (2001) incomplete information model. Zhou (2001) jump diffusion model. Saunders & Cornett, Financial Institutions Management, 4th ed.

Term Structure Derivation of Credit Risk Measures Reduced Form Models: KPMG’s Loan Analysis System and Kamakura’s Risk Manager Saunders & Cornett, Financial Institutions Management, 4th ed.

Estimating PD: An Alternative Approach • Merton’s OPM took a structural approach to modeling default: default occurs when the market value of assets fall below debt value • Reduced form models: Decompose risky debt prices to estimate the stochastic default intensity function. No structural explanation of why default occurs. Saunders & Cornett, Financial Institutions Management, 4th ed.

A Discrete Example:Deriving Risk-Neutral Probabilities of Default • B rated $100 face value, zero-coupon debt security with 1 year until maturity and fixed LGD=100%. Risk-free spot rate = 8% p.a. • Security P = 87.96 = [100(1-PD)]/1.08 Solving (5.1), PD=5% p.a. • Alternatively, 87.96 = 100/(1+y) where y is the risk-adjusted rate of return. Solving (5.2), y=13.69% p.a. • (1+r) = (1-PD)(1+y) or 1.08=(1-.05)(1.1369) Saunders & Cornett, Financial Institutions Management, 4th ed.

Multiyear PD Using Forward Rates • Using the expectations hypothesis, the yield curves in Figure 5.1 can be decomposed: • (1+0y2)2 = (1+0y1)(1+1y1) or 1.162=1.1369(1+1y1) 1y1=18.36% p.a. • (1+0r2)2 = (1+0r1)(1+1r1) or 1.102=1.08(1+1r1) 1r1=12.04% p.a. • One year forward PD=5.34% p.a. from: (1+r) = (1- PD)(1+y) 1.1204=1.1836(1 – PD) • Cumulative PD = 1 – [(1 - PD1)(1 – PD2)] = 1 – [(1-.05)(1-.0534)] = 10.07% Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

The Loss Intensity Process • Expected Losses (EL) = PD x LGD • If LGD is not fixed at 100% then: (1 + r) = [1 - (PDxLGD)](1 + y) Identification problem: cannot disentangle PD from LGD. Saunders & Cornett, Financial Institutions Management, 4th ed.

Disentangling PD from LGD • Intensity-based models specify stochastic functional form for PD. • Jarrow & Turnbull (1995): Fixed LGD, exponentially distributed default process. • Das & Tufano (1995): LGD proportional to bond values. • Jarrow, Lando & Turnbull (1997): LGD proportional to debt obligations. • Duffie & Singleton (1999): LGD and PD functions of economic conditions • Unal, Madan & Guntay (2001): LGD a function of debt seniority. • Jarrow (2001): LGD determined using equity prices. Saunders & Cornett, Financial Institutions Management, 4th ed.

KPMG’s Loan Analysis System • Uses risk-neutral pricing grid to mark-to-market • Backward recursive iterative solution – Figure 5.2. • Example: Consider a $100 2 year zero coupon loan with LGD=100% and yield curves from Figure 5.1. • Year 1 Node (Figure 5.3): • Valuation at B rating = $84.79 =.94(100/1.1204) + .01(100/1.1204) + .05(0) • Valuation at A rating = $88.95 = .94(100/1.1204) +.0566(100/1.1204) + .0034(0) • Year 0 Node = $74.62 = .94(84.79/1.08) + .01(88.95/1.08) • Calculating a credit spread: 74.62 = 100/[(1.08+CS)(1.1204+CS)] to get CS=5.8% p.a. Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Noisy Risky Debt Prices • US corporate bond market is much larger than equity market, but less transparent • Interdealer market not competitive – large spreads and infrequent trading: Saunders, Srinivasan & Walter (2002) • Noisy prices: Hancock & Kwast (2001) • More noise in senior than subordinated issues: Bohn (1999) • In addition to credit spreads, bond yields include: • Liquidity premium • Embedded options • Tax considerations and administrative costs of holding risky debt Saunders & Cornett, Financial Institutions Management, 4th ed.

Mortality Rate Derivation of Credit Risk Measures The Insurance Approach: Mortality Models and the CSFP Credit Risk Plus Model Saunders & Cornett, Financial Institutions Management, 4th ed.

Mortality Analysis • Marginal Mortality Rates = (total value of B-rated bonds defaulting in yr 1 of issue)/(total value of B-rated bonds in yr 1 of issue). • Do for each year of issue. • Weighted Average MMR = MMRi = tMMRt x w where w is the size weight for each year t. Saunders & Cornett, Financial Institutions Management, 4th ed.

Mortality Rates - Table 11.10 • Cumulative Mortality Rates (CMR) are calculated as: • MMRi = 1 – SRi where SRi is the survival rate defined as 1-MMRi in ith year of issue. • CMRT = 1 – (SR1 x SR2 x…x SRT) over the T years of calculation. • Standard deviation = [MMRi(1-MMRi)/n] As the number of bonds in the sample n increases, the standard error falls. Can calculate the number of observations needed to reduce error rate to say std. dev.= .001 • No. of obs. = MMRi(1-MMRi)/2 = (.01)(.99)/(.001)2 = 9,900 Saunders & Cornett, Financial Institutions Management, 4th ed.

CSFP Credit Risk Plus Appendix 11B • Default mode model • CreditMetrics: default probability is discrete (from transition matrix). In CreditRisk +, default is a continuous variable with a probability distribution. • Default probabilities are independent across loans. • Loan portfolio’s default probability follows a Poisson distribution. See Fig.8.1. • Variance of PD = mean default rate. • Loss severity (LGD) is also stochastic in Credit Risk +. Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Saunders & Cornett, Financial Institutions Management, 4th ed.

Distribution of Losses • Combine default frequency and loss severity to obtain a loss distribution. Figure 8.3. • Loss distribution is close to normal, but with fatter tails. • Mean default rate of loan portfolio equals its variance. (property of Poisson distrib.) Saunders & Cornett, Financial Institutions Management, 4th ed.