Exponential Growth

Exponential Growth. Exponential Growth. Discrete Compounding Suppose that you were going to invest $5000 in an IRA earning interest at an annual rate of 5.5%. How much interest would you earn during the 1st year? How much is in the account after 1 year?. Exponential Growth.

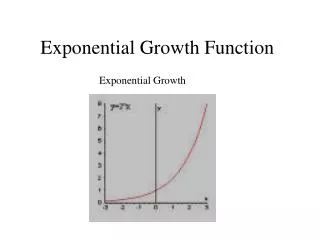

Exponential Growth

E N D

Presentation Transcript

Exponential Growth • Discrete Compounding • Suppose that you were going to invest $5000 in an IRA earning interest at an annual rate of 5.5%. How much interest would you earn during the 1st year? How much is in the account after 1 year?

Exponential Growth • Interest after 1 year: • Account value after 1 year: • What would happen during the 2nd year?

Exponential Growth • Interest made during the 2nd year: • Value of account after 2nd year: • What about for the 3rd year?

Exponential Growth • Interest made during 3rd year: • Value of the account after 3rd year:

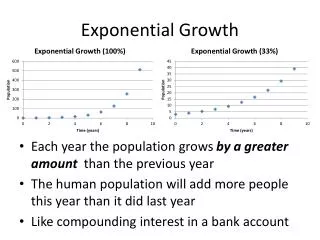

Exponential Growth • Summarizing our calculations:

Exponential Growth • From our calculations, a $5,000 investment into an account with an annual interest rate of 5.5% will have a value of F after t years according to the formula:

Exponential Growth • In general, P dollars invested at an annual rate r, has a value of F dollars after t years according to: • Notice that the interest was paid on a yearly basis, while our money remained in the account. This is called compounding annually or one time per year.

Exponential Growth • What would happen if the interest was paid more times during the year? • Suppose interest is collected at the end of each quarter, (interest is paid four times each year). What would happen to our investment?

Exponential Growth • Since the annual interest rate is 5.5% this rate needs to be adjusted so that interest is paid on a quarterly basis. The quarterly rate is:

Exponential Growth • Interest made during 1st quarter: • Value of account after 1st quarter:

Exponential Growth • Interest made during the 2nd quarter: • Value of account after 2nd quarter:

Exponential Growth • Interest made during the 3rd quarter: • Account value after 3rd quarter:

Exponential Growth • Interest made during the 4th quarter: • Account value after 4th quarter:

Exponential Growth • Summarizing our results for 1 year:

Exponential Growth • Notice that the exponent corresponds to the number of quarters in a year: • So for 1 year there are 4 quarters • So for 2 years there are 8 quarters • So for 3 years there are 12 quarters • So for 4 years there are 16 quarters • So for t years there are 4t quarters

Exponential Growth • So the value of a $5,000 investment with an annual interest rate of 5.5% compounded quarterly after t years is given by:

Exponential Growth • In general, P dollars invested at an annual rate r, compounded n times per year, has a value of F dollars after t years according to:

Exponential Growth • From the last slide, we can also say: • In other words, we can find the present value (P) by knowing the future value (F).

Exponential Growth • Notice for each of the 3 years the account that is compounded quarterly is worth more than the one compounded annually

Exponential Growth • It would seem the larger n is the more an investment is worth, but consider:

Exponential Growth • Notice value of the investment is leveling off when P, r, and t are fixed, but n is allowed to get really big. • This suggests that is leveling off to some special number

Exponential Growth • There is a clever technique that allows us to find this value. We let m = n/r, so that n = mr. For any value of r, m gets larger as n increases. We rewrite the expression:

Exponential Growth • As m gets big,

Exponential Growth • So as m gets large, • This is for continuous compounding • In Excel, use the function EXP(x)

Exponential Growth • So P dollars will grow to F dollars after t years compounded continuously at r % by the equation: • We can also find P by knowing F as follows:

Exponential Growth • How do we compare investments with different interest rates and different frequencies of compounding? • Look at the values of P dollars at the end of one year • Compute annual rates that would produce these amounts without compounding. • Annual rates represent the effective annual yield

Exponential Growth • In our current example when we compounded quarterly, after one year we had: • Notice we gained $280.72 on interest after a year. That interest represents a gain of 5.61% on $5000: Effective Annual Yield (y)

Exponential Growth • Effective annual yield (Discrete): • find the difference between our money after one year and our initial investment and divide by the initial investment. • Therefore, interest at an annual rate r, compounded n times per year has yield y:

Exponential Growth • You may need to find the annual rate that would produce a given yield. • Need to solve for r : This tells you the annual interest rate r that will produce a given yield when compounding n times a year. Note: This is only for Discrete Compounding

Exponential Growth • Effective Annual Yield (Continuous): • Annual interest rate:

Exponential Growth • Ex. Find the final amount if $10,000 is invested with interest calculated monthly at 4.7% for 6 years. • Soln.

Exponential Growth • Ex. Find the annual yield on an investment that computes interest at 4.7% compounded monthly. • Soln. • About 4.80%

Exponential Growth • Ex. Find the rate, compounded weekly, that has a yield of 9.1% • Soln. About 8.72%

Exponential Growth • Examples that use the word continuous to describe compounding period mean you use: • Ex. How much would you have after 3 years if an investment of $15,000 was placed into an account that earned 10.3% interest compounded continuously?

Exponential Growth • Soln.

Exponential Growth • Ex. Find the annual rate of an investment that has an annual yield of 9% when compounded continuously. • Soln. • Approx 8.62%

Exponential Growth • Where else can compound interest be used? • Financing a home • Financing a car • Anything where you make monthly payments (with interest) on money borrowed

Exponential Growth • The average cost of a home in Tucson is roughly around $225,000. Suppose you were planning to put down $25,000 now and finance the rest on a 30 year mortgage at 7% compounded monthly. How much would your monthly payments be?

Exponential Growth • For a 30 year mortgage, you’ll be making 360 monthly payments. • At the end of the 360 months we want the present value (P) of all the monthly payments to add up to the amount you plan to finance, e.g. $200,000 • The $200,000 is called the principal

Exponential Growth • Let’s say that Pkrepresents the present monthly value k months ago. • Then after 360 months, we want:

Exponential Growth • Since we’re borrowing money here, each Pkcan be expressed as • But where F represents the future value for Pk. In other words, F is your monthly payment.

Exponential Growth • Remember we want: • So if we insert: • We have instead:

Exponential Growth • Now for a little algebra (factor out F): • Divide both sides by the stuff in [ ]

Exponential Growth • The last result will tell us our monthly payment F: • Notice that all we need to is figure out how to add up the numbers in the bottom. This is where we use Excel.

Exponential Growth • Since we’re compounding monthly at 7%, r = 0.07 and n = 12 • So:

Exponential Growth • We’ll do the rest of our calculation in Excel • So our monthly payments F:

Exponential Growth • Now that we know what F is we can figure out what each Pk is. • Again, each Pkwill tell us what F dollars was worth k months ago • We’ll again use Excel to answer this question.

Exponential Growth End • In Excel: This number tells us that our monthly payment of $1330.60 was worth $1322.89 one month ago. Notice that as we descend down the table the values get smaller because we’re going farther back in time. This number tells us how much of the monthly payment is for interest. Notice that as we descend the table the interest goes up. This tells us that in the beginning of a payment plan a lot of the monthly payment is toward interest and only a small portion is going toward principal while the reverse is true at the end. Start

Exponential Growth • What your outstanding balance looks like with each monthly payment?