Download

1 / 18

180 likes | 273 Vues

Learn about job order costing vs. process costing systems, cost flow in manufacturing, job order cost cards, and job costing in service organizations.

E N D

Chapter 17Costing Systems:Job Order Costing Belverd E. Needles, Jr. Marian Powers Sherry K. Mills Henry R. Anderson - - - - - - - - - - - Multimedia Slides by: Dr. Paul J. Robertson New Mexico State University Steve Leask New Mexico State University

Job Order Versus Process Costing OBJECTIVE 2 Distinguish between the different types of product costing systems and identify the information each provides.

Product Costing Systems • Organizations have a range of choices in order to distribute product costs. Two ends of that spectrum are: • Job order costing system. • Process costing system.

Product Costing Systems • The kind of production process that an organization uses determines which of two approaches is used. • Organizations that make large, unique, or special-order products typically use job order costing.

A Job Order • A job order is a customer order for a specific number of specially designed, made-to-order products.

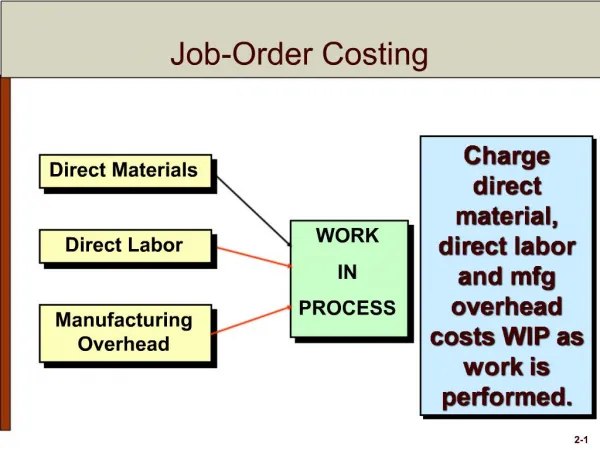

Job Order Costing Systems • Under a job order costing system, the costs of: • direct materials • direct labor • manufacturing overhead • are traced or assigned to specific job orders or batches of products.

Process Costing Systems • Organizations that produce large • amounts of similar products or • liquids that have a continuous • production flow use process costing. • Examples include: • Bricks. • Beverages. • Paper. • Sauces.

Process Costing Systems • Under a process costing system, the cost of direct materials, direct labor, and manufacturing overhead are first traced to processes or work cells and then assigned to the products produced by that process or work cell.

Job Order Costing in aManufacturing Company OBJECTIVE 3 Explain the cost flow in a job order costing system for a manufacturing company.

Job Order Costing System • A job order costing system records information on the following cost flows: • The costs of materials and supplies are first charged to the Materials Inventory Control account and to the respective materials accounts in the subsidiary ledger. • Labor costs are first accumulated in the Factory Labor account.

Job Order Costing System • The various manufacturing overhead costs are charged to the Manufacturing Overhead Control account. • As products are manufactured, the costs of direct materials and direct labor are transferred to the Work in Process Inventory Control account.

Job Order Costing System • Manufacturing overhead costs are applied and charged to the Work in Process Inventory Control account using a predetermined overhead rate. Those charges are used to reduce the balance in the Manufacturing Overhead Control account and increase the Work in Process Inventory Control account.

Job Order Costing System • When products and jobs are completed, the costs assigned to them are transferred to the Finished Goods Inventory Control account. • When the products are sold and shipped, their costs are transferred to the Cost of Goods Sold account.

The Job Order Cost Card OBJECTIVE 4 Prepare a job order cost card and compute a job order’s product unit cost.

The Job Order Cost Card • All costs of • direct materials • direct labor • manufacturing overhead for a particular job are accumulated on a job order cost card.

Job Order Costing ina Service Organization OBJECTIVE 5 Apply job order costing to a service organization.

Job Order Costing in Service Organizations • Job order cost cards for service organizations can be modified to suit their needs, and to determine selling prices in cost-plus contracts. • A significant difference between service and manufacturing organizations is that services are rendered and cannot be held in inventory.

Job Costs in Service Organizations • Job costs in a service organization include: 1. Labor. 2. Materials and supplies. 3. Service overhead.