Job-Order Costing

650 likes | 999 Vues

Job-Order Costing. Process or Job-Order Costing?. Manufacturer of glue textbook publisher An oil refinery Manufacturer of powdered milk Manufacturer of ready-mix cement Custom home builder Shop for customizing vans Chemical manufacturer Auto repair shop Tire manufacturing plant

Job-Order Costing

E N D

Presentation Transcript

Process or Job-Order Costing? • Manufacturer of glue • textbook publisher • An oil refinery • Manufacturer of powdered milk • Manufacturer of ready-mix cement • Custom home builder • Shop for customizing vans • Chemical manufacturer • Auto repair shop • Tire manufacturing plant • Advertising agency • Law office

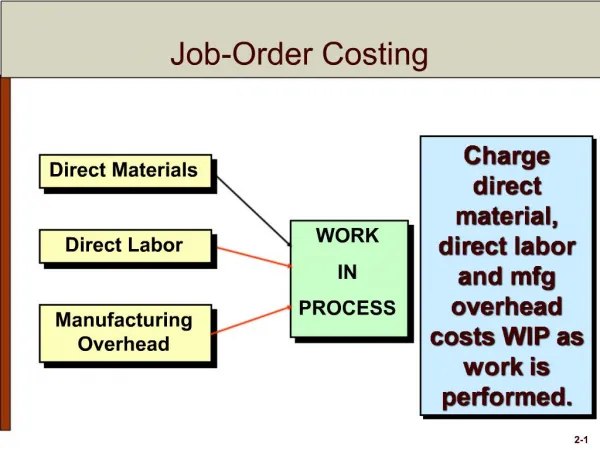

Job Order Cost Components Materials Labor Overhead

Job Cost Sheet #832 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #831 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #830 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Order Cost Components Work In Process Materials Labor Overhead

Job Cost Sheet #832 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #831 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #830 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Order Cost Components Work In Process Materials Labor Overhead

Job Cost Sheet #832 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #831 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Cost Sheet #830 Materials $xxx Direct Labor xxx Manufacturing Overhead xxx Total $xxx Job Order Cost Components Work In Process Materials Labor Overhead

Source Documents • Materials – • Bill of Materials- type and quantity for each unit • Materials Requisition – production for each job • Labor • Time Ticket • For direct labor - hours and rate for each job • Overhead – predetermined OH rate x driver • All summarized on Job Cost Sheet

items being made in this production run Job Cost Sheet OAK & GLASS FURNITURE CO. JOB COST SHEET 831 Product French Court dining tables Date started 4/03/97 Number of units manufactured 100 Date completed 4/21/97 MFG. DIRECT DIRECT LABOR MFG. OVERHEAD DEPT. MATERIALS HOURS COST RATE COST APPLIED Milling & Carving $10,000 70 $14,000 150% $21,000 Finishing 18,000 300 6,000 150% 9,000 COST SUMMARY AND UNIT COSTS

Job Cost Sheet OAK & GLASS FURNITURE CO. JOB COST SHEET 831 Product French Court dining tables Date started 4/03/97 Number of units manufactured 100 Date completed 4/21/97 MFG. DIRECT DIRECT LABOR MFG. OVERHEAD DEPT. MATERIALS HOURS COST RATE COST APPLIED Milling & Carving $10,000 70 $14,000 150% $21,000 Finishing 18,000 300 6,000 150% 9,000 COST SUMMARY AND UNIT COSTS

Let’s take a look at overhead.

Estimated Overhead for the Entire Year Cost Driver Overhead Rate =

$320,000 Cost Driver Overhead Rate =

$320,000 40,000 direct labor hours Overhead Rate =

$320,000 40,000 direct labor hours $8 per dlh =

Cost Driver • Drives the cost up or down with the associated activity • Use the following drivers (there are others) • Direct Labor Dollars • Direct Labor Hours • Machine Hours • Material Dollars

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $1,404 $180 ?

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $1,404 $180 ? $8 per DLH

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $1,404 $180 ? 27 labor hours

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $1,404 $180 ? 27 labor hours x $8

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $216 $1,404 $180

JOB COST SHEET Manufacturing Overhead Direct Materials Direct Labor $216 $1,404 $180 $1,800

Application Exercises 3-1,2,3 • pg 114 • 3-1 Predetermined oh rate • 3-2 Apply overhead • 3-3 Total Cost and unit cost

Three Inventory Accounts • Raw Materials • Work in Process • Finished Goods

Three Costs of any product • Direct Materials • Direct Labor • Overhead • How do costs flow in and out of the three inventory accounts and the three costs

On April 1, Rand Company had $7,000 in raw materials on hand. Another $60,000 was purchased (p. 95). Raw Materials 7,000

On April 1, Rand Company had $7,000 in raw materials on hand. Another $60,000 was purchased (p. 95). Raw Materials 60,000 Accounts Payable 60,000 Raw Materials 7,000 60,000

During April, $52,000 in raw materials were requisitioned. Of these, $2,000 were indirect. Work in Process 50,000 Manufacturing Overhead 2,000 Note that indirect materials are overhead! Raw Materials Work in Process 7,000 30,000 50,000 60,000

During April, $52,000 in raw materials were requisitioned. Of these, $2,000 were indirect. Work in Process 50,000 Manufacturing Overhead 2,000 Raw Materials 52,000 Raw Materials Work in Process 7,000 52,000 30,000 50,000 60,000

Labor cost for April were: direct labor, $60,000; indirect labor, $15,000. Work in Process 60,000 Manufacturing Overhead 15,000 Salaries and Wages Payable 75,000 Raw Materials Work in Process 7,000 52,000 30,000 50,000 60,000 60,000

Rand Company experienced actual overhead costs totaling $40,000. Manufacturing Overhead IM 2,000 IL 15,000

Rand Company experienced actual overhead costs totaling $40,000. Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000

Received a bill for accrued property taxes, $13,000. Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. taxes 13,000

Paid insurance on factory, $7,000. Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. taxes 13,000 Insurance 7,000

Depreciation on factory equipment, $18,000. Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. tax 13,000 Insurance 7,000 Deprec. 18,000

Manufacturing Overhead The debit side of Manufacturing Overhead is the ACTUAL side. IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. tax 13,000 Insurance 7,000 Deprec. 18,000 95,000

Assume that overhead is applied at the rate of $6 per machine hour. During the month, 15,000 machine hours were used on two jobs. By multiplying 15,000 x 6 we arrive at the appliedoverhead amount of $90,000. Manufacturing Overhead

During the month, 15,000 machine hours were used to two jobs. Estimated overhead is $90,000. Manufacturing Overhead Work in Process 90,000 Manufacturing Overhead 90,000

During the month, 15,000 machine hours were used to two jobs. Estimated overhead is $90,000. Manufacturing Overhead Work in Process 90,000 Manufacturing Overhead 90,000 Work in Process 30,000 50,000 60,000 90,000

Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. tax 13,000 Insurance 7,000 Deprec. 18,000 95,000 Applied O/H 90,000 15,000 x $6 The credit side is the “applied” or “estimated” side.

Manufacturing Overhead IM 2,000 IL 15,000 Utilities 21,000 Rent 16,000 Misc. 3,000 Prop. tax 13,000 Insurance 7,000 Deprec. 18,000 95,000 Applied O/H 90,000 You might think of it as the EAST side.

Job A was completed at a cost of $158,000 and transferred to finished goods. Manufacturing Overhead

Job A was completed at a cost of $158,000 and transferred to finished goods. Manufacturing Overhead Finished Goods 158,000 Work in Process 158,000 Finished Goods Work in Process 158,000 30,000 50,000 60,000 90,000 158,000

Three-fourths of the units were sold on account for $225,000. Manufacturing Overhead

Three-fourths of the units were sold on account for $225,000. Manufacturing Overhead Accounts Receivable 225,000 Sales 225,000 The Retail Portion