Download

1 / 49

490 likes | 514 Vues

Review for ECON1000 students on lectures 1-4, covering key concepts and chapters 1-4. Prepare with non-programmable calculator, pencil, eraser, Student ID, and tutor’s name. Test duration: 45 minutes. Total marks: 20.

E N D

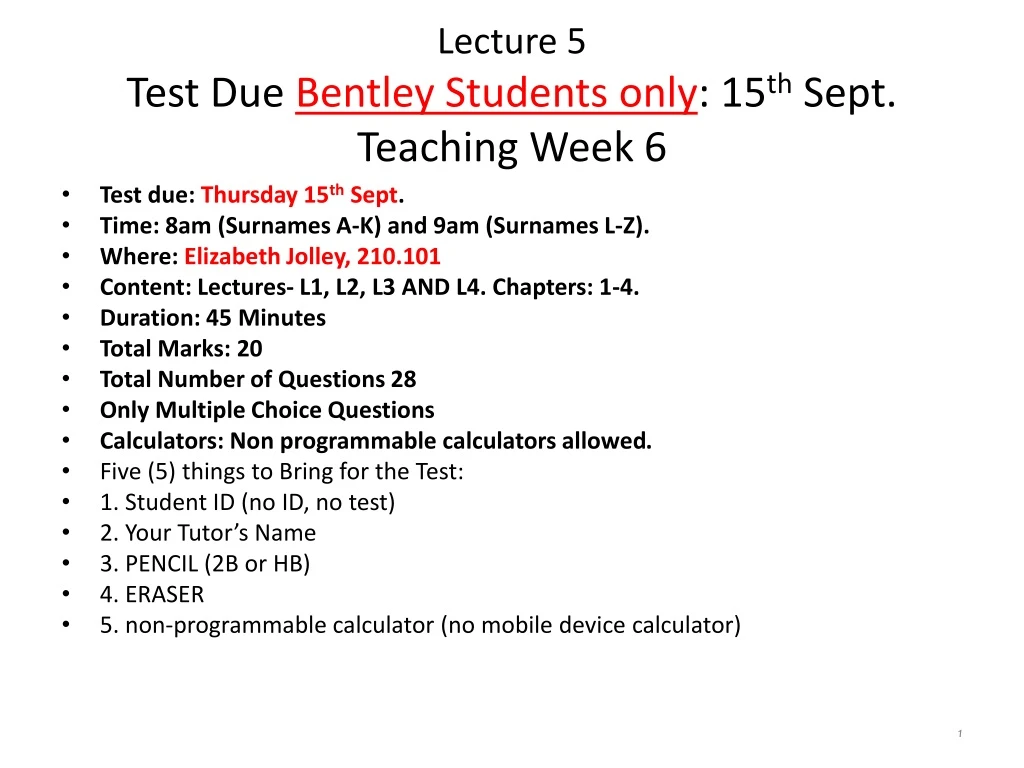

Lecture 5 Test Due Bentley Students only: 15th Sept. Teaching Week 6 • Test due: Thursday 15th Sept. • Time: 8am (Surnames A-K) and 9am (Surnames L-Z). • Where: Elizabeth Jolley, 210.101 • Content: Lectures- L1, L2, L3 AND L4. Chapters: 1-4. • Duration: 45 Minutes • Total Marks: 20 • Total Number of Questions 28 • Only Multiple Choice Questions • Calculators: Non programmable calculators allowed. • Five (5) things to Bring for the Test: • 1. Student ID (no ID, no test) • 2. Your Tutor’s Name • 3. PENCIL (2B or HB) • 4. ERASER • 5. non-programmable calculator (no mobile device calculator)

Test: Instructions • Choose the one alternative that best completes the statement or answers the question. Attempt ALL 28 questions. • This test is divided into six (6) sub-headings that correspond to the relevant concepts taught in the lectures. • Record your answers in PENCIL (2B or HB) Only on both the question paper & on the separate Answer Sheet. • Return your question paper with the Answer Sheet to the test supervisor(s). [Test paper is not returned back to student.]

Test :Topics • The 45-minute test is designed to be as fair as possible for all ECON1000 students - there are no ‘trick’ multiple-choice questions (MCQs). • This test is divided into six (6) sub-headings that correspond to the relevant concepts taught in the lectures (L1 to L4). In the ECON1000 S2 2016 test, you will come across the six sub-headings with the following allocation and number of questions: • 3 MCQs onOpportunity Cost and ppf • 9 MCQs on Demand and Supply • 6 MCQs on Elasticity • 3 MCQs on Consumer and Producer Surplus • 2 MCQs on Rent CeilingS and PRICE FloorS • 5 MCQs on Tax • SAMPLE TEST PAPER AVAILABLE ON BB UNDER ASSESSMENT TAB.

Econs1000 S2 2016, Lecture 5§Chapter 5Behavioural Economics &Asymmetric Information

What’s good about markets? • As demonstrated in Lecture 4, ‘equilibrium’ in a competitive market results in • the economically efficient level of output, where MB = MC. • the greatest amount of Total Surplus, from the production and consumption of a good or service. BUT … † • Not all economic agents make their choices rationally to calculate an ‘optimal’ level of welfare. • The market system may give us an efficient level of output, but we know little about the real implications on society.

PART A of L5.Behavioural economics: Do people make their choices rationally? • Behaviouraleconomics: the study of situations in which people act in ways that are not economically rational. • Consumers commonly commit the following 3 mistakes when making decisions (see slide 5): • they take into account monetary costs but ignore non-monetary opportunity costs • they fail to ignore sunk costs • they are overly optimistic about their future behaviour

‘Utility’ and consumer decision making • Utility: The enjoyment or satisfaction that people receive from consuming goods and services. • Traditional economics: • assumes that consumers will choose to buy the combination of goods and services that make them as well off as possible from among all the combinations that their budgets allow them to buy, i.e. maximise utility.

Behavioural economics: Do people make their choices rationally? • Ignoring non-monetary opportunity costs • Businesses sometimes make use of consumers’ failure to take into account opportunity costs • Failingto ignore sunk costs • Sunk cost: A cost that has already been paid and that cannot be recovered. • Being unrealistic about future behaviour • Examples: People saying they will quit smoking ‘sometime’ or diet ‘soon’, but it doesn’t happen. • Current utility is overvalued and future utility is undervalued.

Social influences on decision making Does fairness matter? • There is a lot of evidence that people like to be treated fairly and that they usually attempt to treat others fairly, even if doing so makes them worse off financially. • Business implication of fairness • Firms sometimes do not raise prices of goods and services, even when there is a large increase in demand. • Why? They are afraid their customers will consider the price increases unfair and may buy elsewhere.

Psychology and Economics:assumptions made about people must be realistic. Daniel Kahneman

Kahneman describes the traditional model as descriptively unrealistic. From his Nobel lecture: • Traditional economics: • People (‘agents’) are strictly logical, centred on a clearly defined goal and free from the unsteady influences of emotion. • Kahneman: • Most decisions that people make are intuitive. • People tend to make decisions spontaneously, without making conscious searches or computations. • Human thoughts are often emotionallycharged and governed by habit.

Kahneman’sanalysis of intuitive thought: effortless, fast and automatic • If most thought is intuitive, then we need to understand what causes us to think certain things spontaneously … • What makes some thoughts highly accessible (i.e. that come quickly to the mind)? • Kahneman(2003) argues that we cannot understand preferences (our likes and dislikes) without understanding the psychology of emotions • an emotional evaluation that occurs before conscious reasoning.

Application 1. Endowment Effect • People often demand much more to give up an item than they would pay to acquire it • When asked to choose between an iPod & $100 (US), subjects were more likely to choose $100 • When given an iPod and asked to trade for $100, most turned down the offer Source: http://www.livescience.com/5004-save-stuff.html

Application 2.Reference Points Behavioural Economics also asserts that the value we place on goods depends on our circumstances or the point from which we make our consumption decision. Example 1: • You bought a ticket for $100 as this is the value you attached to the concert. You find out you could resell it at $500 due to excess demand. • Traditional: Sell the ticket for $500. • Behavioural: Keep the ticket and go to the concert. • Once we own something, we don’t like to lose it. • Your reference point in this case is owning the ticket.

Application 2.Reference Points Example 2: • You get a bonus of $5000. Then you find out that your colleague got a bonus of $10000. • Traditional: You’re happy no matter what your colleagues get – increase in income increases utility (satisfaction). • Behavioural: You get depressed • Your colleague’s income has increased more than yours. • We evaluate our outcomes with reference to the group norm. Your reference point is the increase received by others. • Relative positioning: People tend to be most interested in their relative gains and losses as opposed to their final income and wealth.

‘Bounded Rationality’ • People are boundedly rational and ‘satisfice’—they do the best they can, given the constraints they face. • People are not endowed with the capacity to efficiently and effectively acquire and process all relevant information. • Given the reality of their cognitive wiring and uncertainty and imperfection of information and knowledge • People often face decision-making environments that prevent them from making the best possible choices. • People can and often do make decisions they end up regretting.

PART B of L5:3 reasons for government intervention(or participatory action) due to market failure • Externalities • Public Goods & Common Resources • Asymmetric Information

Two Types of failure • Market failure (focus on in this lecture) • asituation in which the market fails to produce a socially efficient level of output or outcome • Genuine total benefits are notmaximised. • The price system fails to produce the quantity of a good that would be “socially optimal”. • Government failure • occurs when the government fails to correct adequately for market failure or takes actions that lead to a more inefficient outcome than the market.

1. Private Markets & External Costs/Benefits • Private decisions in a market are based on the benefits buyers expect to receive and the costs that firms must pay. • People seldom take into account the costs and benefits their choices have on others – these are called EXTERNAL costs & benefits

An externalityis • a cost or benefit that arises from productionand falls on someone otherthan the producer or the consumer (a 3rdparty) or, • a cost or benefit that arises from consumption and falls on someone otherthan the consumer or the producer (a 3rdparty) [Producer and consumer are 1st and 2nd party]

Externality • An externality is a cost or benefit that arises from production and falls on someone other than the producer, or a cost or benefit that arises from consumption and falls on someone other than the consumer. • Examples: industrial air or water pollution, disposal of waste in public places etc. • Externalities can occur in either production (industry pollution) or consumption (drink driving, smoking at public places, drugs and crime).

Externalities • Externalities can either be negative or positive • a negativeexternality imposes an external costs e.g. pollution • a positive externalitycreates an external benefits e.g. education • Goods that produce negative externalities will be overproduced by the market e.g. pollution • Goods that produce positive externalities will be under-produced by the market e.g. education, research, flu and whooping cough vaccinations

Externalities 4 types of externalities are…Negative production externality Positive production externality Negative consumption externality Positive consumption externality • What type of externality? • Exhaust from cars • Immunisations • Cigarette smoking

E.g. Negative Externality RIVER VANDALS The Western Australian (WA) Turf Club admitted spilling highly toxic pesticide into the Swan River causing $750,000 damage. They were fined $8,000 for poisoning more than 4,000 fish. Who is a third party affected?

Property Rights & the Legal System • Externalities arise because of the lack of clearly defined property (ownership) rights. • Property rightsspecify who owns a resource and who has the right to use it. • What was the property issue with the WA Turf Club? • It may be difficult to assign property rights e.g. the atmosphere, the ocean.

Property Rights & the Legal System • The rule of law: The ability of a government to enforce the laws of the country, particularly with respect to protecting private property and enforcing contracts. • The rule of law is essential for economic development. • Entrepreneurs will not risk investing in a business if their property is not protected by law. • Contracts will not be entered into unless they can be enforced.

Government Policy & Externalities • When externalities are significant and private solutions are not found, government may attempt to solve the problem through… • Various forms of regulation(e.g. bans, taxes) to forbid certain behaviours • Ban on semi-automatic weapons • Regulations on toxic pollutants • Smoking in public places (by imposing fines)

Externalities Review Which of the following is not an example of an externality? • Someone drives a car that emits thick black smoke. • Drunk drivers raise everyone’s car insurance premiums. • The price of timber increases as timber workers’ wages increase. • The neighbour’s beautiful front yard increases your home value. Loud music from a neighbour’s party is • a negative externality if you like the music, and a positive externality if you don’t. • a positive externality if you like the music, and a negative externality if you don’t. • a negative externality whether or not you like it. • a positive externality whether or not you like it.

2. Public goods and Common Resources‘The best things in life are free…’ • Most goods in our economy are allocated by markets. • For these goods, prices are the signals that guide the decisions of buyers and sellers. • When a good does not have a price attached to it, private markets cannot ensure that the good is produced and consumed in the ‘optimal’ amounts. • In such cases, government intervention can potentially remedy the market failure and raise economic well-being.

Two concepts to categorise the various goods in our economy: Excludabilityand Rivalness Excludability • A good is excludable if it is easy to excludesomeone from using it . • Most goods and services use the price system to exclude nonpayers. • Laws recognise and enforce private property rights.

Two concepts to categorise the various goods in our economy: Excludability and Rivalness Rivalness • A good is rivalif the consumption of the good by one person preventsthe consumption available to others. • Nonrivalmeans consumption by one does not reduce consumption for others.

Types of Goods • Private Goods e.g. any store bought good: food, clothing, appliances • Public Goods e.g. national defence, lighthouse, road system, fireworks display, free to air broadcast radio & TV • Quasi Public Goods • Common Resources Available free of charge to anyone who wishes to use them. Rival goods because one person’s use of the common resource reduces other people’s use.

Four Types of Goods Common Resources Private Good Fish in ocean Endangered wildlife Atmosphere Public Park Clean air and water Food Car House Running Shoes RIVAL Quasi-public goods Public Goods Pay TV service, Toll road (e.g. in Ireland) NON RIVAL Lighthouse, Street lighting National defence EXCLUDABLE NONEXCLUDABLE

Public Goods & Free Riders • The Private Market will fail to provide public goods … Why?? • The free rider problem is no incentive for people to pay for what they consume • free riders make it difficult for private markets to supply the socially desirable quantity. • Public Provision • Government can pay for public goods through taxation or monetising debt (at the Federal level)

Common Resources and the tragedy Tragedy of the Commons- the absence of incentive to prevent the overuse and depletion of a commonly owned resource e.g. a fishery. • When a person uses a common resource, he or she diminishes other people’s enjoyment of it.

3. Asymmetric Information The AI alternative • Market participants typically have imperfect informationon the attributes of the products and services they’re transacting. • “even a small amount of information imperfection [can] have a profound effect on the nature of the equilibrium.” (Joseph Stiglitz, Nobel Prize Lecture) The traditional microeconomic model • Market participants have near perfect information on the attributes of the products and services they’re transacting. • Unregulated markets should deliver efficient outcomes, in the sense that participants’ interests are maximised through trade.

Asymmetric Information Is a situation where one party to a market transaction knows morethan the other party, causing market failure. A produceror marketer may know more about the quality of the product he/she is selling than the consumer does • A worker may know more about his/her true ability & efforts than a potential employer does • Examples: Used car market: who has better information, buyers or sellers? • Insurance markets: who has better information, buyers or sellers

Asymmetric Information The situation in which one party to an economic transaction has less information than the other party. Three (3) examples of how asymmetric info causes inefficient market outcomes: • Used car market: who has better information, buyers or sellers? • Insurance markets: who has better information, buyers or sellers? • Credit markets: who has better information, borrowers or lenders?

Example 1:Adverse Selection in USED CAR MARKET LEMONS Problem in the used car market • Some cars are good quality and worth a high price. • Other cars are lemons. • Sellers have more information on the quality of their cars than do buyers. • Buyers don’t know with certainty which cars are ‘lemons’. Asymmetric Info

Asymmetric Information :one party having more information than the other Producers know more than consumers. Consumers buy poor / unsafe products Employers know more than employees about working conditions. People work in wrong occupations Purchasers of insurance know more about risks than do providers of insurance (adverse selection, moral hazard). Asymmetric information occurs in product and factor (labour and capital) markets 4-40

Example 1:Adverse Selection in USED CAR MARKET • High-quality cars are driven out of the market. The market becomes characterised by too many lemons and too few ‘plums’. • Buyers are left with an undesirable or oversupplyof “lemon” used cars

Asymmetric Info 0 Example 2:Adverse Selection in INSURANCE • Buyers of health insurance know more about their health than insurance companies. • People with hidden health problems have more incentive to buy insurance policies. • So, prices of policies reflect the costs of a sicker-than-average person. • Higher premiums discourage healthy people from buying insurance.

Asymmetric Info Example 3: Adverse Selection in CREDIT markets Nature of problem: • Lenders have less information on the credit worthiness of borrowers than the borrowers do. • Low-risk – ‘deserve’ low interest rates • High-risk – should pay higher rates • Lenders don’t know with certainty which borrowers are high/low-risk

Example 3: Adverse Selection in CREDIT markets • Adverse selection occurs in financial markets when • the potential borrowers who are the most likely to produce an adverse outcome—the ‘bad credit risks’—are the ones most likely to be selected (for the loan, credit). This knowledge uncertainty makes it much harder for lendersto screenthe good from the badcredit risks. • Lenders may decide to lend less (or not at all) to business. This creates major source of supply problems and lack of liquidity.

Ways of Reducing Adverse Selection Invest in the acquisition of information… • Car Market – consumers need to do homework (research, learn from other’s experience and seek advice etc.) • https://www.choice.com.au/transport/cars/new/buying-guides/cars • https://www.choice.com.au/transport/cars/used/buying-guides/cars • Regulations requiring minimum warranties (free repairs on the car for a specified time period after purchase) helps to address the problem of adverse selection in the used car market. • Insurance market – e.g. applicants for health insurance may undergo medical examinations/submit medical records. • Credit market – e.g. credit history checks

0 Moral Hazard – Hidden Actions • Moral hazard: a person may change behaviour in a negative way aftera transaction has taken place because his/her actions cannot be monitoredby the other party to the transaction. • Workers sometimes shirk their responsibilities because their employer cannot continually monitor their effort and performance. • Someone whose property is insured may not try as hard to protect it from theft/damage. • While the parents are out, the babysitter may spend more time watching DVDs than watching the children.

Moral hazard in financial markets • Every firm knows more about its financial situation than does any potential investor. Investors are usually reluctant to buy shares or bonds of firms unless comprehensive information is available. • Principal-agent problem: The problem caused by an agent, such as a company manager, pursuing their own interests rather than the interests of the principal who hired them, such as the company shareholders. • Moral hazard also occurs when an agent (borrower) is in conflict with the principal (lender). Agents could have an incentive to: • misallocate funds to personal use (e.g. via offshore banking accounts) • invest in projects with high risk • invest in low yield projects (e.g. for status, etc.)

0 Review: Asymmetric information For each situation below, identify whether the problem is moral hazardoradverse selection • ‘Quality Hi-Fi’ sells home theater sound systems over the Internet and offers to refund the purchase price and shipping if the buyer is not satisfied. • Landlords require tenants to pay security deposits. Asymmetric information is more of a problem when: • getting married. • selling health or life insurance. • buying a used car. • buying a new car.