Download

1 / 14

140 likes | 300 Vues

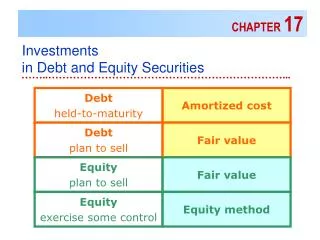

CHAPTER 17. Investments in Debt and Equity Securities. ……..…………………………………………………………. Debt held-to-maturity. Amortized cost. Debt plan to sell. Fair value. Equity plan to sell. Fair value. Equity exercise some control. Equity method. DEBT SECURITIES. Held-to-maturity.

E N D

CHAPTER 17 Investments in Debt and Equity Securities ……..…………………………………………………………... Debt held-to-maturity Amortized cost Debt plan to sell Fair value Equity plan to sell Fair value Equity exercise some control Equity method

DEBT SECURITIES • Held-to-maturity intent and ability to hold security until it matures • Trading held primarily for sale in the near term • Available-for-sale none of the above

HELD-TO-MATURITY SECURITIES Periods Rate PV Annuity FV AD? 1/1/03 1/1/03 Purchased a $50,000, 10% bond for $51,388. The bond pays semiannual interest and matures 7/1/04. Most firms do not record separate premium or discount.

7/1/03 Effective interest = 8% Date Cash Rec’d Interest Rev. Premium Amortiz Carrying Amount 1/1/03 $51,388 7/1/03 1/1/04 7/1/04

Date Cash Rec’d Interest Rev. Premium Amortiz Carrying Amount 1/1/04 2,500 2,038 462 50,482 7/1/04 2,500 2,018 482 50,000 6/1/04 12/31/03 6/1/04 Sold bond for $50,050 plus $2,083 accrd interest.

AVAILABLE-FOR-SALE SECURITIES Date Cash Rec’d Interest Rev. Premium Amortiz Carrying Amount 6/30/02 12/31/02 6/30/02 Purchased a $20,000, 4-year, 7% bond for $18,681 (effective yield=9%). 12/31/02 700 841 141 18,822

1/1/03 12/31/02 12/31/03 12/31/02 Fair value = $19,340; carrying amount = $18,822. 1/1/03 Sold bonds for $19,440. 12/31/03 Adjust fair value adjustment account.

Adjusting Securities to Fair Value • Securities Fair Value Adjustment (AFS) is an asset valuation account that is added to or subtracted from the Available-for-Sale Securities account. • Unrealized Holding Gain or Loss - Equity is reported as part of Other Comprehensive Income. • The year-end adjustment will eliminate any unrealized gains or losses accumulated in the Securities Fair Value Adjustment (AFS) account related to securities that have been sold.

TRADING SECURITIES • Similar to available-for-sale securities, except unrealized gains and losses are closed to net income. 12/31/02 Secur FV Adjustment (Trading) 518 Unrealiz Holding G/L - Income 518

EQUITY SECURITIES • Holdings of less than 20% • fair value method • AFS or trading Accounting treatment the same as with debt securities. • Holdings between 20% and 50% • equity method • Holdings of more than 50% • consolidated statements

HOLDINGS BETWEEN 20% AND 50% • Investor is presumed to exercise “significant influence” if holding 20% or more of voting stock. • Unless there is evidence to the contrary. • Investment: • recorded at cost • not adjusted to market price • increased by share of net income (revenue distinguished from extraordinary G/L) • decreased by amortization of excess of cost over share of book value • decreased by amount of dividends received

OTHER REPORTING ISSUES Financial Statement Presentation Notes for AFS & Held-to Maturity • Total fair value, unreal holding G/L, amortized cost • for each major security type • Summary info. about debt maturities Notes for Equity Method Investments • Name of investee & % ownership • Underlying equity (if different from carrying value) • Fair value

Sec FV Adjust 1,400 Trading Secur 50,000 Loss: Sale of Sec Unreal Hold G/L Reclassification Adjustments 10,000 1,000 40,000 400 600 1,000 Other comprehensive income Total holding gains for period Less: Reclass adj for losses included in net income

Sec FV Adjust 1,400 Trading Secur 50,000 Impairment of Value • If decline in value in not temporary, record impairment. 2/1/07 Loss on Impairment 1,400 Sec FV Adjust 1,400 Unrealiz Hold G/L 1,400 Trading Securities 1,400