GLOBAL SLOWDOWN AND EMERGING MARKETS

170 likes | 305 Vues

GLOBAL SLOWDOWN AND EMERGING MARKETS. New relations on the global markets. Aleš Cantarutti. Global slowdown and emerging markets.

GLOBAL SLOWDOWN AND EMERGING MARKETS

E N D

Presentation Transcript

GLOBAL SLOWDOWN AND EMERGING MARKETS New relations on the global markets Aleš Cantarutti

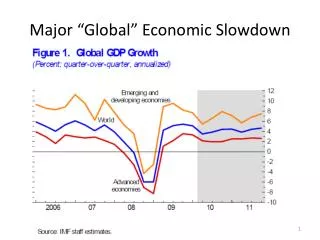

Global slowdown and emerging markets FACT: The collapse in global demand in 2009 brought on by the biggest economic downturn in decades - the biggest contraction of world trade in volume terms since the Second World War “For the last 30 years trade has been an ever increasing part of economic activity, with trade growth often outpacing gains in output. Production for many products is sourced around the world so there is a multiplier effect — as demand falls sharply overall, trade will fall even further. The depleted pool of funds available for trade finance has contributed to the significant decline in trade flows, in particular in developing countries” Pascal Lamy Director-General of WTO Source: OECD National Accounts.

Global slowdown and emerging markets Reasons for trade contarctions • Fall-off in demand is more widespread than in the past; all regions of the world economy are slowing at once • Increasing presence of global supply chains in total trade;goods cross many frontiers during the production process and components in the final product are counted every time they cross a frontier • Shortage of trade finance;ensuring the availability and affordability of trade finance • Protection; any rises in protection threatens the prospects for recovery and prolong the downturn

Merchandise trade: leading exporters and importers, 2008 ($bn and %) Source: WTO a. Secretariat

Growth in the volume of world merchandise trade and GDP, 1998-2008Annual % change Source: WTO Prices of selected primary products, January 1998 — January 2009 Index, January 2002=100 Source: IMF

New relations on the global markets FACT: Not only is the worldwide slowdown hurting developed economies more than emerging economies, but it’s affecting the latter differently and substantively - altering their role in the global economy. Great crisis is forcing change at three levels LEVEL 1 Developing countries are becoming relatively bigger markets; “Emerging markets will account for a larger share of the world’s output when the recession ends than when it began. That will make them even more attractive.” Antoine van Agtmael, Investment firm Emerging Markets Management

New relations on the global markets LEVEL 2 Governments are reshaping the contours of economic development even as they stoke growth through monetary and fiscal policy measures; China used the $586 billion stimulus package to influence demand and supply in 10 industries that together account for 50% of the country’s GDP. “The government calls it a stimulus, but it’s really redesigning industries. That’s why 9% GDP growth in China tomorrow won’t be yesterday’s 9% growth,” David Michael, Greater China head of the consulting firm BCG LEVEL 3 Competition in developing countries has become more intense; With exports shrinking, companies in those countries are concentrating more on growing their sales at home. The rivalry is particularly heated in markets for commodities, such as steel, cement, and aluminum, and for upmarket and middle-market consumer segments.

New relations on the global markets FACT: Companies in emerging markets have started responding to the challenges these changes pose and many of them saw the downturn coming and modified their strategies quickly. • They have an edge because they’re the world’s cheapest manufacturers and don’t need to develop low-cost business models • Before the downturn, rising resource costs and appreciating currencies had eaten away at their profit margins - the recession as a pretext to do some spring cleaning and reduce costs “Between 1995 and 2008, Indian companies grew so quickly that many bad habits crept into their operations. They’re trying to eliminate them. After more than a decade of growth, they are taking a breather to restrategize,” Nirmalya Kumar, London Business School.

Emerging Strategies to Beat the Slowdown • What are many emerging giants doing? • Restructuring portfolios, halting iffy diversification plans, and consolidating operations • Introducing quality systems so that they can manufacture better products at a lower cost • Companies are taking a hard look at talent and firing (or not hiring) and halting bonuses and raises to freeze salary bills at last year’s levels • Using the cash they’ve freed up to develop value-for-money products and services CHINA INDIA Manufacturers are using Tata Motors the slackening of demand low-cost as an opportunity to developinovations advanced products of their own, so that they won’t always have to serve as subcontractors. “Some costs, like talent costs, are lower today, so it’s a good time for companies to invest in developing innovation capabilities,” Peter Williamson, University of Cambridge’s Judge Business School

New relations on the global markets FACT: Most Western companies are preocupied with the crisis in their home markets but they need to start focusing on the next phase of global growth. THEY MUST TRACK FIVE TECTONIC SHIFTS THAT ARE EMANATING FROM THE DEVELOPING WORLD • A GROWING DIVIDE • THE RETURN OF FAMILY-STYLE LEADERS • A REVERSAL IN M&A • HIGHER STAKES IN SUSTAINABILITY • THE CALL OF AFRICA

New relations on the global markets SHIFT 1 A GROWING DIVIDE • Developing countries are trying to reduce their economies’dependence on international trade – concetration on boosting domestic demand • The developing nations have dicovered one another – trade between emerging markets accounted for 40% of their export and import in 2007 (double the level two decades ago) • American-style capitalism VS European-style welfare states – policy makers in the developing world are likely to slow down the pace of deregulation The response: stay focused on emerging markets Western companies must keep investing – advantages in new market segments (rural segment which is tough to break into)

New relations on the global markets SHIFT 2 THE RETURN OF FAMILY-STYLE LEADERS • Crisis as opportunity for new leadership paradigms – in developing countries the new paradigm will come from family businesses (Brazil, India, Mexico, Turkey) and state-owned enterprises (China) • Focus on long-turn pespective, driven by personal pride or national interest • Asia and South Africa; the heads of family-owned businesses have a great deal of power, which enables them to make decisions and modify strategies quickly • China; the leaders of government-run enterprises are powerful (Chinese oil companies and government aid to African nations) The response: Change your leadership criteria Invest in entrepreneurial local managers “For breakthrough performance in developing countries, you need breakthrough leadership” Accenture research report 2009

New relations on the global markets SHIFT 3 A REVERSAL IN M&A • Indian companies set the pace for cross-border deals in 2007 (Tata – Jaguar and Land Rover, Hidalco – Novelis, Mital), but companies from China (Lenovo, TCL), Brazil and Russia will take the lead in the future • Chinese and Latin American companies will use M&A ti internationalize rather than globalize (Brazil – 25 cross-border deals in 2007, Mexico but Indian companies are likely to stalk European companie • Partnerships between emerging giants – China development bank lent $10 billion to Petrobras and $15 to Rosneft (long-term suply of oil) The response: Join forces with emerging giants Western companies need help from local companies to go into China’s hinterland or Indian’s rural market – partnering with emerging giants and offering them knowledge and assets (triangulation strategy); Kawasaki – Bajaj Auto, Telefonica – Huawei Technologies

New relations on the global markets SHIFT 4 HIGHER STAKES IN SUSTAINABILITY • Sustainable solutions are essential to people who don’t have access to water, electricity, or clean air (nonurban markets of China and India) • China imposed tougher emission guidelines – they plan more than 100.000 hybrid, electric and fuel-cell vehicles until 2012, Tata Motors is developing an electric version of the Nano The response: Go green globally Unsutable cascading strategy; cooperatinon with local rivals – launch eco-friendly products all around the world at the same time • ADDITIONAL: China is leading the race for clean energy • China vaulted past competitors from Denmark, Germani, Spain and US to become the world No.1 maker of wind turbines and solar panels – fear from dependence (like oil from the Mideast) • Renewable energy industries are adding jobs rapidly (1.12 mi. in 2008) • RE: 8% of its electricity generation capacity by 2020 (now 4%) • Strategy: to dominate energy-equipment export – government spends $45 billion in 2009

New relations on the global markets SHIFT 5 THE CALL OF AFRICA • Africa: not integrated with much of the developed world, but it does have trading relationships with developing countries • Diferences between African nations – but also common languages, cultures, and trade routes • Several Indian and Chinese companies have found it easy to operate in Africa: Indian immigrants – India-Africa trade $20 billion in 2006 • Investments in Africa: India $2 billion, China $8 billion by 2008 • Africa’s middle class: somewhere betwee 350 and 500 million people – bigger than India’s The response: Tap Africa’s potential It’s time Western multinational companies go on consumer safaris “The future of Guinness may lie not in Ireland’s pubs but in Africa’s bars,” Vijay Mahajan, University of Texsas

New relations on the global markets SHIFT 5 THE CALL OF AFRICA PORTUGAL AREA: 92,090sq. km POPULATION: 10,7 million CAPITAL: LISBON GDP-per capita: 16.100 (2009) GDP growth rate: -3,3% (2009) INFLATION RATE: - 0,9% (2009) UNEMPLOYMENT:9,2% (2009) Labour productivity: 69,5% of EU -27 • ADDITIONAL: PORTUGAL AND AFRICA • Fast development in last two decades: services represent 73,6% of BDP • Export oriented economy: in 2009 export droped for 20% • Export markets in 2009: EU 73,7% (Spain 26,7%, Germany 13,7%, France 12,7%) • Strategy: diversification to emerging markets and Afican markets • Africa: turning toward African countries whose official language is Portuguese (also cultural and history links) • In 2009 Angola absorbed 7,5 of Portuguese export (Mozambique) “Portugal finds itself between the low prices of China, India and Pakistan on the one hand and the design image of Italy and German quality on the other. Portuguese products are not recognised.” Antonio Saraiva, President of CPI

Thank you!Questions? ales.cantarutti@gzs.si