Download

1 / 25

250 likes | 323 Vues

Understand budgeting concepts, strategic planning, advantages, challenges, and the budgeting cycle. Learn how budgets help managers communicate, judge performance, and motivate employees. Dr. Mohamed Mousa provides insights on operating and financial budgets.

E N D

Chapter 6The Master Budget and Responsibility accounting Dr.Mohamed Mousa

Budget Defined : • A budget is the quantitative expression of a proposed plan of action by management for a specified period. • A budget is an aid to coordinating what needs to be done to implement that plan. • A budget generally includes the plan’s both financial and nonfinancial aspects and serves as a road map for the company to follow in an upcoming period. Dr . Mohamed Mousa

Budgets Help Managers…. • Communicate directions and goals to different departments of a company to help them coordinate the actions they must pursue to satisfy customers and succeed in the marketplace. • Judge performance by measuring financial results against planned objectives, activities, and timelines to learn about potential problems. • Motivate employees to achieve their goals. Dr . Mohamed Mousa

Strategic Plans and Operating Plans : Budgeting is most useful when it is integrated with a company’s strategy. Strategy specifies how an organization matches its capabilities with the opportunities in the marketplace to accomplish its objectives. Dr . Mohamed Mousa

Strategic Plans and Operating Plans : To develop successful strategies, managers must consider questions such as the following : • What are our objectives? • How do we create value for our customers while distinguishing ourselves from our competitors? • Are the markets for our products local, regional, national, or global? Dr . Mohamed Mousa

Strategic Plans and Operating Plans : • What trends affect our markets? • How do the economy, our industry, and our competitors affect us? • What organizational and financial structures serve us best? • What are risks and opportunities of alternative strategies and what are our contingency plans if our preferred plan fails? Dr . Mohamed Mousa

Budgeting Cycle: • Before the start of a fiscal year, managers at all levels take into account past performance, market feedback, and anticipated future changes to initiate plans for the next period. • Senior managers give subordinate managers a frame of reference, a set of specific financial or nonfinancial expectations, against which they will compare actual results. • Managers and management accountants investigate any deviations from the plan. Dr . Mohamed Mousa

Advantages of Budgets : Budgets are an integral part of management control systems. As we have discussed at the start of this chapter, when administered thoughtfully by managers, budgets do the following: • Promote coordination and communication among subunits within the company. • Provide a framework for judging performance and facilitating learning. • Motivate managers and other employees. Dr . Mohamed Mousa

Challenges in Administering a Budget : The budgeting process is time-consuming. Estimates suggest that senior managers spend about 10–20% of their time on budgeting and financial planning departments spend as much as 50% of their time on it. For most organizations, the annual budget process is a months-long exercise that consumes a tremendous amount of resources. Dr . Mohamed Mousa

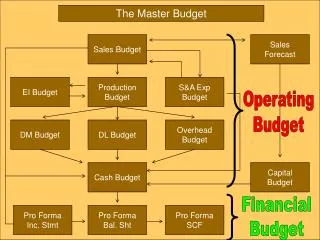

Working Document : Master Budget The master budget is at the core of the budgeting process. It expresses management’s operating and financial plans for a specified period: • Operating decisions deal with how to best use the limited resources of an organization (the operating budget). • Financial decisions deal with how to obtain the funds to obtain those resources (the financial budget). Dr . Mohamed Mousa

Operating Budget and Financial Budget : • The operating budget begins with the Revenues budget, includes multiple schedules and concludes with the Budgeted Income Statement. • The financial budget is made up of the Capital Expenditure budget, the Cash budget, the Budgeted Balance Sheet, and the Budgeted Statement of Cash Flows. Dr . Mohamed Mousa

Basic Operating Budget Steps : • Prepare the revenues budget . • Prepare the production budget . • Prepare the direct materials usage budget and direct materials purchases budget . • Prepare the direct manufacturing labor costs budget . • Prepare the manufacturing overhead costs budget Dr . Mohamed Mousa

Basic Financial Budget : Based on the operating budgets: • Prepare the capital expenditures budget. • Prepare the cash budget. • Prepare the budgeted balance sheet. • Prepare the budgeted statement of cash flows. Dr . Mohamed Mousa

the revenues budget : Sales budget company for the period from ... until ...... The following table shows the sales budget model in detail in terms of determining the quantity of goods available for sale: Dr . Mohamed Mousa

The Revenues budget : Sales budget company for the period from ... until ...... Dr . Mohamed Mousa

Example no 1: • Al Sadat Modern produces two models of remote control, X and y, and the unit sells for 24 $ and 40 $ respectively. The following are the forecasts of sales in units during the second and third quarters of 2018: • Number of units sold: following data: Required: Prepare the sales budget for the second and third quarters of 2018. Dr . Mohamed Mousa

Solution the Sales balance for the second and third quarter of 2018: Dr . Mohamed Mousa

the productionbudget : • The production program budget is based on sales budget estimates. • Estimated quantity of production = sales quantity + total production stock last period - total production stock for the first period. Dr . Mohamed Mousa

The Direct materials purchases budget : • The purchases budget is concerned with determining the value of purchases incurred by the establishment in order to obtain raw materials. • Quantity of materials to be purchased =Quantity of raw material requirements + Quantity of raw material stock last period- Quantity of stocks of raw materials for the first time. • Value of purchases = Quantity of items to be purchased × Average purchase price of the unit. Dr . Mohamed Mousa

The Direct materials purchases budget : Planning budget for the company's procurementFor the period from ... until ...... Dr . Mohamed Mousa

Example no 2: • Gana company produces one of its products using two types of raw materials (X), (Y). The 2017 sales plan was distributed over three-year periods as follows: • First trimester 50,000 units. • Second trimester 30,000 units. • Third trimester 40,000 units. • If you know that:* The budget plan for 2016 states that the remaining stock of the period is 16,000 units. Dr . Mohamed Mousa

Example no 2: * The production plan for 2017 is drawn up so that the stock at the end of every third year is equivalent to 15% of the sales. • The operation of the product unit requires the use of 3 kg of raw material (x) at the price of 5 $ per kilogram, and requires the use of 4 kg of raw material (y) at 10 $ per kilogram. Required:1 - Preparation of production budget for every third year and for the year in total?2 - Preparation of the balance of production needs of raw materials for every third year and for the year in total? Dr . Mohamed Mousa

Solution First: the budget of production for every third year and for the year in total: Dr . Mohamed Mousa

Solution Second: To balance the production needs of raw materials for every third year and for the year in total: Dr . Mohamed Mousa

The Next Lecture Sequences Chapter 6 “ The Master Budget and Responsibility accounting “ Dr . Mohamed Mousa