Exponential Smoothing

70 likes | 287 Vues

Exponential Smoothing. All statistical fitting methods involve some type of smoothing e.g., in regression, a trend line is fitter to the data points Consider the following forecasting scheme f t = wy t-1 + (1-w)f t-1 or, if you update by one period f t+1 = wy t + (1-w)f t

Exponential Smoothing

E N D

Presentation Transcript

Exponential Smoothing • All statistical fitting methods involve some type of smoothing • e.g., in regression, a trend line is fitter to the data points • Consider the following forecasting scheme • ft = wyt-1 + (1-w)ft-1 • or, if you update by one period • ft+1 = wyt + (1-w)ft • Another way to write the process is • ft+1 = ft + w(yt – ft) • The forecast is the current forecast plus a fraction of the current forecast error. Exponential Smoothing

Weighting Past Values • Exponential smoothing places declining weights on past values of a series. Consider ft+1 = wyt + (1-w)ft = wyt + (1-w)[wyt-1 + (1-w)ft-1 ] = w[yt + (1-w)yt-1] + (1-w)2(ft-1) = w[yt + (1-w)yt-1] + (1-w)2[wyt-2 + (1-w)ft-2 ] = w[yt + (1-w)yt-1+(1-w)2yt-2 ] + (1-w)3ft-3 Exponential smoothing places geometrically declining weights on past valued of {yt} Exponential Smoothing

Properties of the weights • Note that w must be between 0 and 1 • A large value of w places a high weight on the current realization of the series • The sum of the weights on past values of {yt} is unity. • The spreadsheet shows a value of w = 0.8 Exponential Smoothing

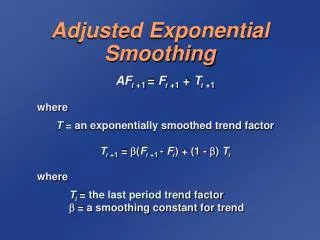

Holt-Winters • Other smoothing methods involve smoothing a trend lines fit to a data series • ft+1 = wyt + (1-w)(ft+Tt) • Tt+1 = b(ft+1 – ft) +(1-b)Tt The one-step ahead forecast is Ht+1 = Ft+1 + Tt+1 • The m=step ahead forecast is • Ht+m = Ft+1 + mTt+1 • Winter’s method includes seasonals • In forecast x you select • alpha for the level • beta for the seasonal • gamma for the trend Exponential Smoothing

Hints • The moving average and exponential smoothing methods will work well with series that do not have a trend or structural breaks. • Exponential smoothing will be preferable if you want to heavily weight near-term events. • Use the Holt-Winters Method for data that has trend and seasonals. • Select values alpha, beta and gamma near 1 if you want forecasts to change strongly with new information. • Forecast-x will also select the smoothing coefficients for you. • The Mean Square Forecast Error (or RMSE) is often used a a criterion as to the best smoothing constant. • The adaptive-response model is limited; it will not be discussed in class Exponential Smoothing