Long-run model of the economy

Long-run model of the economy long-run economic growth--trends grow on average at about 3% per year Short-run model recognizes that we observe lots of fluctuations around the trend Referred to as the Business Cycle Keys facts re. economic fluctuations not regular --not predictable

Long-run model of the economy

E N D

Presentation Transcript

Long-run model of the economy long-run economic growth--trends grow on average at about 3% per year

Short-run model recognizes that we observe lots of fluctuations around the trend Referred to as the Business Cycle

Keys facts re. economic fluctuations • not regular--not predictable • most series fluctuate together • as output falls unemployment rises, etc.

Composite Index of Leading Indicators: Components 1 Average weekly hours, manufacturing 2 Average weekly initial claims for unemployment insurance 3 Manufacturers' new orders, consumer goods and materials 4 Vendor performance, slower deliveries diffusion index 5 Manufacturers' new orders, nondefense capital goods 6 Building permits, new private housing units 7 Stock prices, 500 common stocks 8 Money supply, M2 9 Interest rate spread, 10-year Treasury bonds less federal funds 10 Index of consumer expectations

Downturns in economic activity • recession: rule of thumb--2 consecutive quarters of declining RGDP--but actually called by the NBER’s business dating committee • depression: very severe recession

Smoother economic activity Some controversy regarding the validity of the proposition that we are better at managing the economy--that the economic activity is smoother than it had been.

1) Classical dichotomy real variables vs. nominal variables 2) money neutrality changes in the Ms affect nominal variables and not real variables. Note: Long-run model based on classical theory

Short-Run Model demand and supply model of the economy downward sloping AD upward sloping AS

Aggregate Demand AD = f(PL; ) AD is the quantity of goods and services that households, firms and the government wants to buy at the different price levels.

1. The wealth effect As PL increases money in your possession has lower purchasing power. You feel poorer so you spend less. (less demand from consumers)

2. The interest rate effect As PL increases you need to convert more financial assets into cash. Hence less available for others to borrow in the loanable funds market. This causes r (the real interest rate) to rise so firms invest less. (less demand from businesses)

3. International trade effect As PL rises, U.S. goods become less competitive in world markets. NX falls. (less demand from foreigners)

Aggregate Demand shifters • Shifts due to changes in consumption: tax policy, expectations, wealth changes. • Shifts due to changes in investment: tax policies, monetary policy affecting interest rates, expectations re business activity. • Shifts due to changes in G purchases • Shifts due to changes in net exports: Ereal, foreign economic activity

Aggregate Supply More complicated because we need to distinguish the short-run AS from the long-run AS.

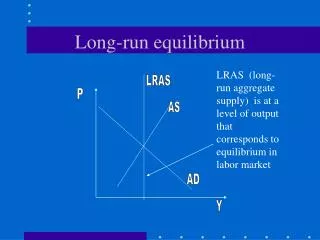

Long-run AS--LRAS The long-run aggregate supply curve is vertical at Y-potential. Where u = natural unemployment. Where we are when we are at full-capacity Long-Run Aggregate Supply PL RGDP

LRAS = f(K, L, tech, productivity, etc.) In this case real output does not depend on PL. Classical dichotomy: A real variable--doesn’t depend on a nominal variable.

In the short-run the AS curve slopes upward due to market imperfections. Short-run AS--SRAS Short-run Aggregate Supply

1. New Classical Misperceptions PL increases to PL2 Even though all prices have increased firms mistakenly believe it is a relative price increase. Ppotaotoes has risen but nothing else has. Hence firms produce more potatoes. Labor thinks its wages have risen, but prices of goods hasn’t so supplies more labor. Eventually firms and labor realizes all P’s rose and supply reverts to long-run level

2. Sticky Wages PL rises from PL1 to PL2, but nominal wages don’t adjust--(unanticipated inflation and the labor contracts did not build in wage increases to compensate). Firms produce more because can sell at higher prices but its costs haven’t risen But once labor unions negotiate a new contract, move back to LRAS and onto a new SRAS

3. Sticky Prices Menu costs: PL increases but it is costly to adjust prices all at once. But as expectations adjust we move to a new SRAS and back to the LRAS.

SRAS SRAS = f(PL; E(PL), ) + -

Equilibrium Equilibrium takes place where AD and SRAS intersect. But there is a difference between long-run equilibrium and short-run equilibrium. LR equilibrium: at potential output; at natural output. SR equilbrium: Where AD and SRAS intersect.

Two examples of getting knocked off equilibrium 1. Shift in the aggregate demand curve--AD shock 2. Shift in the aggregate supply curve--AS shock

Aggregate Demand Shock Examples: --Wave of pessimism shifts the AD curve to the left as in Sept. 11 with consumers spending less. --Government decides to spend less. --Foreign recessions cause US exports to fall.

Aggregate Supply shock Example: --Oil prices rise.

Self-correcting Recessions are self-correcting. There are natural tendencies that will take us out of recession if we are in a recession. But these mechanisms take a long time. We may want to speed things up. Purpose of fiscal and monetary policy