Chapter 4 Job Order Costing

Cost Accounting Foundations and Evolutions Kinney, Prather, Raiborn. Chapter 4 Job Order Costing. Learning Objectives (1 of 3). Contrast the job order and process costing systems and their valuation methods Define what the term ‘job’ means

Chapter 4 Job Order Costing

E N D

Presentation Transcript

Cost Accounting Foundations and Evolutions Kinney, Prather, Raiborn Chapter 4 Job Order Costing

Learning Objectives (1 of 3) • Contrast the job order and process costing systems and their valuation methods • Define what the term ‘job’ means • Explain the purpose of the documents used in a job order costing system

Learning Objectives (2 of 3) • List the journal entries used to accumulate costs in a job order costing system • Identify how technology impacts the gathering and use of information in job order costing systems

Learning Objectives (3of 3) • Explain how standard costs are used in a job order costing system • Describe how job order costing information supports management decision making • Explain how losses are treated in a job order costing system

Job Order or Process Costing Job Order • Small quantities • Batches of identifiable, tailor-made products • User-specific services • Tracks costs by job

Job Order or Process Costing Job Order • Small quantities • Batches of identifiable, tailor-made products • User-specific services • Tracks costs by job Process • Large quantities • Homogeneous goods • Tracks costs by batch of goods by department

Job Order Costing • A job is a single unit or group of units identifiable as being produced to distinct customer specifications • A job can be a • Client • Engagement • Project • Contract

COLA Costing Systems Job order costing Process costing

Product Costing • Cost identification • Cost measurement • Product cost assignment

Methods of Product Costing • Cost Accumulation Systemdefines • cost object • method of assigning costs to production • Valuation Methodspecifies • how product costs will be measured

Job Order Actual Normal Standard Process Actual Normal Standard Six Possibilities V A L M U E A T T H I O O D N COSTING SYSTEM

Actual Actual direct material Actual direct labor Actual overhead Normal Actual direct material Actual direct labor Predetermined overhead Standard Standard direct material Standard direct labor Standard overhead The Difference Valuation Methods

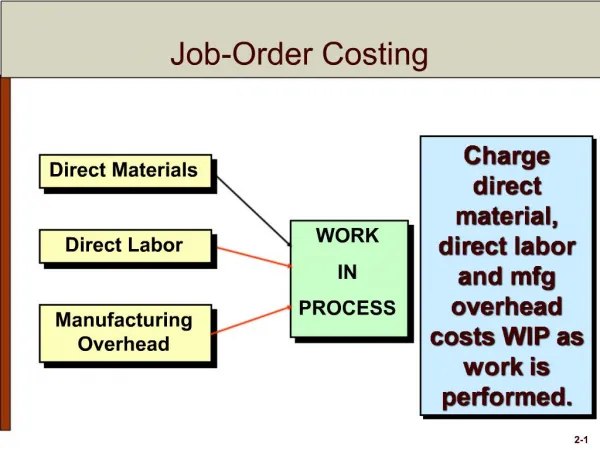

Job Order Costing System • Each job is a cost object • Costs are accumulated for each job • A jobcan consist of one or more units of output • There is a subsidiary ledger for each job

Job 1 Job 2 Job 3 WIP Control Job Order Costing System WIP Subsidiary Ledger = 100 200 500 Job 1 100 Job 2 200 Job 3 500 Total 800 Job 1 + Job 2 + Job 3 = WIP Control

Material Requisition Form • Tracks who is responsible for materials • Verifies flow of materials from warehouse to department to job

Material Requisition Form • Tracks who is responsible for materials • Verifies flow of materials from warehouse to department to job • Journal entry Work in Process Inventory (direct material) Manufacturing Overhead (indirect material) Raw Material Inventory

Materials Requisition Form No. ### Date ___________________ Department _______________ Job No. _________________ Issued by _________________ Authorized by ___________ Inspected by _______________ Received by _____________ Item Part Unit of Quantity Quantity Unit Total No. No. Descrip. Measure Required Issued Cost Cost

Job Order Cost Sheet • All financial information about a job • direct material (from material requisition) • direct labor (from time sheets or labor tickets) • applied overhead • budgeted cost information

Job Order Cost Sheet • All financial information about a job • direct material (from material requisition) • direct labor (from time sheets or labor tickets) • applied overhead • budgeted cost information • When job is complete, use job order cost sheet to analyze actual costs to budgeted costs

Job Order Cost Sheet Customer ____________ Job No. ### Starting Date _________ Job Description ____________ Completion Date ______ Contract Price _____________ Materials Date Ref# Amount Direct Labor Date Ref # Amount Overhead Applied Date Ref# Amount Total Materials _________ Total Labor _________ Total Cost of Job Total OH Applied _________ ========

Employee Time Sheet • Time worked on each job

Employee Time Sheet • Time worked on each job • Journal entry Work in Process Inventory (direct labor) Manufacturing Overhead (indirect labor) Salaries and Wages Payable

Employee Time Sheet Employee Name _______________ Employee No. _______________ Department _______________ For week ending _______ Start Stop Total Type of Work Job No. Time Time Day Hours Employee Signature Supervisor’s Signature

Overhead Account Manufacturing Overhead Actual Overhead Applied Overhead • Journal Entry • Work in Process Inventory • Manufacturing Overhead (applied)

Completion of a Job • Move job cost sheet from WIP subsidiary to Finished Goods subsidiary

Completion of a Job • Move job cost sheet from WIP subsidiary to Finished Goods subsidiary • Journal entry Finished Goods Inventory Work in Process Inventory

Standard Cost System • Actual cost • Normal cost • Standard cost • Predetermined norms (or standards) for materials, labor, and overhead • Compare actual costs to standard costs - difference is a variance

Management Use of Job Order Costing Systems • Estimate future job costs • Establish realistic bids and selling prices • Develop budgets and standards • Compare actual costs to estimated costs • Determine which jobs are profitable • Manage inventory

Product and Material Losses • Shrinkage • Evaporation • Leakage • Oxidation • Production errors • Defects can be economically reworked • Spoilage cannot be economically reworked

Product and Material Losses • Normal Loss – expected during production • Abnormal Loss – exceeds that expected during production

Normal Loss • Anticipated on all jobs • Include cost when calculating predetermined overhead application rate • Include cost less the estimated disposal value • Specific to a job • Applied to the specific job • Include cost less the estimated disposal value

Abnormal Spoilage • Period cost – includes cost of abnormal loss less any disposal value

Product and Material Losses Normal Loss Abnormal Loss Loss for most jobs In overhead rate Period cost Loss identified with a specific job Charge to specific job Period cost

Questions • What is the difference between job order and process costing systems? • How do actual, normal, and standard costing valuation methods differ? • How is the job order cost sheet used?