Download

1 / 20

200 likes | 282 Vues

Learn how financial institutions can serve as key partners in Individual Development Account programs to empower low-income individuals and families. Presented by Angie Franklin.

E N D

MOKANSaveIndividual Development Account Conference FINANCIAL INSTITUTIONS AS PARTNERS IN IDA PROGRAMS May 8-9, 2003 Presented by Angie Franklin Communities United Credit Union Wichita, KS

WHO CAN ADMINISTER AN IDA PROGRAM? • One or more not for profit 501(c) 3 tax exempt organizations • State or local government agency • Tribal government submitting an application jointly with a not for profit organization • A credit union designated as a low income or CDCU credit union by NCUA • An organization designated as a community development financial institution (CDFI) by the US Treasury Dept

FINANCIAL INSTITUTIONS AS PARTNERS WITH SPONSORING ORGANIZATIONS • Qualifying financial institutions are banks or credit unions that offers consumer financial services and products, that are insured by the Federal Deposit insurance Corporation (FDIC) or the National Credit Union Administration (NCUA). These financial institutions have a stated and demonstrated commitment to the communities in which it does business.

WHAT IS A LOW INCOME CREDIT UNION? • A low income credit union (LICU) is a credit union designated by NCUA to serve a membership of which over 50% of its members annual household income falls at or below 80% of the national median household income.

WHAT IS A COMMUNITY DEVELOPMENT CREDIT UNION? • Community development credit unions are special purpose financial institutions that: • promote economic revitalization and community development • have a designated target market that is either low income or historically underserved by traditional financial institutions: and • is not an entity of the state or local government

WHAT IS A COMMUNITY DEVELOPMENT BANK? • A community development bank (CDB) is an insured bank that: • has a primary purpose of providing capital to rebuild economically distressed communities through targeted lending and investments • provides basic financial services to a targeted population of low income people or others who lack adequate access to financial services

WHAT IS THE CDFI FUND? • The Community Development Financial Institution Fund is a program administered by the U S Dept of Treasury to make capital grants, investments and awards for technical assistance to community development financial institutions.

Personal finance workshops Interest bearing savings accounts Matching Funds Financial support for operating expenses Administer and track IDA accounts Incentive savings match Financial literacy classes Staff support FINANCIAL INSTITUTIONS AS PARTNERS CAN PROVIDE….

WHAT IS A SPONSORING ORGANIZATION? • Sponsoring organizations are not for profit community organizations (also can be a low income financial institution or community development credit union) whose mission is to help low-income individuals and families achieve economic independence and become more vital community members.

SPONSORING ORGANIZATIONS (cont’d) • Establish IDA programs in order to help low income individuals and families become homeowners, develop or expand a small business or attend a post secondary education program

SPONSORING ORGANIZATIONSASSISTS PARTICIPANTS IN …. • Setting realistic short and long term personal, financial and asset goals • Establishing a strategy to achieve goals • Financial skills and knowledge to make informed financial decisions • Developing and improving self discipline, self esteem, self confidence and assertiveness particularly with regard to financial matters

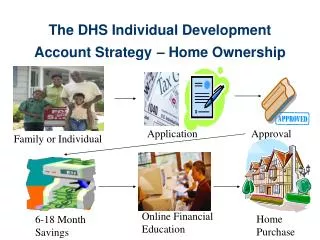

IDA PROGRAMS NEED FINANCIAL INSTITUTIONS TO…. • Open new accounts • Enhance existing accounts • Provide funding • Design and implement programs

WHY SHOULD FINANCIAL INSTITUTIONS GET INVOLVED? • CRA Consideration • Positive Public Relations • IDAs are low transaction, low cost accounts • IDA holders are potential customers for other bank products • IDAs can help rebuild communities

DESIGNING AN IDA PROGRAM IN A FINANCIAL INSTITUTION • Determine the feasibility of an IDA program, level of interest • Develop mission and purpose of IDA • Select a IDA Task Force • Identify community based organizations with similar mission as possible partners • Develop and conduct Survey

DESIGNING AN IDA PROGRAM IN A FINANCIAL INSTITUTION (cont’d) • What purposes will members save for with the IDA? • What is the average amount that someone would need for this purpose? • What is the desired length for someone to save? • What is the appropriate amount to save per month?

DESIGNING AN IDA PROGRAM IN A FINANCIAL INSTITUTION (cont’d) • How does it fit with other products offered by financial institution? • What other sources are available in the community to assist account holders? • Who will develop plan for raising operating expenses and match funds? • Task force to research, write grants, seek funding, etc.

DESIGNING AN IDA PROGRAM IN A FINANCIAL INSTITUTION (cont’d) • Identify partners to conduct financial literacy plan • Develop policies and procedures • Identify staff to manage IDA program • Develop plan to market IDA program

RESOURCES • Contact local community based organizations or the national CFED office at 202-408-9788 who will direct you to local IDA programs in your community. • To find a list of financial institutions that are currently participating in IDA programs: www.idanetwork.org, click on financial institutions, select your state

RESOURCES(cont’d) • For more information on financial institutions engaging in IDAs: www.cfed.org • For more information on Community Reinvestment Act (CRA) www.frb.org • For more information on Bank Enterprise Awards: www.treas.gov/cdfi

FINANCIAL LITERACY RESOURCES Financial literacy training resources: • Money Smart Program contact FDIC @ (202) 942-3404 • Financial Tool Kit contact Fannie Mae Foundation @ www.fanniemaefoundation.org