Download

1 / 17

180 likes | 211 Vues

Explore consumption and investment decisions based on human and nonhuman wealth, forecasting, and profit evaluations. Understand the impact of current income, expectations, and profit projections on economic decisions.

E N D

Expectations,Consumption,and Investment Chapter 16

16-1 Consumption Total Wealth: Human Wealth +Nonhuman Wealth Human Wealth: the expected present value of after tax labor income Nonhuman Wealth: Financial Wealth + Housing Wealth Financial Wealth: The value of stocks, bonds, checking and savings accounts. Housing Wealth: The value of the house – the mortgage due

16-1 ConsumptionThe very foresighted consumer Consumption depends on total wealth.

The Very Foresighted Consumer • They may not intend to maintain constant consumption over their lifetimes. • The computations involved in planning for constant consumption may be too complicated. • Humanwealth is based on forecasts of future earnings, which may turn out to be less than expected. • Banksmay be unwilling to extend much credit to young adults on the expectation of future earnings.

Towards a more realistic description Consumption depends positively on the total wealth and current after-tax labor income.

Current income, expectations, and consumption • Expectations affect consumption through human wealth (future labor income, taxes and the interest rate) • Expectations affect consumption through nonhuman wealth-stocks, bonds, and housing. • Two main implications for the relation between consumption and income • Fluctuationsin current income are likely to generate less than proportional fluctuations in consumption. • Consumptioncan be affected by changing expectations about the future, even when current income does not change.

16-2 Investment • Investment decision: Firms compare the expected present value of profit from the machine or plant to the cost. • Wear and tear is called depreciation. • The depreciation rate measures how much usefulness the machine loses from one year to the next.

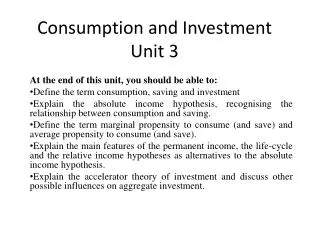

16-2 Investment Figure 16-2 Computing the Present Value of Expected Profits

16-2 Investment Investment depends positively on the expected present value of future profits. The higher the current or expected profits, the higher the level of investment.

A Convenient Special Case Suppose firms expect the future profits and future interest rates toremain at the same level as today (Static expectations). The expected present value of profits is the ratio of the profit rate to the rental cost of capital.

16-2 Investment Investment depends on the ratio of profit to the rental cost. The higher the profit, the the higher the level of investment. The lower the rental cost, the higher the level of investment.

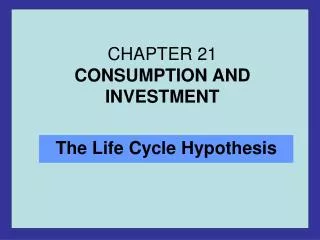

16-2 Investment Figure 16-3 Changes in Investment and Changes in Profit in the United States, since 1960

Current versus expected profit • The firm may be reluctant to borrow if current profit is low. • Even, if the firm wants to invest, it might have difficulty borrowing. • Investment depends both on the expected present value of profits and on the current level of profit.

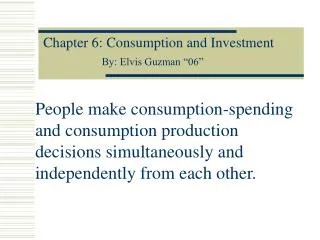

Profit and Sales What determines profit per unit of capita? The level of sales The existing capital stock Profit per unit of capital is an increasing function of the ratio of sales to the capital stock.

16-2 Investment Figure 16-4 Changes in Profit per Unit of Capital versus Changes in the Ratio of Output to Capital in the United States, since 1960

Appendix: Derivation of the Expected Present Value of Profits under Static Expectations