Download

1 / 9

90 likes | 185 Vues

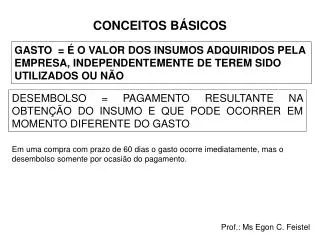

CONCEITOS BÁSICOS. GASTO = É O VALOR DOS INSUMOS ADQUIRIDOS PELA EMPRESA, INDEPENDENTEMENTE DE TEREM SIDO UTILIZADOS OU NÃO. DESEMBOLSO = PAGAMENTO RESULTANTE NA OBTENÇÃO DO INSUMO E QUE PODE OCORRER EM MOMENTO DIFERENTE DO GASTO.

E N D

CONCEITOS BÁSICOS GASTO = É O VALOR DOS INSUMOS ADQUIRIDOS PELA EMPRESA, INDEPENDENTEMENTE DE TEREM SIDO UTILIZADOS OU NÃO DESEMBOLSO = PAGAMENTO RESULTANTE NA OBTENÇÃO DO INSUMO E QUE PODE OCORRER EM MOMENTO DIFERENTE DO GASTO Em uma compra com prazo de 60 dias o gasto ocorre imediatamente, mas o desembolso somente por ocasião do pagamento. Prof.: Ms Egon C. Feistel

DESPESA = VALOR DOS INSUMOS NÃO IDENTIFICADOS COM A PRODUÇÃO E QUE SÃO CONSUMIDOS PARA O FUNCIONAMENTO DA EMPRESA. CUSTO = VALOR DOS INSUMOS USADOS NA FABRICAÇÃO DOS PRODUTOS DA EMPRESA. As despesas são diferenciadas dos custos pelo fato de estarem relacionadas com a administração geral da empresa, ao passo que os custos estão ligados à produção.

CONCEITOS BÁSICOS PERDA = VALOR DOS INSUMOS CONSUMIDOS DE FORMA ANORMAL E INVOLUNTÁRIA DESPERDÍCIO = VALOR DOS INSUMOS UTILIZADOS DE FORMA NÃO EFICIENTE. INVESTIMENTO = VALOR DOS INSUMOS ADEUIRIDOS (GASTO) PELA EMPRESA NÃO UTILIZADOS NO PERÍODO, OS QUAIS PODERÃO SER EMPREGADOS EM PERÍODOS FUTUROS. (QUE ORIGINA BENEFÍCIOS EM PERÍODOS FUTUROS) Prof.: Ms Egon C. Feistel

CUSTOS DE PRODUÇÃO OS CUSTOS DE PRODUÇÃO, OU CUSTOS, SÃO A SOMA DOS CUSTOS DE MATÉRIA-PRIMA (MP) MÃO-DE-OBRA DIRETA (MOD) E CUSTOS INDIRETOS DE FABRICAÇÃO (CIF) CUSTOS = MP + MOD + CIF Prof.: Ms Egon C. Feistel

MATÉRIA-PRIMA RELACIONAM-SE COM OS MATERIAIS COMPONENTES DO PRODUTO ACABADO QUE PODEM SER RELACIONADOS A ELE DE FORMA CONVENIENTE Alguns materiais pouco relevantes em termos de custos, como parafusos, pregos, etc, podem ser considerados materiais de consumo. Prof.: Ms Egon C. Feistel

MÃO-DE-OBRA DIRETA TRABALHO HUMANO QUE ESTÁ NITIDAMENTE RELACIONADO COM A FABRICAÇÃO DO PRODUTO, PODENDO SER FACILMENTE ATRIBUÍVEL A ELE Trabalhadores em atividade de suporte, como supervisores, são denominados mão-de-obra indireta. Prof.: Ms Egon C. Feistel

CUSTOS INDIRETOS DE FABRICAÇÃO TODOS OS OUTROS CUSTOS DE PRODUÇÃO, COM EXCEÇÃO DA MATÉRIA-PRIMA E DA MÃO-DE-OBRA DIRETA, SÃO DENOMINADOS CUSTOS INDIRETOS DE FABRICAÇÃO Prof.: Ms Egon C. Feistel

CUSTOS DE TRANSFORMAÇÃO OS CUSTOS DE TRANSFORMAÇÃO (CT) SÃO A SOMA DOS CUSTOS DE MÃO-DE-OBRA DIRETA (MOD) e CUSTOS INDIRETOS DE FABRICAÇÃO. CT = MOD + CIF Prof.: Ms Egon C. Feistel

EXERCICIO Vendas do ano $275.000,00 Estoques no início do ano: Matéria-prima $3.500,00 Produtos em processo $4.200,00 Produtos acabados $6.800,00 Estoque no fim do ano: Matéria-prima $3.750,00 Produtos em processo $5.800,00 Produtos acabados $8.500,00 Compras de MP no ano $108.000,00 Custos de mão-de-obra $64.500,00 Os custos indiretos de fabricação foram 2/3 do custo da mão-de-obra. Despesas: De vendas = 10% das vendas Administrativas = 5% das vendas Preparar o demonstrativo de resultados para o ano encerrado em 31-12-03 Prof.: Ms Egon C. Feistel