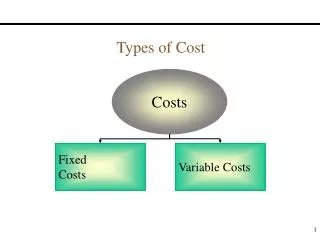

Three manufacturing costs

340 likes | 915 Vues

Direct material cost: Consist of all those material that can be identified with a specific product. Example: wood used in manufacturing of a table. Direct labor cost :

Three manufacturing costs

E N D

Presentation Transcript

Direct material cost: Consist of all those material that can be identified with a specific product. Example: wood used in manufacturing of a table. Direct labor cost : Consist of all those cost that can be specifically traced or identified with a particular product. Example: wages of workers working on that table. Overhead (indirect) cost: overhead refers to the cost pool used to accumulate all indirect manufacturing costs. Indirect costs are allocated to the cost object using of cost allocation method. Example: heat, light and power for the factory, rent on factory building, property taxes on factory building, and all kind of depreciation. Three manufacturing costs

Overhead consists of many individual cost items. These are costs that can’t be measured or traced for a specific product. Factory overhead costs are both fixed and variable. The factory overhead controlling account is debited when costs are incurred and credited when factory overhead is applied to various job orders. i.e indirect material and labor, utility costs, depreciation of equipment and salaries of factory administrative personnel. Factory Overhead

The most simplistic traditional costing system assigns indirect costs to cost objects using a single overhead rate for the organization as a whole. The terms blanket overhead rate or plant-wide rate are used to describe a single overhead rate that is established for the organization as a whole. Plant-wide (blanket) overhead rates

A job is a production run for a specific product. A relatively small number of units generally comprise a job. Job order costing system record actual and estimated production costs in the formal accounting system leading to manufacturing statements. Construction firms use a variation of job order costing. Some overhead is applied to each job so that the contractor can recoup its general production costs which apply to all jobs but which are not traceable to any specific job. Job Order Costing

You will know on an ongoing basis which projects are profitable and which ones aren’t. You will be able to get paid on a timely basis as you complete the job. You can avoid committing resources to projects. If you manufacture products: You will know what it cost to make each item You will be able to set selling prices that cover your costs and earn a fair profit You will know what product lines to expand because they’re profitable, and what product line to drop because they’re unprofitable. Benefits of job costing

Identify the job that is chosen cost object The cost object can be chosen through the job cost record. Companies keep a job cost record for every specific job. A job cost record, also called a job cost sheet records and accumulates all the costs assigned to a specific job, starting when work begins. General approach to job costing

Identify the Direct costs of the job: Robinson identified two direct manufacturing cost categories, direct material and direct manufacturing labour. Example can be seen for the direct costs for the specific job. Select the cost allocation bases to use for allocating indirect cost to the job. Indirect costs can’t be allocated to a specific product. It will be impossible to complete a job without incurring indirect cost such as supervision, manufacturing engineering, utilities and repairs. Multiple cost allocation bases are used to allocate a indirect cost because different indirect cost have different cost drivers. Example : depreciation or repair of machines is closely related to machine hours so machine hours can be used as a cost driver.

Identify the indirect cost associated with each cost allocation base. Now that the allocation bases has been identified, all indirect cost are now identified for that allocation base. In our example from the Robinson company they use indirect manufacturing costs to machinery hours used. Compute the rate per unit of each cost allocation base used to allocate indirect costs to the job. Actual manufacturing overhead costs Actual manufacturing overhead rate = Actual total quantity of cost allocation base $1215000 Actual manufacturing overhead rate = 27000 direct manufacturing labor hours $45 per direct manufacturing labor hour =

Compute the indirect costs allocated to the job. Indirect cost allocated to a job= actual quantity of each different allocation base x indirect cost rate of each allocation base Compute the total cost of the job by adding all direct and indirect costs assigned to the job. Total cost= Direct cost + Indirect cost

JOB-COST RECORD JOB NO: WPP 298 CUSTOMER: Western Pulp and Paper Date Started: Feb. 3, 2006 Date Completed: Feb. 28, 2006 DIRECT MATERIALS Materials Requisition No. Unit Cost Date Received Quantity Used Total Costs Part No. Feb. 3, 2006 2006: 198 MB 468-A 8 $ 14 $ 112 Feb. 3, 2006 2006: 199 TB 267-F 12 63 756 • • $4,606 Total DIRECT MANUFACTURING LABOR Labor-Time Record No. Hourly Rate Period Covered Employee No. Hours Used Total Costs Feb. 3-9, 2006 LT 232 551-87-3076 25 $ 18 $ 450 Feb. 3-9, 2006 LT 247 287-31-4671 5 19 95 • • $1,579 Total MANUFACTURING OVERHEAD Allocation-Base Units Used Cost pool Category Allocation- Base Rate Total Costs Date Allocation-Base Dec. 31, 2006 Manufacturing Direct Manufacturing 88 hours $ 45 $ 3,960 Labor-Hours $ 3,960 Total $ 10,145 TOTAL MANUFACTURING COST OF JOB

MATERIALS-REQUISITION RECORD Materials-Requisition Record No: 2006: 198 Feb. 3, 2006 Unit Total Cost Cost Date: Quantity 8 Job No.: Part No. MB 468-A WPP 298 Part Description Metal Brackets $14 $112 Issued By:B. Clyde Received By: L. Daley Date: Date: Feb. 3, 2006 Feb. 3, 2006

Panel 2Material Requisition Number Description Quantity Rate Amount47624 Bar steel 720 lbs $11.50 $8,280.00 Stock 3” A35161 Subassemblies 290 units 38.00 $11,020.00 Total direct materials cost $19,300.00 Panel 1Job Number: J4369 Date: July 6, 2000Customer: Michigan MotorsProduct: Automobile engine valves (Valve #L181)Engineering Design Number: JDR-103Number of Units: 1,500

Panel 3Dates Number Hours Rate Amount 8/2, 8/3, 8/4, 8/5 M16 24 $28.00 $672.00 8/2, 8/3, 8/4, 8/5 M18, M19, M20 64 26.00 1,664.00 8/6, 8/7, 8/8, 8/9, 8/10 A25, A26, A27 120 18.00 2,160.00 8/6, 8/7, 8/8, 8/9, 8/10 A32, A34, A35 60 17.00 1,020.00 Total direct labor cost 268 $5,516.00 Panel 4 Support Cost Amount 117 Machine hours @ $40 per hour $ 4,680.00 268 Direct labor hours @ 36 per hour 9,648.00 Total overhead cost $14,328.00

Concept of Costing System Cost Assignment Direct costs Cost Object Cost Tracing Indirect costs Cost Allocation

A cost allocation is the process of assigning costs when a direct measure does not exist for the quantity of resources consumed by a particular cost object. Example: consider an activity such as receiving incoming materials. Assuming that the depreciation of the machine is strongly related to the number of hours machine was used. The basis that is used to allocate costs to cost objects is called an allocation base or cost driver. Two types of systems can be used to assign indirect costs to cost objects. They are traditional costing system and activity-based-costing(ABC) systems. Assigning direct and indirect costs

Cost Allocations and Cost Tracing Direct costs Cost tracing Traditional costing systems Cost objects Indirect costs Cost allocations ABC systems

Traditional Costing Systems Overhead cost accounts (for each individual category of expenses) First stage allocations Cost center 1 (Normally departments) Cost center 2 (Normally departments) Cost center N (Normally departments) Second stage allocations (Direct labour or machine hour) Cost objects (Products, services and customers) Direct cost

Applying the three-stage allocation process requires the following four steps: Assigning all manufacturing overheads to production and service cost centres; Reallocating the cost assigned to service cost centres to production cost centres; Computing separate overhead rates for each production cost centre; Assigning cost centre overheads to products or other chosen cost objects. An illustration of the three-stage process for a traditional costing system

Traditional Costing System Levels of Sophistication Simplisticsystems • Inexpensive to operate • Extensive use of arbitrary cost allocations • Low levels of accuracy • High cost of errors

Service dept S1 S4 S2 S3 Conceptual view of the separate department overhead rates Producing dept DM DL FO DM DL FO DM DL FO Cost objects Cost objects Cost objects Cost objects Cost objects Cost objects

Common cost are allocated to all the departments. Some cost can be directly related such as salary of the engineer working in the service quality department, however other need to be allocated using an allocation base. Basis of allocation Cost Area Number of employees Value of items of plant and machinery Property taxes, lighting and heating Employee-related expenditure: works management, works canteen, payroll office Depreciation and insurance of plant and machinery Stage1 : Assigning all manufacturing overhead to production and service departments.

Stage2 :Reallocating the cost assigned to service cost centers to production cost centers. the next step is to reallocate the costs that have been assigned to service cost centres to production cost centres. Service departments or support department are those departments that exist to provide services of various kinds of other units within the organization. For example, the costs of the cafeteria can be reallocated to the production cost center by using number of workers in the factory as the allocation base. There are three methods in reallocating the cost from service to production departments. DIRECT METHOD STEP METHOD ALGEBRIC METHOD

Diagram of 3 diff, allocation methods Service department Producing department X A Part 1 Direct method B Y X A Part 2 Step method B Y X A Part 3 Algebraic method B Y

In the final step is to allocated the overheads to products passing through the production centers. Volume base allocation is used to assign the overhead costs to the products. Example, number of units produced, number of machine hours used. Stage 3: Assigning cost center overheads to products or other chosen cost objects.

The annual costs for the Enterprise Company which has three production centres (two machine centres and one assembly centre) and two service centres (materials procurement and general factory support) are as follows: (£) (£) Indirect wages and supervision Machine cenres: X Y Assembly Materials procurement General factory support Indirect materials Machine centres: X Y Assembly Materials procurement General factory support Lighting and heating Property taxes Insurance of machinery Depreciation of machinery Insurance of buildings Salaries of works management 1 000 000 1 000 000 1 500 000 1 100 000 1 480 000 6 080 000 500 000 805 000 105 000 0 10 000 1 420 000 500 000 1 000 000 150 000 1 500 000 250 000 800 000 4 200 000 11 700 000

The following information is also available: Area Occupied (sq. metres) Number Of employees Direct Labour hours Book Value of Machinery (£) Machine hours Machine shop: X Y Assembly Stores Maintenance 8 000 000 5 000 000 1 000 000 500 000 500 000 10 000 5 000 15 000 15 000 5 000 300 200 300 100 100 1 000 000 1 000 000 2 000 000 2 000 000 1 000 000 1000 15 000 000 50 000 Details of total material issues to the production centres are as follows: (£) 4 000 000 3 000 000 1 000 000 Machine shop X Machine shop Y Assembly 8 000 000

OVERHEAD ANALYSIS SHEET Production centres Service centres Machine centre X (£) Machine centre Y (£) Materials procurement (£) General factory support (£) Total (£) Assembly (£) Item of expenditure Basis of allocation Indirect wage and supervision Indirect materials Lighting and heating Property taxes Insurance of machinery Depreciation of machinery Insurance of buildings Salaries of works management Reallocation of service centre costs Materials procurement General factory support Machine hours and direct labour hours Machine hour overhead rate Direct labour hour overhead rate Direct Direct Area Area Book value of machinery Book value of machinery Area Number of employees (1) Value of materials issued Direct labour hours (2) 6 080 000 1 420 000 500 000 1 000 000 150 000 1 500 000 250 000 800 000 1 000 000 500 000 100 000 200 000 80 000 800 000 50 000 240 000 1 000 000 805 000 50 000 100 000 50 000 500 000 25 000 160 000 1 100 000 150 000 300 000 5 000 50 000 75 000 80 000 1 480 000 10 000 50 000 100 000 5 000 50 000 25 000 80 000 1 500 000 105 000 150 000 300 000 10 000 100 000 75 000 240 000 11 700 000 2 970 000 2 690 000 2 480 000 1 760 000 1 800 000 880 000 450 000 660 000 450 000 220 000 900 000 1 760 000 1 800 000 11 700 000 4 300 000 3 800 000 3 600 000 2 000 000 1 000 000 2 000 000 £2.15 £3.80 £1.80

Reallocation of Service centre costs Materials procurement General factory support Machine hours and direct labour hours Machine hour overhead rate Direct labour hour overhead rate Value of materials issued Direct labour hours (2) 880 000 450 000 660 000 450 000 220 000 900 000 1 760 000 1 800 000 11 700 000 4 300 000 3 800 000 3 600 000 2 000 000 1 000 000 2 000 000 £2.15 £3.80 £1.80

cost centre overheads cost centre direct labour hours or machine hours £4 300 000 Machine centre X = = £2.15 per machine hour 2 000 000 machine hours £3 800 000 Machine centre Y = = £3.80 per machine hour 1 000 000 machine hours £3 600 000 Assembly department = = £1.80 per direct labour hour 2 000 000 direct labour hours

£ Product A Direct costs (100 units x £100) Overhead allocations Machine center A (100 units x 5 machine hours x £2.15) Machine center B (100 units x 10 machine hours x £3.80) Assembly (100 units x 10 direct labour hours x £1.80) Total cost Cost per unit (£16 675/100 units) = £166.75 10 000 1 075 3 800 1 800 16 675 £ Product B Direct costs (200 units x £200) Overhead allocations Machine center A (200 units x 10 machine hours x £2.15) Machine center B (200 units x 20 machine hours x £3.80) Assembly (200 units x 20 direct labour hours x £1.80) Total cost Cost per unit (£66 700/200 units) = £333.50 40 000 4 300 15 200 7 200 66 700