Download

1 / 12

150 likes | 458 Vues

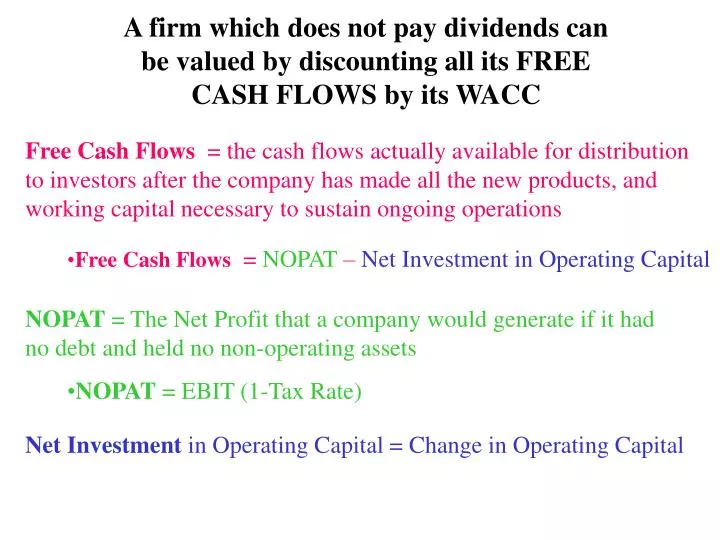

A firm which does not pay dividends can be valued by discounting all its FREE CASH FLOWS by its WACC. Free Cash Flows = the cash flows actually available for distribution to investors after the company has made all the new products, and working capital necessary to sustain ongoing operations.

E N D

A firm which does not pay dividends can be valued by discounting all its FREE CASH FLOWS by its WACC Free Cash Flows = the cash flows actually available for distribution to investors after the company has made all the new products, and working capital necessary to sustain ongoing operations • Free Cash Flows = NOPAT – Net Investment in Operating Capital NOPAT = The Net Profit that a company would generate if it had no debt and held no non-operating assets • NOPAT = EBIT (1-Tax Rate) Net Investment in Operating Capital = Change in Operating Capital

Operating Capital = Net Fixed Assets + Net Operating Working Capital Net Operating Working Capital = the working capital acquired with investor-supplied funds i.e. Current Assets – (Accounts Payable + Accruals)

Balance Sheet: Assets 2000 1999 Cash 7,282 57,600 AR 632,160 351,200 Inventories 1,287,360 715,200 Total CA 1,926,802 1,124,000 Gross FA 1,202,950 491,000 Less: Deprec. 263,160 146,200 Net FA 939,790 344,800 Total Assets 2,866,592 1,468,800

Liabilities and Equity 2000 1999 Accts payable 524,160 145,600 Notes payable 720,000 200,000 Accruals 489,600 136,000 Total CL 481,600 1,733,760 Long-term debt 1,000,000 323,432 Common stock 460,000 460,000 Retained earnings (327,168) 203,768 Total equity 132,832 663,768 Total L&E 2,866,592 1,468,800

Income Statement 2000 1999 Sales 5,834,400 3,432,000 COGS 5,728,000 2,864,000 Other expenses 680,000 340,000 (573,600) 228,000 EBITDA 116,960 18,900 Depr. & Amort. EBIT (690,560) 209,100 Interest exp. 176,000 62,500 EBT (866,560) 146,600 Taxes (40%) (346,624) 58,640 Net income (519,936) 87,960

What was the free cash flow (FCF) for 2000? FCF = NOPAT – Net investment in Operating Capital = -$414,336 – ($1,852,832 – 1,187,200) = -$414,336 – $665,632 = -$1,079,968.

net operating profit after taxes (NOPAT)? NOPAT = EBIT(1 – Tax rate) NOPAT00 = -$690,560(1 – 0.4) = -$690,560(0.6) = -$414,336.

Operating Capital Operating capital = Net fixed assets + NOWC = $939,790 + $913,042 = $1,852,832. = $1,187,200. Operating capital00 Operating capital99

Issues Regarding the Free Cash Flow Method • Free cash flow method is often preferred to the dividend growth model--particularly for the large number of companies that don’t pay a dividend, or for whom it is hard to forecast dividends. (More...)

FCF Method Issues Continued • Similar to the dividend growth model, the free cash flow method generally assumes that at some point in time, the growth rate in free cash flow will become constant. • Terminal value represents the value of the firm at the point in which growth becomes constant.

FCF estimates for the next 3 years are -$5, $10, and $20 million, after which the FCF is expected to grow at 6%. The overall firm cost of capital is 10%. 0 1 2 3 4 ... k = 10% g = 6% -5 10 20 21.20 -4.545 8.264 15.026 21.20 0.04 530 = = *TV3 398.197 416.942 *TV3 represents the terminal value of the firm, at t = 3.

The firm’s value would therefore be $416.942