Download

1 / 26

260 likes | 504 Vues

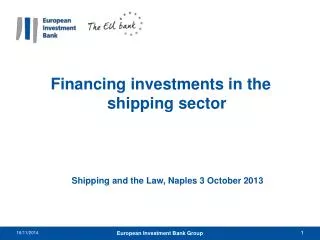

Financing of Infrastructure Investments in Railways. UNIFE/RBF (Rail Business Forum, Poland) Seminar . Lars Hougaard European Investment Bank Warsaw, 11-12 July 2007. European Union Long-term Financing institution to Support EU Objectives. Created by the Treaty of Rome in 1958.

E N D

Financing of Infrastructure Investments in Railways UNIFE/RBF (Rail Business Forum, Poland) Seminar Lars Hougaard European Investment Bank Warsaw, 11-12 July 2007

European Union Long-term Financing institution to Support EU Objectives • Created by the Treaty of Rome in 1958. • Subscribed capital EUR 165 bn by 27 EU Member States. • Operates in: • EU Member, Accession and Candidate States. • New Neighbourhood and Mediterranean Partner Countries. • African, Caribbean and Pacific States. • Asia and Latin America. • Lending in 2006: EUR 45.8 bn (EUR 39.8 bn within the EU-25). • EU Policy-driven Bank, including: • EU Transport Policy, in particular Trans-European Networks. • Economic and Social Cohesion within the EU. • Environmental protection and improvement. • Support for EU development aid and cooperation policies. • EIB lending for Railways total (1996 – 2006) of EUR 49 bn.

EU Initiatives in the Railway Sector • Trans-European Transport Policy Objectives • Improve territorial cohesion. • Boost competitiveness and growth potential of enlarged Union. • Reduce congestion on the major routes. • Encourage intermodality and modal shift to railways. • Extend the European axes concept into Neighbourhood Countries. • Trans-European Transport Investment Programme • Modernise and build new railway lines on 94,000 km. • 17 out of 30 European Priority Projects in the railway sector. • 5 further projects in rail/road projects. • Introduce interoperable European signalling system (ERTMS). • Establishment of six major cross-European freight corridors. • EU funding for rolling stock modernisation in Central and Eastern Europe. • Support for the Railway Sector is a Core Activity for EIB.

Rationale for EIB’s Involvement in the Railway Sector • EIB promotes European Union policy objectives including environmentally friendly means of transport, interoperability and intermodality. • Efficient EU infrastructure network necessary to underpin economic growth, competitiveness, employment and territorial cohesion. • EIB activities extend to: • Institutional policy advice: to EU and other multilateral institutions, industry associations et al to develop sector policies and best practice. • Project up-stream: EIB financial engineering is critical and the EIB’s technical know-how can influence the investment concept. • Project down-stream: EIB’s contribution to the overall financial packages for defined investments. • EIB equipped to assist EU’s Railway Sector to achieve its investment goals.

EIB’s Approach to Railways • Promote an economically viable and financially sustainable restructuring of the sector. • Focus where railways have a competitive advantage: • High speed links. • Urban and sub-urban transport. • Main freight corridors. • Foster multi-modal integration. • Support an EU wide approach to creating a competitive railway system (e.g. TENs, interoperability). • Careful selection of new investment opportunities with project requirements including: • Support EU policies. • Technically sound investments. • Good economics (ERR). • Proper environmental protection (EIA, Nature Conservation, SEA). • Sufficient credit quality. • EIB’s role as a valuable counterpart has broader scope than its financing role and its appraisal methods are well-regarded.

EIB Focus on Future Lending • Priority Trans-European Network. • Other Pan-European Corridors and TEN networks. • Sustainable transport projects with environmental benefits. • Rehabilitation/upgrading vs. new infrastructure. • Signalling systems and interoperability. • Rolling stock and locomotives for passenger and freight. • EUR 40-50 billion required in rail TENs infrastructure by 2020.

Challenges for and Propositions to Europe’s Railways • Challenges • Loss of competitiveness particularly in freight services. • Lower public sector contribution to investments. • Back-log of investment required in rehabilitation/upgrading and new infrastructure, signalling, rolling stock, locomotives, stations… • Lack of interoperability. • Propositions • Focus on priority network needs – HSL, freight corridors, ERTMS signalling. • Improve indermodality. • Increase of private sector participation in the railways where financially viable. • Adaptation of financing structures to the separation of infrastructure and service operators. • Development of new financial products to meet railways’ needs. • Higher private sector investments in railways to create modern and competitive transport alternative to road.

Use of road infrastructure in EU-15 1970 = 100 Source: EC, Eurostat, OECD

Use of road infrastructure in NMS 1995 = 100 Source: EC, Eurostat, OECD

Use of rail infrastructure in EU-15 1970 = 100 Source: EC, Eurostat

Use of rail infrastructure in NMS 1995 = 100 Source: EC, Eurostat

Estimate of Investment Demand for EU’s Railways • TEN-T until 2020 (source EU) • EUR 190 bn in Priority TEN-T. • EUR 380 bn in overall TEN-T Programme. • Urban and light rail over 20 years • EUR 140 bn of which EUR 30 bn in rolling stock. • Top-down approach • EU-15 GDP : EUR 8,545 m in 2000 to EUR 16,900 m in 2030. • EU-25 GDP : EUR 8,940 m in 2000 to EUR 18,020 m in 2030. • “EU-30” GDP : EUR 9,610 m in 2000 to EUR 19,800 m in 2030. • Transport sector investment 1 –1.5% of GDP depending on level of development. • Share of railways in transport sector investments in EU: 30%. • Annual investment demand in European railway sector rises from EUR 30 bn (2000) to EUR 60 bn (2030) in 2000 prices. • How much can be financed by the public sector? • Role and financing capacity of private sector to be developed.

Key Features of Private Sector Participation in the Railway Sector • Increased use of private sector skills for public sector services; each partner does where he/she is ‘best’ at. • Payment related to private partner service delivery. • Whole life approach to design, build, operational maintenance. • Optimal realistic risk sharing and scope for innovation. • Improved ‘value for money’ for the public sector. • Ultimate regulatory authority & responsibility remain in public sector. • Under the right terms and conditions private participation could provide an additional instrument to the traditional way of financing railway investments.

EU Public Investment is declining … US EU Source: OECD

PPPs not turned the trend even in UK Public investment without PPPs Public investment plus PPPs Source: OECD, HMT

The Financial Situation is Changing • Historically, credit risks related to rail infrastructure investments were rarely fully linked to the underlying risk of the project. • Full backing from or ownership by local or national governments. • Many infrastructure owners financed directly through public budget without any possibility to borrow. • Now, situation changing influenced by factors such as: • Liberalising markets • For freight since 1 January 2007. • For passengers : opening of international services expected in 2010. • Privatisation of previously public companies. • Concessions (in the form of PPPs or otherwise). • Off-balance sheet ownership of rolling stock (through leasing higher proportion of fleet). • In the future higher alignment between risk profile of projects to be financed and the structure of the financing solution.

Immediately available instruments for rail infrastructure,rolling stock and innovation • European Commission • The TEN-T funds and Structural / Regional / Cohesion funds. • During the 2007-2013 financial perspective EUR 20 to 30 bn to be allocated to the rail sector. • EIB financing • Particularly favourable terms for Priority TENs project. • Structured Finance Facility enables EIB to engineer customised solutions and take lower graded risk than in the past. • Joint EIB - EU Funding • Eligibility criteria to satisfy EIB and European Commission with Cross-Conditionality (Combined EIB/EU Funding could reach 90%+ of project cost). • Loan Guarantee for Transport TENs • Instrument to reduce traffic revenue risk for private investors in critical ramp-up phase. • Projects eligible under the TEN-T Financial Regulation will be eligible under the Guarantee, provided they benefit from a substantial level of financial support from the Member States and/or other public authorities. • Guarantee will provide security for standby credit facilities aimed at covering post construction risks during the early operational phase. • For viable projects, financing is available – what about project preparation?

Improved Access for Railways to Cohesion Funding through JASPERS

Activities of JASPERS • JASPERS will provide technical assistance from the early stages of a project through to the application for a Commission decision to provide assistance. • Assistance will cover the technical, economic and financial aspects and all other preparatory work required to deliver a mature project. • Objective: to deliver high quality project applications with a view to rapid approval by the Commission. • JASPERS: advice, coordination, develop and review of project structure, removing bottlenecks, filling gaps, identification of problems not addressed (e.g. state aid, EIA), provide DG REGIO with information on project maturity. • Much of the detailed technical work will remain the responsibility of the beneficiary/Member State. • JASPERS will have its own TA framework contract. • Advice on structuring PPPs. • Seeking to facilitate the project preparation phase.

EIB Role in JASPERS • EIB contribution • Long-term loans / favourable lending conditions (AAA-rating + Non-profit seeking). • In-house expertise: >75 project engineers and economists in sectoral departments. • Worldwide experience > 140 countries. • Specialized PPP-Department > 170 PPP-projects . • JASPERS – Organisation • JASPERS Facility managed by EIB. • Separated from the lending activities of the EIB. • Close cooperation with Member States, DG-REGIO counterpart and EBRD in defining priorities and strategy in Annual Action Plans. • Cooperation with EIB’s internal services to assure consistency and specialised expertise (i.e.PPPs). • Most staff will work locally in regional offices close to the needs of Member States. • JASPERS is valuable counterpart for project sponsors.

Scope of JASPERS • Upstream technical assistance in sectors eligible for Cohesion Fund financing: • Trans-European networks. • Transport sector outside of TENs, including rail, river and sea transport, intermodal transport systems and their interoperability, management of road and air traffic, clean urban and public transport. • Environment including water and sanitation, solid waste management, energy efficiency and renewable energy. • Pan-European assistance for best practice and know-how transfer.

Conclusions • The railway sector is one of the core priorities of EU transport policies. • EIB is a committed long-term financier and risk participant of the railway sector. • Competitiveness of the sector depends on availability of competitive services, passenger and freight and rolling stock. • Asset ownership becomes less important than ability to meet user’s need in efficient manner. • Modernised capital markets and financing industry can provide both budget based and risk based innovative financing instruments. • Innovative funding structures need reliable legal base.

Contact: Lars Hougaard Transportation Sector Structured Finance and Advisory +352.4379.7332 (l.hougaard) Email: hougaard@eib.org www.eib.org