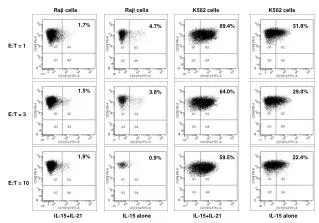

1.7 Resource Markets

1.7 Resource Markets. U nit Overview. Introduction to Resource Markets. 1.7 Resource Markets. Introduction to Resource Markets

1.7 Resource Markets

E N D

Presentation Transcript

1.7 Resource Markets Unit Overview

Introduction to Resource Markets • 1.7 Resource Markets Introduction to Resource Markets Throughout most of this course we have examined the interactions of buyers and sellers in product market, in which households are the buyers and firms the sellers. Recall from our circular flow model, however, that a market economy includes a market in which the roles are reversed. • Resource (or Factor) Markets: Where households provide firms with the factors of production needed to produce good and services. The resources sold include: Labor, Land and Capital. Households receive money payments for their resources. These are: • For Labor – WAGES • For Land – RENT • For Capital - INTEREST • These payments are determined just like any other price, by market supply and demand.

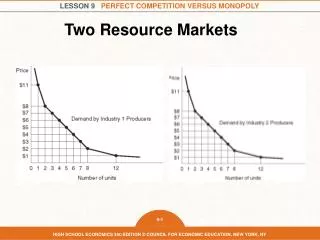

Introduction to Resource Markets • 1.7 Resource Markets Degrees of Competition in Resource Markets Resource markets, like product markets, can have lots of competition or be relatively uncompetitive. However, unlike product markets, competition in resource markets is among the BUYERS of resources, not among the SELLERS of products. A perfectly competitive resource market: Is one in which there are hundreds of firms competing with one another to HIRE WORKERS… The market price is the wage rate firms pay workers, and this is determined entirely by the market demand for labor and the market supply of labor. Firms in perfectly competitive labor markets are known as “wage-takers” because they can hire as many workers as they like at the equilibrium wage rate. They do not need to raise wage to attract more workers. An imperfectly competitive resource market: Is one in which there is only one firm (or a relatively small number of firms) hiring all of one particular type of labor. This type of labor market is known as a monopsony, which means “single buyer” Firms in a monopsonistic labor market are known as “wage-makers” because in order to attract more workers, they must raise the wages they pay all their workers.

Derived Demand for Resources • 1.7 Resource Markets • Derived Resource Demand • Demand for any resource (labor, land or capital) is derived demand. This means it depends on other factors, including: • The price of the good the resources is used to produce, • The productivity of the resource • The demand for a resource is determined primarily by the productivity of the resource. Recall from an earlier unit the law of diminishing returns. This stated that; • As additional units of a variable resource put towards the production of a good using fixed resources, the output of additional units of the variable resource will eventually decrease. • In other words, the more labor you add to a fixed amount of capital, the less additional output the labor will produce. • For this reason, demand for labor is going to be inversely related to the price of labor (the wage rate). • Firms will only wish to hire more workers as the wage rate falls.

1.7 Resource Markets Marginal Revenue Product • Marginal Revenue Product • The demand for a resource (we will focus on labor) is based on the productivity of the resource and the price of the good being produced. Labor demand is based on the marginal revenue product of labor. • Marginal Revenue Product of Labor (MPR) = the change in a firm’s total revenue resulting from the employment of one additional worker. It can also be measured by the marginal physical product of labor multiplied by the price of the good being produced. • (where Pg is the price of the good) • MRP is the revenue attributable to the last worker hired… Due to diminishing marginal returns, as more and more workers are hired in the short-run, MRP will decrease, because: • Labor productivity decreases as labor is added to fixed capital, and in the case of a price-making firm, • The price of the output must decrease as output increases in order for the firm to sell additional units.

1.7 Resource Markets Marginal Revenue Product • Marginal Revenue Product for a Perfectly Competitive Seller • The marginal revenue product of labor is determined by the productivity of labor and the price of the output. Consider the production data for a bakery below. • The bakery sells its bread in a perfectly competitive market at a price of $2 per loaf • The bakery can hire anywhere from 1 to 8 workers. • Calculating the MRP will tell the bakery how much revenue each additional worker adds to the firm’s total revenue. • Calculate the MRP of each worker: • Multiply the marginal product of each worker (how much output she contributes) and the price of bread. • This tells us the most the bakery would be willing to pay each worker,or, the DEMAND FOR LABOR

1.7 Resource Markets Marginal Revenue Product • Marginal Revenue Product for a Perfectly Competitive Seller • The MRP of labor is analogous with the firm’s demand for labor. This is because: • MRP tells the firm how much additional revenue each worker adds to the total revenu • The firm will be willing to pay anything UP TO, but not greater than, each worker’s MRP in order to hire that worker. • Consider, for example, the 4th worker in the bakery: • The fourth worker contributed 3 additional loaves of bread per hour to the bakery’s output • Each loaf sold for $2 • So the worker was accountable for $6 per hour of additional revenue for the bakery. • The bakery would happily pay this worker $3 per hour, or even $4, or ever $5, or even $5.99! • The bakery would be willing to pay the baker up to, but no more than $6 per hour, since this is exactly how much revenue the worker contributes per hour!

1.7 Resource Markets Marginal Revenue Product Marginal Revenue Product for a Perfectly Competitive Seller By plotting the marginal revenue product of labor against the quantity of labor hired, we can see the firm’s demand for labor curve. • Notice from the graph: • There is clearly an inverse relationship between the quantity of labor demanded and the wage rate. • At higher wage rates, a lower number of workers will be hired (because the MRP has to be high enough to cover the wages paid) • At lower wage rates a larger number of workers is demanded (since the firm can afford to hire workers with a lower MRP). 14 Demand for Labor 12 10 MRP = PL (wage rate) 8 6 4 2 D=MRP 7 1 2 3 4 5 6 QL

1.7 Resource Markets Marginal Revenue Product Marginal Revenue Product for an Imperfectly Competitive Seller Now let’s consider how the level of competition in the product market will affect a firm’s demand for labor. Assume now that our bakery is selling bread in an imperfectly competitive market, making the firm a price-maker. The bakery must now lower its price to sell additional loaves of bread. • Calculate the MRP of each worker: • Notice that now BOTH marginal product AND the price of bread falls, • The bakery is willing to pay more for the first couple workers, because the price of bread is high • But MRP falls more rapidly than it did for the perfectly competitive seller.

1.7 Resource Markets Marginal Revenue Product Marginal Revenue Product for an Imperfectly Competitive Seller An imperfectly competitive seller’s demand for labor will be much less responsive to chages in the wage rate than a perfectly competitive seller. In other words, demand for labor is more inelastic among monopolistic firms (and other imperfectly competitive sellers). • Demand for labor is highly inelastic: • To go from one worker to 2 workers, the seller would require a $10 decrease in the wage rate. This compares to the perfectly competitive seller, which hired a second worker when the wage fell by only $2 • Because the price of bread decreases as the bakery makes more bread, it is very hesitant to hire additional workers, i.e. demand for labor is wage inelastic

1.7 Resource Markets Marginal Revenue Product Marginal Revenue Product for an Imperfectly Competitive Seller By plotting the marginal revenue product of labor against the quantity of labor hired, we can see the firm’s demand for labor curve. • Notice from the graph: • The blue line represents the imperfectly competitive seller’s demand for labor. • The green line is the perfectly competitive seller’s demand for labor • The imperfectly competitive seller’s labor demand begins at a higher wage rate (since it can sell bread at a higher price at first), but drops rapidly with the additional workers hired due to the fact that both MP and P are declining as output increases. 30 28 Demand for Labor 24 20 MRP = PL (wage rate) 16 12 8 4 D=MRP 7 1 2 3 4 5 6 QL

1.7 Resource Markets Market Labor Demand • Competitive Labor Markets – Market Demand for Labor • The demand for labor is based on the marginal revenue product of labor in a particular industry. • On the previous slides we showed individual firms’ demands for labor. • In the labor market as a whole, demand for labor consists of the sum of all the individual firms in the market. • Assume, for example, that there are 100 bakeries competing to hire bakers. Each firm has the MRP for labor that we calculated previously. Market labor demand is simply the sum of all the individual firms competing for workers. 14 14 Each Firm’s Demand for Labor The Market Demand for Labor 12 12 10 10 MRP = PL (wage rate) MRP = PL (wage rate) 8 8 X 100 firms = 6 6 4 4 2 2 D=MRP D=MRP QL QL 700 7 100 1 200 2 300 3 400 4 500 5 600 6

1.7 Resource Markets Market Labor Supply Competitive Labor Markets – Market Supply of Labor To understand how supply of labor is determined, we must only imagine how households respond to changes in the wage rate being paid to a particular type of worker: • There is a direct relationship between the wage rate and the supply of labor • Imagine the wages for bakers is rising. More individuals will be willing and able to become bakers at higher wage rates, since it means more income is to be earned! • If wages for bakers are falling, fewer individuals will be willing and able to work as bakers, since it would mean lower income for the households. • The equilibrium wage rate and the quantity of labor employed in a perfectly competitive labor market is determined by the intersection of labor supply and labor demand! The Perfectly Competitive Labor Market 14 Supply of Labor 12 10 MRP = PL (wage rate) 8 6 4 2 D=MRP 700 100 200 300 400 500 600 QL

1.7 Resource Markets Marginal Resource Cost • Marginal Resource Cost • A firm faces a downward sloping demand for labor curve due to the decreasing productivity of labor in the short-run (and for a price-maker, the falling prices of its output). To determine exactly how many workers a firm should hire, it must consider not only the MRP of labor, but also the Marginal Resource Cost: • Marginal Resource Cost (MRC): The cost to a firm of hiring one additional worker. • In perfectly competitive labor markets, MRC = the Wage Rate: A “wage-taker” is a firm that can hire as many workers as it wants at the market wage rate. The cost of each additional worker, therefore, is simply the wage the firm must pay that worker, which never changes as the level of employment changes! • In a monopsonisticlabor market, MRC is always greater than the wage rate: A “wage-maker” is a firm that must raise the wages it offers workers in order to attract more individuals to come work for the firm. Since hiring one more worker requires raising wages for workers who are already employed, the cost of hiring the additional worker is higher than the actual wage the firm has to pay that worker.

1.7 Resource Markets Profit Maximization Profit Maximization Rule of Resource Employment Based on what we know about MRP (the change in a firm’s revenues of hiring one more worker) and MRC (the change in a firm’s costs of hiring one more worker), the decision of how many workers to employ can be thought of as simple cost/benefit analysis. The Profit Maximization Rule of Resource Employment: If the cost of hiring an additional worker (the MRC) is less than the benefit of hiring the worker (the MRP), then the worker should be hired! If the cost is greater than the benefit, then he should not be hired. Workers should be hired up until the MRP = MRC In perfectly competitive labor markets, this means individual firms should hire workers until the MRP of the last worker is equal to the market wage rate.

1.7 Resource Markets Profit Maximization Profit Maximization in a Perfectly Competitive Labor Market Based on the rule explained in the previous slide, a perfectly competitive employer will want to hire workers until the MRP of the last worker equals the market wage rate. The Perfectly Competitive Labor Market 14 14 A Single Firm in the Labor Market Supply of Labor 12 12 10 10 MRP = PL (wage rate) MRP = PL (wage rate) 8 8 We We MRC 6 6 4 4 2 2 D=MRP D=MRP The MRC seen by the individual firm is the market wage rate (We). The “wage-taker” can hire as many workers as it wishes at We. 700 7 100 1 200 2 300 3 400 4 500 5 600 6 QL QL

1.7 Resource Markets Profit Maximization Profit Maximization in a Monopsonistic Labor Market As explained previously, a monopsonist is a firm which must raise wages to attract new workers to the market. The firm is a “wage-maker”. For this reason, the MRC is always going to be greater than the wage rate the firm is actually paying. The Monopsonistic Labor Market • Observe from the graph: • Because the single employer must raise wages to attract more workers, it will always cost the firm more to hire one more worker than the wage it has to pay that worker. • Wages must be risen for all workers! • The MRC rises faster than the wage rate. • As a result, the firm will hire fewer workers and pay them lower wages than would be paid in a perfectly competitive labor market! 14 MRC Supply of Labor 12 10 MRP = PL (wage rate) 8 6 We 4 2 D=MRP 700 100 200 300 400 500 600 QL

1.7 Resource Markets Profit Maximization Employment in Perfectly Competitive vs. Monopsonistic Markets Due to its wage-making ability, a monopsonist will employ fewer workers and pay lower wages than would be hired in a perfectly competitive labor market. The Monopsonistic Labor Market The Perfectly Competitive Labor Market 14 14 MRC Supply of Labor Supply of Labor 12 12 10 10 MRP = PL (wage rate) MRP = PL (wage rate) 8 8 We 6 6 We 4 4 2 2 D=MRP D=MRP Monopsonistic labor markets are undesirable to workers, for whom there will be fewer employment opportunities and lower wages offered. 700 700 100 100 200 200 300 300 400 400 500 500 600 600 QL QL

1.7 Resource Markets Minimum Wages Minimum Wages in Labor Markets Assume the government sets a minimum wage in the two labor markets below. A minimum wage is a price floor in a labor market, set above the equilibrium wage rate. The Monopsonistic Labor Market The Perfectly Competitive Labor Market 14 14 MRC Supply of Labor Supply of Labor 12 12 10 10 Wm MRP = PL (wage rate) MRP = PL (wage rate) 8 8 Wm 6 6 4 4 2 2 D=MRP D=MRP 700 700 100 100 200 200 300 300 400 400 500 500 600 600 QL QL Wm becomes the firm’s MRC, and it’s lower than the previous MRC. The firm will end up hiring more workers! Qs of labor will increase, while Qd will decrease. Unemployment results in the PC labor market

1.7 Resource Markets The Least Cost Rule • The Least Cost Combination of Resource Employment • When deciding on the optimal combination of two resources (say workers and robots) a firm should consider the marginal product per dollar spent on each resource. • Similar to the utility maximization rule of consumer behavior, which said that consumers should buy the goods which provide them with the most marginal utility per dollar. • When a firm employs the resource that gives it the most marginal product per dollar, the firm is maximizing its “bang for its buck” • The Least Cost Combination of Resources: When a firm is hiring two resources (labor and capital) it should attempt to employ them up to the point where the last dollar spent on labor yielded the same additional output as the last dollar spent on capital: • Where… MPL is the marginal product of labor and PL is the price of labor, and • MPC is the marginal product of capital and Pc is the price of capital

1.7 Resource Markets Quick Quiz • Quick Quiz on Resource Markets • Why is the Marginal Revenue Product curve equivalent to an individual firm’s labor Demand curve? • In pure competition, a firm will hire workers up to the point at which the market wage rate (MRC) is equal to its MRP. Hence, the firm’s MRP schedule constitutes the firm’s D for labor, because each point on this curve indicates the number of workers the firm would hire at each possible wage rate. • Why does a purely competitive firm’s D for labor tend to be more elastic than an imperfect competitor’s? • Perfect competitors face a downward sloping D curve because marginal productivity diminishes as more workers are hired. Imperfect competitors face diminishing marginal productivity AND product price falls as output increases. Therefore, imperfectly competitive firms are LESS responsive to changes in the wage rate than perfect competitors. (i.e. less elastic resource D) • What makes resource demand "derived demand"? • Demand for resources is derived from the productivity of the resource as well as the price of the good or service the resource is used to produce

1.7 Resource Markets Discussion Questions Discussion Questions on Resource Markets What determines demand for labor? What determines the supply of labor? How is the wage rate determined? Why are wages higher in the US and Western Europe than in countries like India and China? What is the difference between nominal wage and real wage? What determines the level of employment and the wage rate in a purely competitive labor market and a representative firm? (include a diagram) What determines the level of employment and the wage rate in an imperfectly competitive labor market? (include a diagram) What are the effects of a minimum wage? Is a minimum wage good or bad for society? (include a diagram)