Uploaded by

meara

0 SLIDES

166 VUES

0LIKES

Exchange Rates

DESCRIPTION

Exchange Rates. Chapter 17. Currency Markets and Exchange Rates. People need foreign currencies to make two kinds of transactions One is purchases of goods and services from other countries. The other is purchases of foreign assets, or capital outflows. The Trading Process.

Download

1 / 0

Download Presentation

Télécharger la présentation

Exchange Rates

An Image/Link below is provided (as is) to download presentation

Download Policy: Content on the Website is provided to you AS IS for your information and personal use and may not be sold / licensed / shared on other websites without getting consent from its author.

Content is provided to you AS IS for your information and personal use only.

Download presentation by click this link.

While downloading, if for some reason you are not able to download a presentation, the publisher may have deleted the file from their server.

During download, if you can't get a presentation, the file might be deleted by the publisher.

E N D

Presentation Transcript

-

Exchange Rates

Chapter 17 - Currency Markets and Exchange Rates People need foreign currencies to make two kinds of transactions One is purchases of goods and services from other countries. The other is purchases of foreign assets, or capital outflows.

- The Trading Process The Interbank Market Participants are large banks (commercial and investment). These banks are dealers, trading currencies for themselves, and also act as brokers for companies and individuals. The minimum denomination for trades is $1 million worth of currency. Two big OTC networks: Reuters, and Electronic Broking Services (EBS) These are exchanges of bank deposits

- The Trading Process (cont’d) The Retail Market You buy euros using your account at a large bank, or if you don’t have an account, your small bank buys euros from its account at a large bank Your Week in Paris Small-scale currency markets ATMs and credit cards

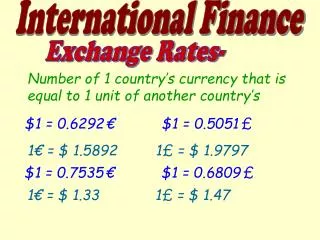

- Measuring Exchange Rates A nominal exchange rate can be expressed as the price of either currency in terms of the other. By convention, it is expressed as the amount of a foreign currency that buys one unit of the local currency. An appreciation of a currency is a rise in its price in terms of foreign currency. This is also called a currency getting “stronger”. Depreciation is a currency getting “weaker” in the sense that it takes less foreign currency to buy one unit of local currency.

- Why Exchange Rates Matter – Effects of Appreciation Cheaper Imports – If the dollar appreciates against the Euro, European goods and services become less expensive for American consumers. Lower Sales for Domestic Firms – two types of firms are hurt Import-competing firms (e.g., Washington wine makers) Exporting firms Losses to holders of foreign assets An appreciation of the dollar reduces the dollar value of foreign assets.

- Real vs. Nominal Exchange Rates The real exchange rate measures the relative prices of domestic and foreign goods. It accounts for both nominal exchange rates and for local prices. Denote domestic price level P, and denote foreign price level P*, and nominal exchange rate e Cost of American goods in euros is eP Cost of European goods in euros is P* Real exchange rate is = eP/P* If eP/P* is greater than 1, that means U.S. goods are more expensive than European goods.

- Long-Run Behavior of Exchange Rates Purchasing Power Parity (PPP): theory of exchange rates based on the idea that a currency purchases the same quantities of goods and services in different countries; implies that real exchange rates are constant PPP starts with a basic idea called “The Law of One Price” which is a theory that identical goods or services have the same price in all locations. Under PPP, eP/P*=1, so e=P*/P Over a several-year time frame, PPP appears to hold fairly well.

- Real Exchange Rates in the Short Run Prices are determined by the supply and demand for dollars in the Foreign Exchange market Supply of dollars comes from Americans who trade dollars for foreign currencies, either to buy foreign goods (imports) or to buy foreign assets (capital outflow). Demand for dollars comes from foreigners who buy dollars to purchase American goods (exports) or American assets (capital inflow). Equating supply and demand, and rearranging, we get Net Exports (NX) = Net Capital Outflow (NCO) We assume that real exchange rate does not affect NCO, but does affect NX – as the real exchange rate appreciates, NX declines.

More Related

Audio

Live Player