PROBLEMS

E N D

Presentation Transcript

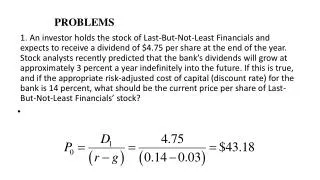

PROBLEMS 1. An investor holds the stock of Last-But-Not-Least Financials and expects to receive a dividend of $4.75 per share at the end of the year. Stock analysts recently predicted that the bank’s dividends will grow at approximately 3 percent a year indefinitely into the future. If this is true, and if the appropriate risk-adjusted cost of capital (discount rate) for the bank is 14 percent, what should be the current price per share of Last-But-Not-Least Financials’ stock?

PROBLEMS 2. Suppose that stockbrokers have projected that Jamestown Savings will pay a dividend of $2.50 per share on its common stock at the end of the year; a dividend of $3.25 per share is expected for the next year, and $4.00 per share in the following two years. The risk-adjusted cost of capital for banks in Jamestown’s risk class is 15 percent. If an investor holding Jamestown’s stock plans to hold that stock for only four years and hopes to sell it at a price of $50 per share, what should the value of the bank’s stock be in today’s market? = $38.14 per share

PROBLEMS 3. Oriole Savings Association has an equity-to-asset ratio of 9 percent which means its equity multiplier must be: In contrast, Cardinal Savings has an equity-to-asset ratio of 7 percent which means it has an equity multiplier of: With an ROA of 0.67 percent Oriole Savings Association would have an ROE of: ROE = 0.67 × 11.11x = 7.44 percent. With an ROA of 0.67 percent Cardinal Savings would have an ROE of: ROE = 0.67 × 14.29x = 9.57 percent In this case Cardinal Savings is making greater use of financial leverage and is generating a higher return on equity capital as compared to Oriole Savings Association.

4. The latest report of condition and income and expense statement for Smiling Merchants National Bank are as shown in the following tables: Smiling Merchants National Bank (complete) Income and Expense Statement (Report of Income) Interest and fees on loans $50 Interest and dividends on securities 6 Total interest income 56 Interest paid on deposits 40 Interest on nondeposit borrowings 6 Total interest expense 46 Net interest income 10 Provision for loan losses 5 Noninterest income and fees 20 Noninterest expenses: Salaries and employee benefits 10* Overhead expenses 5 Other noninterest expenses 2 Total noninterest expenses 17 Net noninterest income -2 Pretax operating income 8 Securities gains (or losses) 2 Pretax net operating income 10 Taxes 2 Net operating income 8 Net extraordinary income -1 Net income 7 *Note: the bank currently has 40 FTE employees.

Using the Report of Income and Report of Condition, calculate the following performance measures: ROE Asset Utilization ROA Equity Multiplier Net Interest margin Tax Management efficiency Net Noninterest margin Expense control efficiency Net Operating Margin Asset Management efficiency Earnings Spread Funds Management efficiency Net Profit Margin Operating efficiency ratio What strengths and weaknesses are you able to detect in Happy Merchant’s Performance?

STRENGTHS AND WEAKNESSES • Strengths: • ROE: Positive value reflects a high rate of return flowing to shareholders. • Net profit margin: Positive value reflects effectiveness of management in controlling cost and service pricing policies. • Asset utilization: Positive value reflects a good portfolio management policies and yield on assets. • Equity multiplier: Positive value reflects efficient financial policies. • Expense control efficiency, asset management efficiency ratio, funds management efficiency ratio, operating efficiency ratio also reflects a high operating efficiency and expense control. • Tax-management efficiency ratio: Positive ratio reflecting the use of security gains or losses and other tax-management tools (such as buying tax-exempt bonds) to minimize tax exposure etc.

STRENGTHS AND WEAKNESSES Weaknesses • ROA: Positive value (0.714%) reflects managerial efficiency and how successful management has been in converting assets into net earnings. Since the positive value is only 0.714% it acts as a weakness for Smiling Merchants National Bank. • Net noninterest margin: Negative value (−0.2%) reflects that net noninterest income is inline with noninterest cost. • Net interest margin: Positive value (1.02%) reflects that management is not successful in achieving close control over earning assets and in utilizing the cheapest sources of funding. Since the positive value is only 1.02% it acts as a weakness for Smiling Merchants National Bank. • Earnings spread: Positive value (0.21%) reflects a high competition, forcing management to try and find other ways to make up for an eroding earnings spread.