Download

1 / 31

350 likes | 654 Vues

From the Short Run to the Long Run. Monetary Policy in the Short Run. In the short run, interest rates are determined by the supply and demand for money. The Fed can change interest rates because it controls the supply of money. Short Run Versus Long Run. In the long run:

E N D

Monetary Policy in the Short Run • In the short run, interest rates are determined by the supply and demand for money. The Fed can change interest rates because it controls the supply of money.

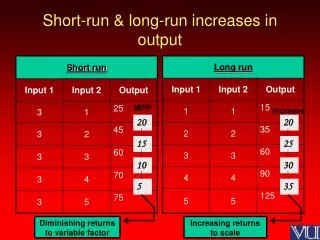

Short Run Versus Long Run • In the long run: • Prices are flexible. • The level of GDP is determined by the demand and supply for labor, the stock of capital, and technological progress. • The economy operates at full employment. • The supply of output is fixed. • Any increases in government spending must come at the sacrifice of some other use of output.

Short Run Versus Long Run • In the short run: • Prices are primarily fixed. Short-run, Keynesian economics applies to the period of time when wages and prices do not change—at least not substantially. • The level of GDP is determined by the total demand for goods and services. • Increases in the money supply, government spending, or tax cuts will lead to an increase in GDP.

Wage and Price Adjustments • Wages and prices rise and fall together. • During booms, when GDP exceeds its full employment level, or potential output, wages and prices tend to increase. Firms will offer higher wages because it is more difficult to find, hire, and retain workers. • During recessions, when GDP falls below potential output, wages and prices will fall together.

Wage and Price Adjustments • As prices rise, workers need higher nominal wages to maintain their real wage. This concept is associated with the reality principle: RealityPRINCIPLEWhat matters to people is the real value of money or income–its purchasing power–not the face value of money or income.

The Wage-price Spiral • The process by which rising wages cause higher prices and higher prices feed higher wages is known as the wage-price spiral. • A wage-price spiral occurs when actual output produced exceeds the potential output of the economy.

Unemployment, Output,and Wage and Price Changes When output exceeds potential, wages and prices will rise above previous inflation rates. For example, if the economy had been experiencing 6% annual inflation, prices will rise at a rate faster than 6% per year.

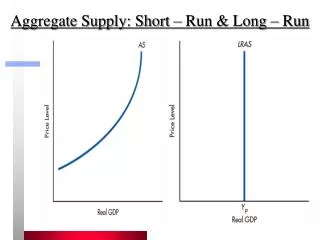

Aggregate Demand,Aggregate Supply and Adjustment • The aggregate demand curve is the relationship between the price level and the quantity of real GDP demanded.

Aggregate Demand,Aggregate Supply and Adjustment • There are two aggregate supply curves: • The classical aggregate supply curve, or long-run aggregate supply, represented as a vertical line at the full-employment level of output.

Aggregate Demand,Aggregate Supply and Adjustment • There are two aggregate supply curves: • The Keynesian aggregate supply curve. A relatively flat supply curve that reflects the idea that prices do not change very much in the short run and that firms adjust production to meet demand.

Aggregate Demand,Aggregate Supply and Adjustment • In the short run, prices and output are determined where the aggregate demand curve intersects the Keynesian aggregate supply curve, at point A.

Aggregate Demand,Aggregate Supply and Adjustment • In the long run, the level of prices and output is determined by the intersection of the aggregate demand and the classical aggregate supply curve, at point D.

Adjustment to Long-run Equilibrium • At point A, output exceeds potential and the unemployment rate exceeds the natural rate. Firms find it difficult to hire and retain workers and the wage-price spiral begins.

Adjustment to Long-run Equilibrium • As the price level increases, the Keynesian aggregate supply curve shifts up over time. Eventually, the economy reaches point D. • At point D, the economy reaches full employment and the adjustment stops.

Adjustment to Long-run Equilibrium • With unemployment at the natural rate, the wage-price spiral ends. • Once the economy has made the transition to the long run, the result is, as predicted by the classical model, that prices are higher and output returns to full employment.

Adjustment to Long-run Equilibrium • If the level of output is below full employment, the adjustment process works in reverse. • The unemployment rate exceeds the natural rate of unemployment. As wages and prices fall, the aggregate supply curve shifts downward until the economy returns to full employment.

The Speed of Adjustmentand Economic Policy • One alternative for policy makers is to do nothing, allowing the economy to adjust itself, down to point D. • Another is to use expansionary policies to shift the aggregate demand curve to the right, up to point E. But, the price level is higher at point E than at point D.

The Speed of Adjustment and Economic Policy • Active economic policies are more likely to destabilize the economy if the adjustment is quick enough: • Economists who believe the economy adjusts rapidly to full employment generally oppose using fiscal or monetary policy to try to stabilize the economy. • Economists who believe the economy adjusts slowly are more sympathetic to using stabilization polices.

A Closer Look atthe Adjustment Process • Model of demand with money: At the current price level P0, the economy is producing at a level of output y0 that is below full employment yF.

Returning to Full Employment • If prices are cut in half, the demand for money shifts leftward. Interest rates fall, investment increases, and total demand shifts up.

Returning to Full Employment • In sum, changes in wages and prices restore the economy to full employment through changes in the demand for money and interest rates, followed by changes in investment and the level of GDP.

Monetary Policy in theShort run and the Long run • In the short run, an increase in the money supply increases output above potential (point A). • In the long run, the economy returns to full employment but at a higher price level, at point B.

Long-run Neutrality of Money • In the long run, changes in the money supply are “neutral” with respect to real variables in the economy, that is, they have no effect on real variables, only on prices. • Money is, however, not neutral in the short run. In the short run, changes in the money supply affect interest rates, investment spending, and output.

Long-run Neutrality of Money • Monetary expansion that initially leads to output above full employment, higher prices and wages, and higher demand for money, eventually results in higher interest rates, lower investment, and a return to full employment.

Long-run Neutrality of Money • If every green dollar was replaced by two blue dollars, then: • Everyone would have twice as many blue dollars as they formerly had of green dollars. • Prices and wages quoted in the blue currency would simply be twice as high as for the green dollars. • The purchasing power of blue money would be the same as it was for green money, therefore, real wages would be the same as before.

Long-run Neutrality of Money • In the long run, the currency conversion has no effect on the real economy, and will be neutral. Prices adjust to the amount of nominal money available. • Whether the money comes from an open market purchase or a currency conversion, it will be neutral in the long run.

Crowding Out in the Long Run • Crowding out is the reduction of investment (or other component of GDP) in the long run caused by an increase in government spending.

Crowding Out in the Long Run • Crowding out of investment spending in the long run, translates into reduced capital deepening and lower levels of real income and wages in the future. • Tax cuts can also crowd out investment in the long run. Tax cuts will lead to an increase consumption; a higher level of GDP; higher prices, wages, and demand for money, thus higher interest rates.

Crowding Out in the Long Run • Crowding in is the increase of investment (or other component of GDP) in the long run caused by a decrease in government spending. • The economy will experience increased capital deepening and higher levels of real income and wages in the future.

Political Business Cycles • The political business cycle describes the effects on the economy of using monetary or fiscal policy to stimulate the economy before an election to improve reelection prospects. • The long run impact of expansionary policies to stimulate the economy before reelection are higher prices, or crowding out after reelection. Before the election, the economy booms; after the election, the economy contracts.