Breakeven

370 likes | 469 Vues

Breakeven. Unit 3 Topic 3.2.3. Aims for today. To understand what break even is and how it can be used to assist businesses in their planning. Starter task: Formula recap. Match the formulas. Contribution Break Even in units Margin of safety Total Revenue Profit or loss?.

Breakeven

E N D

Presentation Transcript

Breakeven Unit 3 Topic 3.2.3

Aims for today • To understand what break even is and how it can be used to assist businesses in their planning

Match the formulas • Contribution • Break Even in units • Margin of safety • Total Revenue • Profit or loss? • Selling price x Quantity • Actual production level – break even output • Total revenue – Total costs • Fixed costs/contribution • Selling Price – Variable costs

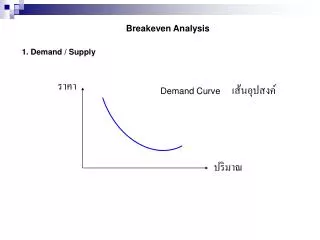

What does break even mean? • Break even is where a firms TOTAL REVENUE is the same as its TOTAL COSTS (In other words, money coming in = money going out). • At the break even point, a firm is neither making a PROFIT nor A LOSS Q: Why would it be useful for a toy manufacturing business to calculate its break even point? To understand the role & purpose of break even analysis

Break even • Break even analysis is useful as a business can work out what volume of sales it needs to achieve to cover its costs. • The key to break even is to work out the contribution made from the sale of each unit. • The amount of money from each unit sold contributes to pay for the fixed and indirect costs of the business.

Break even formula Contribution To understand the role & purpose of break even analysis

Contribution formula Contribution = selling price less variable costs per unit (SP - VC) • Cans of coke = £1 - 0.25 = 0.75 contribution • Fixed costs are £6,000 • BE = FC / Contribution • 6,000 / 0.75 = 8000 Cans need to be sold to break even

A CD factory has the following costs: • Fixed cost: £10,000 • Variable cost: £2 • Selling price: £7 Q: Calculate the break even point in units and the break point in revenue. ANSWER: In units £10,000 / (£7-2) = 2000 units In revenue: £2,000 x £7 = £14,00

Break even point in units = Fixed costs / contribution £10,000 / (£7-2) = 2000 units

Break even point in revenue Quantity at break even x Selling price £2,000 x £7 = £14,00

Calculating the break even point Step 1. Identify fixed & variable costs – add them together to get the TOTAL costs Step 2. Calculate the TOTAL REVENUE To understand the role & purpose of break even analysis

Task 1: Calculating break even To understand the role & purpose of break even analysis

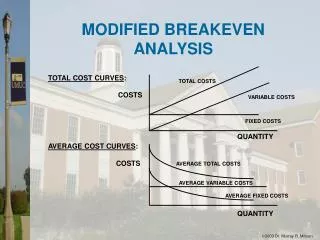

Task 2: Draw the break even chart using your data • Label the vertical axis “sales and costs in pounds”. • Label the horizontal axis “sales/production (units)”. • Draw on the BE point • Draw a horizontal line for total fixed costs. • Starting at the Total costs point, draw the total cost line going through the break even point. • Starting at zero, draw the total revenue line through the break even. • Where the sales revenue crosses the total costs line is the break even point. • Read off the units of sales to give the break even level of sales. • The gap between the total costs line and sales revenue line after the break even point represents the level of profit. To understand the role & purpose of break even analysis

The break even chart To understand the role & purpose of break even analysis

Margin of safety formula • The difference between the planned number of units or actual sales and the number of units of sales at break even point. Cans of coke: They can make: • 10,000 cans potentially – 8,000 actual units at break even • = 2,000 Margin of safety

Task 3: Draw the margin of safety To understand the role & purpose of break even analysis

Extension task: Break even worksheet Complete worksheets: #3 Break Even Analysis #4 Break even charts To understand the role & purpose of break even analysis

Why must businesses understand its break even point? • …because the contribution from every unit sold above the break-even point adds to profit. • The break-even point provides a focus for the business; • It works out whether the forecast sales will be enough to produce a profit and; • Whether or not further investment in the product is worthwhile.

Limitations of break-even charts? • Assumes all stock is sold • Does not take into account possible changes in costs over the time period • Does not allow for changes in the selling price. • Analysis is only as good as the quality of information. • Does not allow for changes in market conditions in the time period – e.g. entry of new competitor.

Task 4 Hot Dogs • Helen & Joe operate a hot dog stand in the town centre. The stand costs £200 per week to hire. Each hot dog needs one bread roll at 20p, one sausage at 25p and sauces at 5p. • The selling price of each hot dog is £1

Complete the table At what quantity do total costs = total revenue? (Break even)What profit is made when they sell 600 hot dogs?

Complete the table At what quantity do total costs = total revenue? (Break even)What profit is made when they sell 600 hot dogs?

Complete the table At what quantity do total costs = total revenue? (Break even)What profit is made when they sell 600 hot dogs?

Task 5 • Draw a Break Even chart for the Hot Dog business - Ensure your chart is FULLY and CLEARLY labelled • Draw on the margin of safety (1) • Explain how the Break even analysis will help Helen and Joe (4) • Discuss what strategies Helen and Joe could use to enable them to reach their break even point quicker (6) • Evaluate which of these strategies would be best for the business (6)

Plenary 1: Break even drag & drop • http://www.businessstudiesonline.co.uk/AppliedGcseBusiness/Activities/Unit3/BreakEven/BreakEvenTermsDragDrop/frame.htm To understand the role & purpose of break even analysis

Break even drag & drop solution To understand the role & purpose of break even analysis

Plenary 2: Break even piggy bank http://www.quia.com/cz/5773.html?AP_rand=331777296 To understand the role & purpose of break even analysis

Contribution Selling Price – Variable costs To understand the role & purpose of break even analysis

Break Even in units Fixed costs/contribution To understand the role & purpose of break even analysis

Break Even Revenue Break Even Quantity x Selling price To understand the role & purpose of break even analysis

Margin of safety Actual production level – break even output To understand the role & purpose of break even analysis

Total Revenue Selling price x Quantity To understand the role & purpose of break even analysis

Total Revenue Selling price x Quantity To understand the role & purpose of break even analysis

Profit or loss? Total revenue – Total costs To understand the role & purpose of break even analysis