Understanding Financial Crises

340 likes | 487 Vues

Understanding Financial Crises. Franklin Allen and Douglas Gale Clarendon Lectures in Finance June 9-11, 2003. Lecture 2. Currency Crises Franklin Allen University of Pennsylvania June 10, 2003 http://finance.wharton.upenn.edu/~allenf/. Introduction.

Understanding Financial Crises

E N D

Presentation Transcript

Understanding Financial Crises Franklin Allen and Douglas Gale Clarendon Lectures in Finance June 9-11, 2003

Lecture 2 Currency Crises Franklin Allen University of Pennsylvania June 10, 2003 http://finance.wharton.upenn.edu/~allenf/

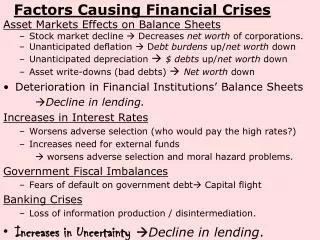

Introduction Major theme of the banking crises literature • Central bank/government intervention is necessary to prevent crises From 1945-1971 banking crises were eliminated but currency crises were not

Many of the currency crises were due to inconsistent government macroeconomic policies • Explanations of currency crises are based on government mismanagement • Contrasts with banking literature where central banks/government are the solution not the problem

First generation models • Krugman (1979) and Flood and Garber (1984) show how a fixed exchange rate plus a government budget deficit leads to a currency crisis • Designed to explain currency crises like that in Mexico 1973-82

Salant and Henderson (1978): Model to understand government attempts to peg the price of gold • Market Solution: Earn r on gold holdings P(t) = P(0) ert Ln P(t) = Ln P(0) + rt

Ln P(t) Ln Pc Ln P(0) T t

Ln P(t) Ln Pc Ln P* T t If the government pegs price at P*, what does the price path look like? Can’t be an equilibrium because of arbitrage opportunity

Ln P(t) Ln Pc Ln P* T’ T t Equilibrium: Peg until T’ then there is a run on reserves and the peg is abandoned

Krugman (1979) realized that the model could be used to explain currency crises • Government is running a fiscal deficit • It can fix the exchange rate and temporarily fund the deficit from its foreign exchange reserves

Ln S(t) Ln S* T’ t There is an exchange rate over time such that the “inflation tax” covers the deficit Equilibrium has predictable run on reserves and abandonment of peg

Problems with first generation models • Timing of currency crises is very unpredictable • There are often jumps in exchange rates • Government actions to eliminate deficits? • E.g. ERM crisis of 1992 when the pound and the lira dropped out of the mechanism

Second generation models • Obstfeld (1996): Extent government is prepared to fight the speculators is endogenous. This can lead to multiple equilibria. • There are three agents • A government that sells reserves to fix it currency’s exchange rate • Two private holders of domestic currency who can continue to hold it or who can sell it to the government for foreign currency

Each trader has reserves of 6 • Transactions costs of trading are 1 • If the government runs out of reserves it is forced to devalue by 50 percent

High Reserve Game: Gov. Reserves = 20 • There is no devaluation because gov. doesn’t run out of reserves. If either trader sells they bear the transaction costs. • The unique equilibrium is (0, 0)

Low Reserve Game: Gov. Reserves = 6 • Either trader can force the government to run out of reserves • The unique equilibrium is (0.5, 0.5)

Medium Reserve Game: Gov. Reserves = 10 • Both traders need to sell for a devaluation to occur • Multiple equilibria (0.5, 0.5) and (1.5,1.5)

Equilibrium selection • Sunspots – doesn’t really deal with issue • Morris and Shin (1998) approach • Arbitrarily small lack of common knowledge about fundamentals can lead to unique equilibrium

With common knowledge about fundamentals e.g. currency reserves C Unique Peg fails CL CU Unique Peg holds Multiple

With lack of common knowledge • Major advance over sunspots • Empirical evidence? Unique Peg fails C* Unique Peg holds

Twin Crises • Kaminsky and Reinhart (1999) have investigated joint occurrence of currency and banking crises • In the 1970’s when financial systems were highly regulated currency crises were not accompanied by banking crises • After the financial liberalizations that occurred in the 1980’s currency crises and banking crises have become intertwined

The usual sequence is that banking sector problems are followed by a currency crisis and this further exacerbates the banking crisis • Kaminsky and Reinhart find that the twin crises are related to weak economic fundamentals - crises when fundamentals are sound are rare • Important to develop theoretical models of twin crises

Panic-based twin crises • Chang and Velasco (2000a, b) have a multiple equilibrium model like Diamond and Dybvig (1983) • Chang and Velasco introduce money as an argument in the utility function and a central bank controls the ratio of currency to consumption

Banking and currency crises are “sunspot phenomena” • Different exchange rate regimes correspond to different rules for regulating the currency-consumption ratio • Policy aim is to reduce parameter space where “bad equilibrium” exists

Fundamental-based twin crises Allen and Gale (2000) extends Allen and Gale (1998) to allow for international lending and borrowing • Risk neutral international debt markets • Consider small country with risky domestic assets

Banks • Use deposit contracts with investors subject to early/late liquidity shocks • Can borrow and lend using the international debt markets • Domestic versus dollar loans

Domestic currency debt Risk sharing achieved through: • Bank liabilities • Deposit contracts • Large amount of domestic currency bonds • Bank assets • Domestic risky assets • Large amount of foreign currency bonds

Government adjusts exchange rate so the value of banks’ foreign assets allows them to avoid banking crisis and costly liquidation • Risk neutral international (domestic currency) bond holders bear most of the risk while domestic depositors bear little risk • If portfolios large enough all risk transferred to international market

Viable system of international risk sharing for developed countries whose banks can borrow in domestic currency • Many emerging countries’ banks cannot borrow in domestic currency because of the fear of inflation – they must borrow using dollar-denominated debt

Dollar-denominated debt • The benefits that a central bank and international bond market can bring are reduced • Dollarization: The central bank may no longer be able to prevent financial crises and inefficient liquidation of assets • Dollar debts and domestic currency deposits: It may not be possible to share risk with the international bond market

Policy Implications • Is the IMF important as lender of last resort like a domestic central bank (Krugman (1998) and Fischer (1999) OR • It misallocates resources because it interferes with markets (Friedman (1998) and Schwartz (1998)?

Framework above allows these issues to be addressed • Case 1: Flexible Exchange rates and Foreign Debt in Domestic Currency – No IMF needed • Case 2: Foreign Borrowing Denominated in Foreign Currency – IMF needed to prevent banking crises with costly liquidation and contagion

Conclusions • When is government the problem and when is it the solution? • The importance of twin crises • Interaction of exchange rate policies and bank portfolios in avoiding crises and ensuring risk sharing