Download

1 / 16

160 likes | 418 Vues

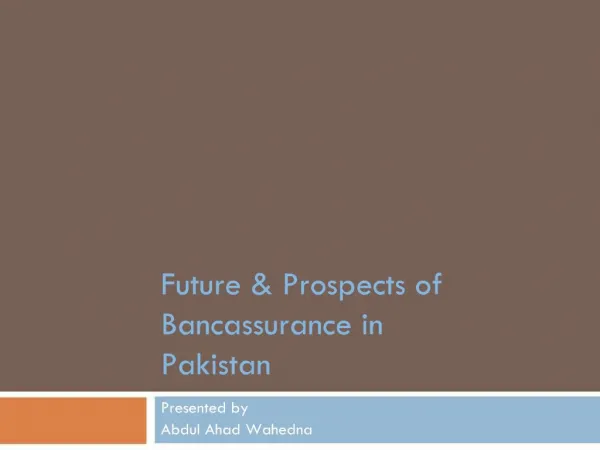

Rise of Bancassurance An Asia experience. International Insurance Society Taiwan, 13-16 July 2008. David Fried Group General Manager Regional Head of Insurance Hongkong and Shanghai Banking Corporation. Contents. Global Drivers Aging population brings in opportunities Bancassurance.

E N D

Rise of Bancassurance An Asia experience International Insurance Society Taiwan, 13-16 July 2008 David Fried Group General Manager Regional Head of Insurance Hongkong and Shanghai Banking Corporation

Contents • Global Drivers • Aging population brings in opportunities • Bancassurance

Saturated Developed Moderately developed Under penetrated Japan South Korea Hong Kong Taiwan Singapore Malaysia Thailand The Philippines Macau China India Vietnam Indonesia Opportunities in Asia Insurance markets in Asia are at different stages of development Bancassurance is the fastest growing channel

Why now? Asia opportunity – paradigm shift in insurance spend as GDP’s hit threshold Life premiums/GDP (%) Potential Taiwan (1978) South Korea Japan (1976) Australia Malaysia Philippines China (1982) India Current penetration of emerging markets Thailand Vietnam (1996) Hong Kong (1990) Singapore Indonesia Real per capita GDP, US$ ‘000 * Data series of penetration start from 1970 unless specified. Real per capita GDP in log scale. Source: Swiss Re Economic Research and Consulting

Emerging Markets comprise 10% of world premiums – skewed to Life Top 10 Countries = 87% of Life Market US$0.33tn Life Top 10 Countries = 64% of GI Market GI

High Bank (Credit) Products Wealth Insurance investment needs Low Youth Mature Client time Evolving customer needs:a Golden Opportunity for BanksOlder customers have different financial needs Financial needs map • Over 50’s possess 70% of all financial assets • These individuals and their assets need protection (insurance) and investing – no longer borrowing • Ageing is [accelerating] this shift as old borrowers de-leverage • Equally applicable in Developed and Emerging Markets • This “sea change” too big an opportunity to miss and should build on HSBC credit credentials

Why now?People are aging Percentage of total population aged 60 years or over in 2050 • … but will have increased significantly in many countries by 2050 Source: UN Population Ageing 2006

Bancassurance - catching on globally.. France:the largest bancassurance market, 62% of new premiums in 2005 earned through bank networks (favourable legislation, taxation)* USA: 1999 legislation allowed insurance sales through banks but the expected revolution hasn’t materialised (low awareness, low growth)* UK: with 20% total premiums collected, bancassurance lags in market penetration (dominance of IFA sales force)* China: >30% of new business from bancassurance (heavily biased by SP products)* Sth Korea: since regulatory changes in 2003, bancassurance has exploded. New Business Apr 2006 through Jan 2007 accounted for 46%collected premiums (heavily biased by SP roducts)* HK: 38% bancassurance weighted penetration in 2007 (legislation, low interest rates, bank expertise)** Others: Vietnam circa 0.5% penetration in 2005, Indonesia circa 20% in 2004 up from 5% in 1998 Malaysia circa 45% in 2005.* • Watson Wyatt Data

New Life Insurance Premium 1998 New Life Insurance Premium 2005/06 China Less than 10% 33.9% Hong Kong 15.1% 33.1% India Negligible 4.61% (15.4% in private sector) S. Korea Nil 47% (unweighted premium) Malaysia 6% 48% Singapore 26% 26% Taiwan 1% 37.5% Bancassurance – a growing success in Asia New Premium from bancassurance as a percentage of total New Premium: Source: various sources, Watson Wyatt and Swiss Re reports

A new distribution channel in addition to the traditional Agency & Direct A tool for deepening banking customer relationships & driving NFI Meeting Stakeholders Needs • A three-way all-win solution • Maximising business performance and potential One-stop shop, holistic solutions Customers Bank Insurer

Integrated bancassurance defines where customers are Private Banking Global Banking and Markets Global Institutions HNWI Corporate Mass Affluent Commercial Banking Personal banking SME Mass Market Global product (Credit Cards)

5. Advisory 2. Co-incidental 2. Co-incidental Products align with different market segments ADVISORY The selling model(s) chosen impacts product, distribution channel, staff selection and training, marketing, sales processes and support etc NEEDS BASED 4. Advanced standalone Sales complexity increases 3. Simple standalone / packaged • As per ‘Advanced Stand-alone’ but formal recommendations made TRANSACTIONAL • Whole life • Endowments • Complex riders • Critical Illness • Income Protection • Unit Linked Life • Annuities 1. Targeted outbound for simple products • Personal Accident • Home Contents • Travel • Basic Term • Mortgage Reducing Term (cross sales for Fire buildings and contents) • Creditor on Credit Cards • Motor (with car loans) • Accidental Death • Personal Accident • Hospital Cash

Key is distribution…. Underwriting automatically follows 65% General Insurance 15% 10% 10% 15% 10% 30% 45% Distribution Manufacturing Client/insured 1 2 3 4 5 6 7 Invest-ments Channel Brand Admin Product U/W Claims Life, Pensions& Investments (LPI) >20% >30% ~10% Return on Equity (ROE) Banks • Develop expertise, understanding and models • Beauty parades, developing JVs and exclusive relationships • Seeking value creation rather than just fee income • Starting to see the value in manufacturing – and building their own Insurers • Support and relationship building with banks • Understanding of banks and their needs • More internal support, blueprints, regional or global academies within companies • Benchmarking against the competition

Align tasks performed with channel functionality A bancassurance model leverages ALL distribution channels for different stages of the sales cycle Lead generation Qualify sale Diary management booking Close sale Post sales service Account management Branches Internet Telephone F2F (FPM’s) Good OK Poor

Different Bancassurance Models Integrated Bank Insurer Agents • Agents to place at bank branches • Mine on bank’s client base - telemarketing • No agent at branches • Bank’s RMs to sell Non -integrated Bank Insurer Bank Insurer Broker’s model Partnership - Leads referral from bank on commercial business; brokers to recommend business Broker Bank