Download

1 / 8

80 likes | 157 Vues

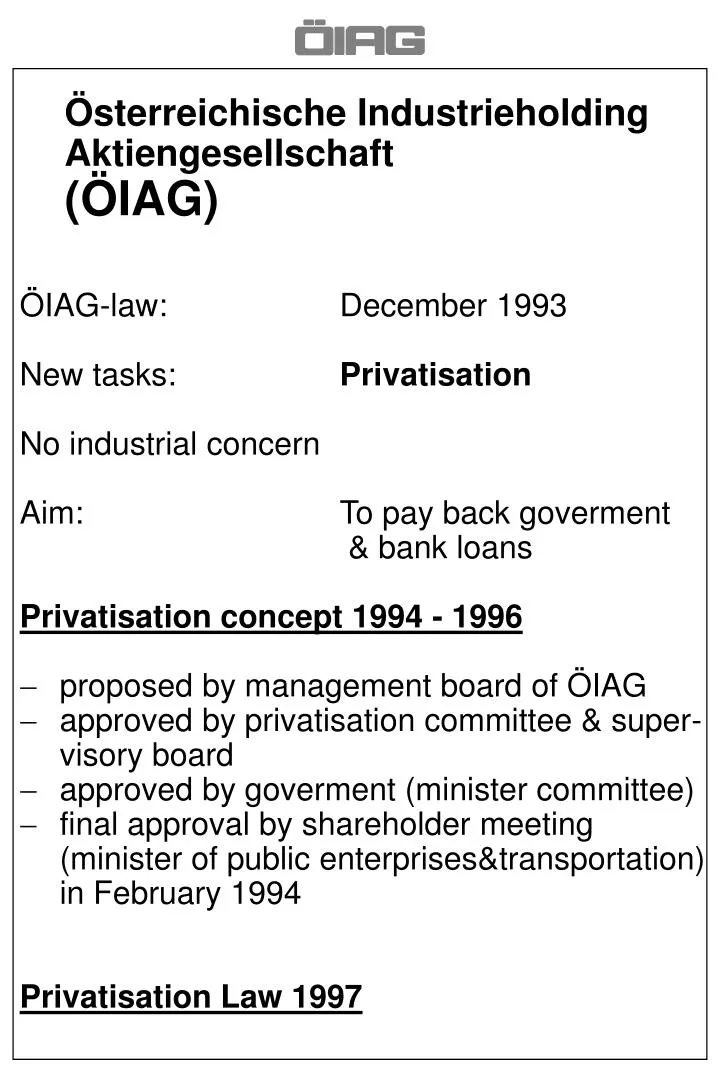

Österreichische Industrieholding Aktiengesellschaft (ÖIAG). ÖIAG-law: December 1993 New tasks: Privatisation No industrial concern Aim: To pay back goverment & bank loans Privatisation concept 1994 - 1996 proposed by management board of ÖIAG

E N D

Österreichische Industrieholding Aktiengesellschaft (ÖIAG) • ÖIAG-law: December 1993 • New tasks: Privatisation • No industrial concern • Aim: To pay back goverment • & bank loans • Privatisation concept 1994 - 1996 • proposed by management board of ÖIAG • approved by privatisation committee & super-visory board • approved by goverment (minister committee) • final approval by shareholder meeting (minister of public enterprises&transportation)in February 1994 • Privatisation Law 1997

ÖIAG - PRIVATISATION PROCEDURE • 1.Decision on WAY of Privatisation • IPO (selling old shares) • IPO + capital increase (selling old and new • shares) • Sale to strategic Investor • 2.Preparatory Work • Restructuring/Regrouping • Transforming business into separate legal • entities • turn around profitability • 3.Privatisation Process • IPO Strategic Sale • 4. AIM: High Proceeds • Preserving Austrian Interests

to 1. How does ÖIAG proceed in privatising? • -Stock exchange • -selling to strategic investors • -MBO/MBI • First you have to decide in which way you want to privatise your firms: • wether you want to make an IPO • i.e. you sell the shares to the public on the • stock exchange • or you combine an IPO with the infusion of new • equity capital into the firm to privatise: • i.e.: you sell old shares and issue new shares • that are only bought by the public • in this case the owner (=state) doesn´t get • as much money as in the case of selling only • old shares and you only go this way if the • companies needs fresh money. • The thus enhanced value can later be realised in a secondary public offering by the owner • or you want to sell the companies to a strategic • owner (because it is too small or not interesting • (profitable) enough for the stock market.

to 2.Having decided on the kind of privatisation • Procedure • Preparatory work: • restructuring and /or regrouping of companies: • transforming business into seperate legal entities • giving them the matching legal form (public or • limited companies). • to make the turn around before privatising is in most cases is advisable, unless you don´t have the managerial know how to do it.

IPO Privatisation • select an international and a national investment • bank as lead manager who are responsible for the issue • make the prospectus due to the publication requirements of the international stock market • valuation according to the rules of the SEC in the various countries you want to float the company´s shares • organise the PR-publicity campaign of the issue • (road shows and one - on - one meetings with potential investors in your country and abroad • Sale to a strategic investor • selection of an investmentbank or corporate advisor who monitors- and accompanies the privatisation process. • valuation (by an auditor or investment bank) • selling memorandum ( investment bank) • list of potential buyers (longlist-shortlist) • send the information memorandum to selected buyers (against signing of a confidentialy agreement) • dataroom - first round • selecting one or two potential buyers with the best offer • exclusive bargaining • exclusive dataroom insight • signing of a contract • preservation of Austrian interests

IPO / Stock Market privatisation • 1. Select investment investment bank(s) • as lead manager(s) • 2. Prospectus • 3. Valuation (SEC-rules) • 4. PR + publicity campaign • road shows/one on one • 5. Book building process: Austrian and abroad • 6. Pricing • 7. Subscription period

SALE TO A STRATEGIC INVESTOR • 1. Select investment bank or corporate advisor • 2. Valuation (Auditor or Investment Bank) • 3. Information (Selling) memorandum • 4. List of potential buyers: Long-/Short list • 5. Confidentiality Agreement • 6. Data room • 7. Select best bid • bargaining with best bidders on the basis of a contract drafted by ÖIAG • signing • closing

AUSTRIAN INTERESTS & ECONOMIC PERFORMANCE • SECURING: Workforce • Production • Future (expansion) of the company • high proceeds • AUSTRIAN INTERESTS:to keep production facilities and work force in Austria • (to countervail de- industrialisation) • AUSTRIAN OWNERSHIP: to keep strategic industrial control in Austria