Contribution Margin Ratio

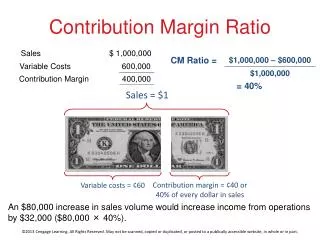

Contribution Margin Ratio. Sales $ 1,000,000. CM Ratio =. Variable Costs 600,000. Contribution Margin 400,000. = 40%. Sales = $1. $1,000,000 – $600,000. $1,000,000. Variable costs = ¢60.

Contribution Margin Ratio

E N D

Presentation Transcript

Contribution Margin Ratio Sales $ 1,000,000 CM Ratio = Variable Costs 600,000 Contribution Margin 400,000 = 40% Sales = $1 $1,000,000 – $600,000 $1,000,000 Variable costs = ¢60 Contribution margin = ¢40 or 40% of every dollar in sales An $80,000 increase in sales volume would increase income from operations by $32,000 ($80,000 × 40%).

Contribution Margin Ratio • 60% of $80,000 increase in sales will go to variable costs and the remaining 40% will go to contribution margin. • The increase in contribution margin will flow to income from operations as fixed costs do not change with increase in sales.

Unit Contribution Margin • Useful when an increase/decrease in sales volume is measured in units (not dollars). Unit Contribution Margin = Sales Price per Unit – Variable Cost per Unit

Unit Contribution Margin • If sales increases by 15,000 units, from 50,000 units to 65,000 units: Sales Price/Unit $20 Unit Variable Cost 12 Unit Contribution Margin $ 8

Learning Objective 3 Determine the break-even point and sales necessary to achieve a target profit

Break-Even Point • Level of operations where revenues and costs are the same. • Useful in business planning, especially when increasing or decreasing operations.

Fixed Costs = $90,000 Selling price per unit Variable cost per unit $25 $15 Contribution Margin per unit $10 Break-Even Point Fixed Costs UCM $90,000 $10 = 9,000 units = Break-Even Sales (Units) =

Break-Even Point $90,000/$10 = 9,000 units needed to break even

Effect of Changes in Fixed Costs There is a direct relationship between total fixed costs and break-even units.

Effect of Changes in Fixed Costs How would a $100,000 increase in fixed costs affect the break-even sales units? Now: $600,000/$20 UCM = 30,000 break-even Proposed: $700,000/$20 UCM = 35,000 break-even

Effect of Changes in Unit Variable Costs There is a direct relationship between unit variable costs and break-even units.

Effect of Changes in Unit Variable Costs How would an extra 2% commission (increase in variable cost per unit) affect the break-even sales units? Now: $840,000/$105 UCM = 8,000 break-even Proposed: $840,000/$100 UCM = 8,400 break-even

Effect of Changes in Unit Selling Price There is an inverse relationship between unit selling price and break-even units.

Effect of Changes in Unit Selling Price How would a $10 price increase affect the break-even sales units? Now: $600,000/$20 UCM = 30,000 break-even Proposed: $600,000/$30 UCM = 20,000 break-even

Target Profit • To find units needed to attain a certain target profit, add the target profit to the fixed costs in the break-even formula. Fixed Costs + Target Profit UCM Break-Even Sales (Units) =

Fixed Costs = $200,000 Target Profit = $100,000 Selling price Per unit Variable Cost Per unit $75 $45 Contribution Margin per unit $30 Calculating Sales (units) Fixed Costs + Target Profit UCM $200,000 + $100,000 $30 = 10,000 units =

Verification of Units Required to Achieve Target Profit Target Profit