Example

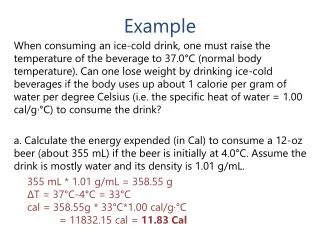

Example. Mr. and Mrs. Barlow, married, with two dependent children, buy a 120 acre tract for purchase price of $135,000 . Additional costs associated with the purchase are shown in the Barlow’s Journal. Journal Page No. 1. Journal Page No. 2, Allocation of Cost Basis.

Example

E N D

Presentation Transcript

Example Mr. and Mrs. Barlow, married, with two dependent children, buy a 120 acre tract for purchase price of $135,000. Additional costs associated with the purchase are shown in the Barlow’s Journal W.L. Hoover

JournalPage No. 1 W.L. Hoover

JournalPage No. 2, Allocation of Cost Basis W.L. Hoover

Sell all timber right away Sell all merchantable timber in 1991 Contract price: $110 per MBF Volume: 12 MBF per acre on 90 acres Net Gain: Gross Revenue $110 x 90 x 12 . . . . . . $118,800 Allowable (Cost) Basis . . (90,342) Sale Expenses . . . . . . . . ( 5,940) ------------- Net Gain . . . . . . . . . . $ 22,518 Reported as a short-term capital gains since timber was held for less than 1 year W.L. Hoover

Sell 42% of timber right away Sell 450 MBF (42% of total) in 1991 Contract Price: $110 per MBF Net Gain: Gross Revenue $110 per MBF x 450 MBF . . $49,500 Allowable Basis $83.65* per MBF x 450 MBF (37,643) Sale Expenses . . . . . . . . . . . ( 3,500) ------------- Net Gain . . . . . . . . . . . . $ 8,357 * Allowable Basis = Depletion Unit x Number of Units Sold $90,342 Depletion Unit = ------------------------ 1,080 MBF = $83.65 per MBF W.L. Hoover

Ten Years Have Passed These transactions occurred over 10-year period: 1. Timber stand improvement (TSI) 90 acres @ $60 per acre 2. Purchase adjacent 20 A tract of timber for $30,000. Timber accounts for 2/3 of acquisition cost 3. Merchantable timber on original tract grew 350 per acre per year. 4. Young growth reached merchantable size and grew an average of 50 BF per acre per year W.L. Hoover

Adjust Accounts • Close out young growth to merchantable timber account • Adjust merchantable timber account ($’s) for previous sale, purchase, and young growth • Adjust merchantable volume account for previous sale, growth, purchase, and young growth W.L. Hoover

Journal W.L. Hoover

LEDGERAccount: Timber Value - Young Growth W.L. Hoover

LEDGERAccount: Timber Volume - Young Growth W.L. Hoover

LEDGERAccount: Timber $’s - Merchantable W.L. Hoover

LEDGERAccount: Timber Volume - Merchantable W.L. Hoover

Sell 900 MBF in 2001Contract price: $145 per MBF Net Gain: Gross Revenue $145 per MBF x 900 MBF . . . . $130,500 Allowable Basis $52.70* per MBF x 900 MBF . . ( 47,430) Sale Expenses . . . . . . . . . . . . . . ( 8,000) -------------- Net Gain . . . . . . . . . . . . . . . . . $ 75,070 $82,205 * Depletion Unit = --------------- 1,560 MBF = $52.70 per MBF W.L. Hoover