Download

1 / 42

420 likes | 670 Vues

Insurance solutions for an aging population Consumer Perspectives November 2012. Mark Twigg Executive Director, Cicero Group. Introduction. Ageing societies: A demographic time-bomb? Generating retirement incomes in future At retirement income products and financial advice.

E N D

Insurance solutions for an aging population Consumer Perspectives November 2012 Mark Twigg Executive Director, Cicero Group

Introduction • Ageing societies: A demographic time-bomb? • Generating retirement incomes in future • At retirement income products and financial advice

Aegon Retirement Readiness Survey 2012 • Findings based on 9,000 responses from nine countries • 8,100 current employees • 900 in retirement • Survey work completed early 2012 • Core objective to examine pensions sustainability and adequacy Sweden Neth. UK Poland Germany France Hungary Spain

Aegon Retirement Readiness Survey 2012 • Objective: To provide thought leadership defining the ‘enabler’ role of the insurer in an age of personal responsibility. The insurance industry: • Allow households to identify new risks and improve risk management • Enhances peace of mind and promotes financial stability • Helps to relieve the burden on government social security systems • Mobilises domestic savings and allocation of capital for use in the wider economy

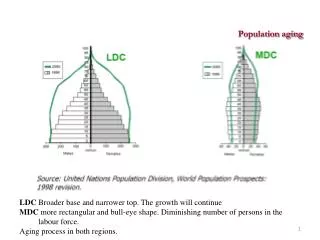

The world is ageing rapidly By 2040 there will be 1.8 billion people at or in retirement age Proportion of the world population over 60 and under 14 Source: UN population division

Families are having fewer children These numbers are lower in Europe, and lower still in Eastern Europe Low birth rates are compounded by net migration. Replacement level Source: UN population division

Europe is rapidly ageing Old age dependency ratio (65+ population per 100 15-65 year olds) • As a whole, Europe’s total fertility has fallen from 2.65 in 1950-55 to just 1.53 in 2005-10 • In the same time period life expectancy has risen from 65.6 to 75.3 UK 1950: 16.2 2010: 25.1 2050: 39.9 Sweden 1950: 15.5 2010: 28 2050: 42.3 Poland 1950: 8 2010: 19 2050: 47.9 Hungary 1950: 11.6 2010: 24 2050: 43.6 Germany 1950: 14.5 2010: 30.8 2050: 56.5 France 1950: 17.3 2010: 25.9 2050: 43.4 Spain 1950: 10.9 2010: 24.9 2050; 61.9 Source: UN population division

An uncertain future combined with low levels of retirement preparedness The AEGON Retirement Readiness Index is based on 6 questions relating to levels of awareness about retirement; understanding of the need to save more; willingness to save more; and current savings behaviours Source: AEGON retirement Readiness Survey 2012

A new found pessimism surrounding retirement Two-thirds of Hungarians are pessimsitic Source: AEGON retirement Readiness Survey 2012

Hungarians are the most pessimistic Source: AEGON retirement Readiness Survey 2012

People expect to be worse off than their parents in retirement... Social equity between the generations is breaking down Source: AEGON retirement Readiness Survey 2012

Interaction Between the retirement pillars – a balanced approach? Hungarians least likely to support personal responsibility Source: AEGON Retirement Readiness Survey 2012

Institutional Responses • The State • The Employer

A widespread belief that State Pensions will be less generous 83% of Hungarians expect a less generous state pension Source: AEGON Retirement Readiness Survey 2012

Hungarians have least confident in the state Source: AEGON Retirement Readiness Survey 2012

Employers are still seen as a key piece of the retirement income solution... Q. What should employers do to help people plan for retirement? Source: AEGON Retirement Readiness Survey 2012

A widespread belief that employers will reduce benefits Source: AEGON Retirement Readiness Survey 2012

Household Responses 3. Work More 4. Save More

Will you be likely to keep working after retirement? Source: AEGON Retirement Readiness Survey 2012

How will your transition into retirement change? Source: AEGON Retirement Readiness Survey 2012

A phased retirement is increasingly seen as the norm Retired Population Working Age population Source: AEGON Retirement Readiness Survey 2012

Opinions remain divided over extending ‘pensionable’ age Source: AEGON retirement Readiness Survey 2012

Individual behaviour is not keeping up with rising longevity Source: HSBC Future of Retirement 2011

Widespread belief that personal savings are worth less due to financial crisis 85% think savings have been negatively affected Source: AEGON Retirement Readiness Survey 2012

Again, Hungarians are among the most pessimistic Source: AEGON Retirement Readiness Survey 2012

Likely to plan more for retirement? Source: AEGON Retirement Readiness Survey 2012

What would encourage you to save more? 70% of Hungarians agreed that is was now more important to save for their retirement but 63% can’t afford it – fiscal incentives would be the biggest single help according to 47% Source: AEGON Retirement Readiness Survey 2012

What does retirement preparedness involve? Classic model of household income Source: HSBC Future of Retirement 2011

Income needs increase with age Retirement aspirations: 66% (63%) would like to travel; 52% (44%) pursue new hobbies* Onset of active retirement Onset of passive retirement *Source: AEGON Retirement Readiness Survey 2012

What do consumers need from insurers? • A better awareness of risks and a better value of those risks. “Value of insurance... Increasing prosperity and generally making people more aware of the reality of risks” (Geneva Association, 2012). • In retirement this applies to three key risks: • Longevity • Inflation • Investment

What product features really matter in retirement? Frail retirement Under-estimated ‘The Annuity Puzzle’ Source: AEGON Retirement Readiness Survey 2012

Clear need for more advice Source: AEGON Retirement Readiness Survey 2012

Hungarians recognise advice needs more than other countries Source: AEGON Retirement Readiness Survey 2012

Where would you go for advice? Source: AEGON Retirement Readiness Survey 2012

Advice needs identified Source: AEGON Retirement Readiness Survey 2012

What do consumers want from insurers? Source: AEGON Retirement Readiness Survey 2012

Conclusion • Demography and financial crisis have created ‘a perfect storm’ – reversals in living standards are now widely anticipated • The four pillars of retirement are shifting – failure to promote pensions will result in likely over-reliance on ‘make-do’ or ‘plan b’ options • Personal responsibility will increase but through which products and how is not clear – financial risks are complex and advice is lacking • “Insurance should be perceived not only as a protection mechanism, but more importantly as a partnership that allows individuals and businesses to spread their wings where they otherwise might not have dared to go” – (Geneva Association, 2012)