Download

1 / 14

150 likes | 272 Vues

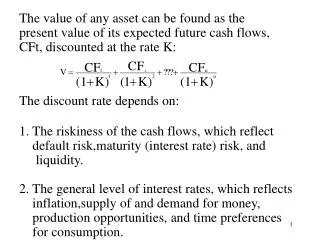

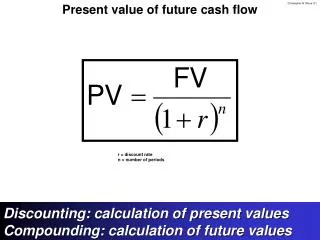

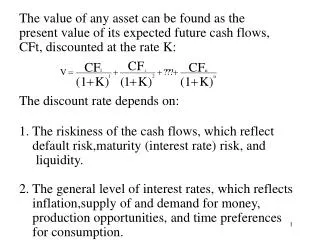

The value of any asset can be found as the present value of its expected future cash flows, CFt, discounted at the rate K:. The discount rate depends on: 1. The riskiness of the cash flows, which reflect default risk,maturity (interest rate) risk, and liquidity.

E N D

The value of any asset can be found as the present value of its expected future cash flows, CFt, discounted at the rate K: The discount rate depends on: 1. The riskiness of the cash flows, which reflect default risk,maturity (interest rate) risk, and liquidity. 2. The general level of interest rates, which reflects inflation,supply of and demand for money, production opportunities, and time preferences for consumption. 1

A. Bond B. Par, or Face, Value; Maturity Value, M C. Coupon Interest Rate; Coupon Payment, INT D. Maturity; Maturity Date E. Call Provision; Call Protection; Call Premium F. Issue Date G. Default Risk H. Kd 2

10% 3

For a constant growth stock, D1=Do(1+g) and Note (1) that g must be constant forever, and (2) that Ks must be >g

ESTIMATED THE CAPITALIZATION RATE IF DIVIDENDS ARE EXPECTED TO GROW AT A CONSTANT RATE, g IF A FIRM EARNS A CONSTANT RETURN ON BOOK EQUITY AND PLOWS BACK A CONSTANT PROPORTION OF EARNINGS, THEN DIVIDEND = g = PLOWBACK X RETURN GROWTH RATE RATION ON EQUITY

WHAT’S PVGO FOR FLEDGING ELECTRONICS? SUPPOSE EPS = 8.33 (RETURN ON EQUITY=.25 EQUITY INVESTMENT=33.33) NOTE: *PVGO IS LARGE BECAUSE FLEDGLING EARNS MORE THAN COST OF CAPITAL(.25>.15) *FLEDGLING’S EARNINGS-PRICE RATIO UNDERSTATES ITS COST OF CAPITAL 8.33/100 = .083 <.15