Forecasting Exchange Rates

Forecasting Exchange Rates. Forecasting Techniques: The Role of the Efficient Market (and Market Based Forecasting Models. Fundamental and Technical Analysis. Initial Observation.

Forecasting Exchange Rates

E N D

Presentation Transcript

Forecasting Exchange Rates Forecasting Techniques: The Role of the Efficient Market (and Market Based Forecasting Models. Fundamental and Technical Analysis.

Initial Observation • Since demise of the Bretton Woods “fixed exchange rate” regime in the early 1970s and the resulting move towards more flexible exchange rates, the need to forecast exchange rates has: • (1) become more important and • (2) probably more difficult.

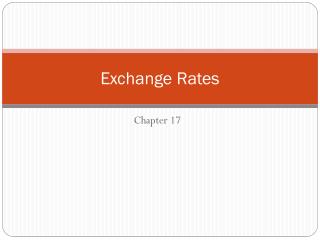

Pound and Yen During Bretton Woods Pound Sterling Japanese Yen

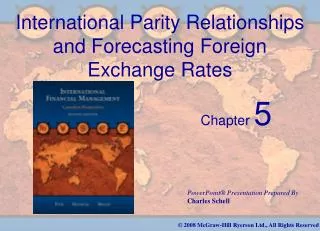

Pound and Yen Post Bretton Woods Pound Sterling Japanese Yen

Why Is There a Need to Forecast? • Multinational Business Firms: • Hedging decisions (managing foreign exchange exposures) • Financing decisions (where to raise long term capital) • Capital budgeting decisions (FDI locations) • Profit remittance decisions (when and where to move profits) • Short term financing decisions (managing idle cash) • Global Investors: • Constructing appropriate portfolios

Three FX Forecasting Approaches • Efficient Market Approach • This model assumes that today’s spot exchange rate fully captures all relevant pricing information. • Technical Approach • These models assume that charts depicting historical movements in spot rates are useful in predicting future moves in spot rates. • Fundamental Approach • These models focus on macroeconomic variables and government policies that are likely to influence a currency’s future spot rate. These models can be divided into two sub groups: • Non-parity models: Look at demand and supply pressures. • Asset Choice, Balance of Payments, etc. • Parity models: Estimate equilibrium prices through economic based formulas. • These models were the subject of previous lectures.

Efficient Market Approach • Efficient Market Model postulates that foreign exchange markets are efficient if: • All relevant pricing information is quickly incorporated into current spot exchange rates; this information includes: • Current (i.e., new) financial, economic, and political information/data, and • Historical financial, economic, and political information/data, and • Expectations regarding these variables (i.e., expectations for the future). • Thus the spot rate includes what it knows and what it thinks it knows about the future. • Based on this information, the foreign exchange market is making its best estimate (optimal forecast) as to the spot rate.

Efficient Markets and Forecasting • If foreign exchange markets are efficient and current spot rates reflect, historical and current information along with expectations for the future, then changes in spot exchange rates will only occur when the market receives information it did not expect (a “surprise”). • However, unexpected information is unpredictable and probably random. • And when surprises do happen, the spot rate will adjust quickly. • Issue for forecasting: Since we can’t anticipate unexpected information, how can we forecast spot exchange rates?

Efficient Market (EM) Forecasting • Issue: What can advocates of the efficient market use to forecast future spot rates? • They use “market based” models: • Either the current spot rateor • The current forward rate to forecast the future spot rate. • Assumes that a market based forecast is as good as any since you can’t anticipate unanticipated information. • These models also assume “unbiased predictor errors,” or specifically • Forecasting errors should net out to zero over time.

Empirical Tests of Market Based Models • (1) Comparing market based models: • Question: Do forward rate models and the spot rate models produce the same forecasting results? • Agmon and Amihud (1981) found that one forecasting method was not better than the other. • (2) Testing market based models for “unbiased predictors” of future spot rates. • Done through studies which examine market based forecasts in relation to a “Perfect Forecast Line.” • Test: Are the forecasts consistently above or below the actual (realized) spot rates? • Studies suggest that market based approaches over long periods of time produce cumulative errors approaching zero.

Market Based Models Over the Short Term • Even if we assume that market based models produce unbiased results over the long term, that is not the same thing as saying that they may not produce large errors over the short term. • Questions: • Are there short term errors? • If so, how large?

Market Based Forecasting Errors • Use the following formulas for American Terms Quotations: • Absolute forecast error = (Forecast Rate – Actual Rate) /Actual Rate • British Pound Example: • Current 30 day forward = $1.5800 (Forecast) • Current Spot rate = $1.6100 (Forecast) • Actual spot in 30 days = $1.5900 (Actual) • Forward Market Based Model Error: • ($1.5800 – 1.5900)/1.5900= -0.01/1.5900 = -0.63% • The forecast (1.58) underestimated the actual (1.59) by 0.63% • Current Spot Market Based Model Error: • ($1.6100 – 1.5900)/1.5900 = +0.02/1.5900 = +1.26% • The forecast (1.61) overestimated the actual (1.59) by 1.26%

Current Spot Market Based Model Errors: 30 Day Forecast of the Pound

Current Spot Market Based Model Errors: 30 Day Forecast of the Pound

Market Based Forecasting Errors • Use the following formulas for European Terms Quotations: • Absolute forecast error = (Actual Rate – Forecast Rate) /Actual Rate • Yen Example: • Current 30 day forward = 81.00 (Forecast) • Current Spot rate = 83.75 (Forecast) • Actual spot in 30 days = 82.00 (Actual) • Forward Market Based Model Error: • (82.00 – 81.00)/82.00= 1.00/82.00 = 1.22% • The forecast (81) overestimated the actual (82) by 1.22% • Current Spot Market Based Model Error: • (82.00 - 83.75)/82.00 = -1.75/82.00 = -2.13% • The forecast (83.75) underestimated the actual (82) by 2.13%

Current Spot Market Based Model Errors: 30 Day Forecast of the Yen

Current Spot Market Based Model Errors: 30 Day Forecast of the Yen

Spot Market Based Forecast: Summary Pound Yen Daily Data: N = 933 Mean error: -1.14% Standard Deviation: 3.72% Range: +13.13% to -13.21% Monthly Data: N = 130 Mean error: - 0.18% Standard Deviation: 2.33% Range: +5.46% to – 6.22% • Daily Data: • N = 933 • Mean error: +0.79% • Standard Deviation: 4.53% • Range: +20.30% to -12.00% • Monthly Data: • N = 130 • Mean error: -0.01% • Standard Deviation: 2.36% • Range: +9.04% to – 6.02%

Summary: Efficient Markets (i.e., Market Based Models) • Advantages of market based models: • Easy to use: data are readily observable. • Costless to use: data are “free.” • Disadvantages of market based models: • Conceptual: Models don’t force us to think about forces which may account for future moves in exchange rates. • Even if we assume these models provide long term unbiased predictors, there are times, especially over the short run, when they may produce large single period forecasting errors. • Implications for Global Firms and Global Investors: Use with caution, given the potential for large short term forecasting errors .

Technical Analysis • The second approach used to forecast exchange rates is called technical analysis. • Technical analysis uses historical foreign exchange price data to predict future prices. • Specifically, this approach looks for the formation of specific patterns of spot rate prices, which may signal future moves in spot rates. • Approach relies heavily on charts (and computers) and thus is sometimes called a “chartist” approach.

Assumptions and Use of Technical Analysis • Question: Why does technical analysis assume that past price patterns can be used to signal future moves in foreign exchange spot rates? • Technical analysis argues that spot prices are not random and that patterns will develop. • Furthermore, these patterns can be used to predict future moves in exchange rates (i.e., they repeat). • Technical analysis focuses on very short term forecasting (within a trading day out to a couple of weeks or months). • Thus, this approach is not useful for global companies concerned with longer term currency moves (e.g., over a year, or longer). • This approach is used by currency traders.

Technical Analysis Approaches • Today, there are many technical approaches to chose from. Among these are: • Moving Average Cross Over Technique • Bollinger Band Analysis Technique • We will examine these two approaches in the slides which follow. • For a more complete and current discussion of technical analysis and technical signals see: • http://www.fxstreet.com/technical/

Moving Average Cross Over Strategy • The Moving Average Cross Over Strategy compares a currency’s current spot rate to some longer term moving average of past spot rates. • Strategy looks for crossovers of the two series and uses the following rules: • When current spot crosses its trend on way up, this signals future currency strength. • Trading strategy: Buy long. • When current spot crosses its trend on way down, this signals future currency weakness. • Trading strategy: Sell short

Bollinger Band Analysis • Bollinger Band Analysis is a technique which examines a currency’s spot price in relation to pre-determined upper and lower trading bands. • This technique first calculates the currency's simple moving average of the currency’s spot rates over some historical period (this is called the SMA). • Then two bands are calculated about this moving average: • 1. An upper band of the historical spot rates (which is plus 2 standard deviations from the SMA) • 2. A lower band of the historical spot rates (which is minus 2 standard deviations from the SMA)

Using the Bollinger Bands • Technique assumes that the tendency of a currency is to trade within the upper and lower band. • Movement outside of the band produces the following 2 signals: • (1) When spot prices move above the upper band (i.e., above plus 2 standard deviations), the signal is the currency is overbought. • This is a technical signal of future weakness. • Trading strategy: Sell short • (2 When spot prices move below the lower band (i.e. below minus 2 standard deviations) the signal is the currency is oversold. • This is a signal of future strength in currency. • Trading strategy: Buy long.

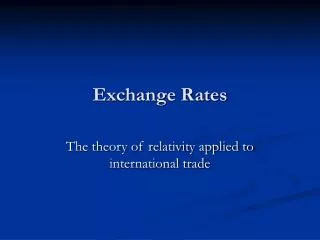

British Pound: Bollinger Bands Around 90-day Moving Average, January 2007 – Sept 2007

Sources for Technical Analysis Charts • http://fx.sauder.ubc.ca/ • http://www.fxstreet.com/index.asp • http://www.saxobank.com/?ID=101 • Subscription required.

Appendix 1: More on the Efficient Market Hypothesis The following slides discuss the three possible forms of FX market efficiency and their implications for forecasting. These slides also cover some of the studies of FX market efficiency as they apply to developed and developing countries.

Three Possible Forms of Foreign Exchange Market Efficiency? • There are three possible forms of Foreign Exchange market efficiency, they are: • Strong-Form Efficiency: All information, public and private (including insider information) is reflected in current spot exchange rates. • Semi-Strong Efficiency: All publicly available information is reflected in current spot exchange rates. • Weak-Form Efficiency: All past price and past volume information is reflected in current spot exchange rates. • It is named weak form because prices are the most publicly and easily accessible pieces of information. • The information contained in the past sequence of prices of a spot exchange rate is fully reflected in the current spot exchange rate.

Degree of Market Efficiency and Forecasting Exchange Rates • The “degree of efficiency” of the foreign exchange markets also has implications for forecasting future spot rates. • Weak Form: Current spot rates reflect all past spot rates. • The information contained in the past sequence of spot rates is fully reflected in the current spot rate. • Technical analysis (using historical charts to forecast) is useless. • Semi-strong Form: Current spot exchange rates reflect all publicly available information (such as interest rates, balance of payments, inflation, etc.) • Changes in the spot rate will only occur in response to unpredictable news in the future. • Strong Form: Current spot exchange rates reflect all publicly available information and all private information. • Assumes even if you had insider information, you could not predict spot changes in the future.

Testing The Efficiency of FX Markets • Tests of the foreign exchange markets in developed countries generally conclude that they are weak form and semi-strong-efficient. • The market is assumed to be semi-strong, if prices adjust quickly to publicly available information (Eugene Fama, 1970). For an interview with Eugene Fama see: • http://www.dfaus.com/library/reprints/interview_fama_tanous/ • Studies of developed countries suggest that “unanticipated” news has been a major determinant of exchange rate moves. • Frenkel, 1981 and Cosset, 1985

Testing The Efficiency of Markets • Tests of foreign exchange markets in developing countries, however, provide mixed results, some supporting weak form, but not semi strong efficiency. These studies include: • Masih and Masih, 1996 • Sarwa, 1997 • Ayogu, 1997 • Los, 1999 • Wickremasinghe, 2004 • Thus, in developing countries these currencies may not react quickly to new information as it becomes available.