Download

1 / 5

50 likes | 69 Vues

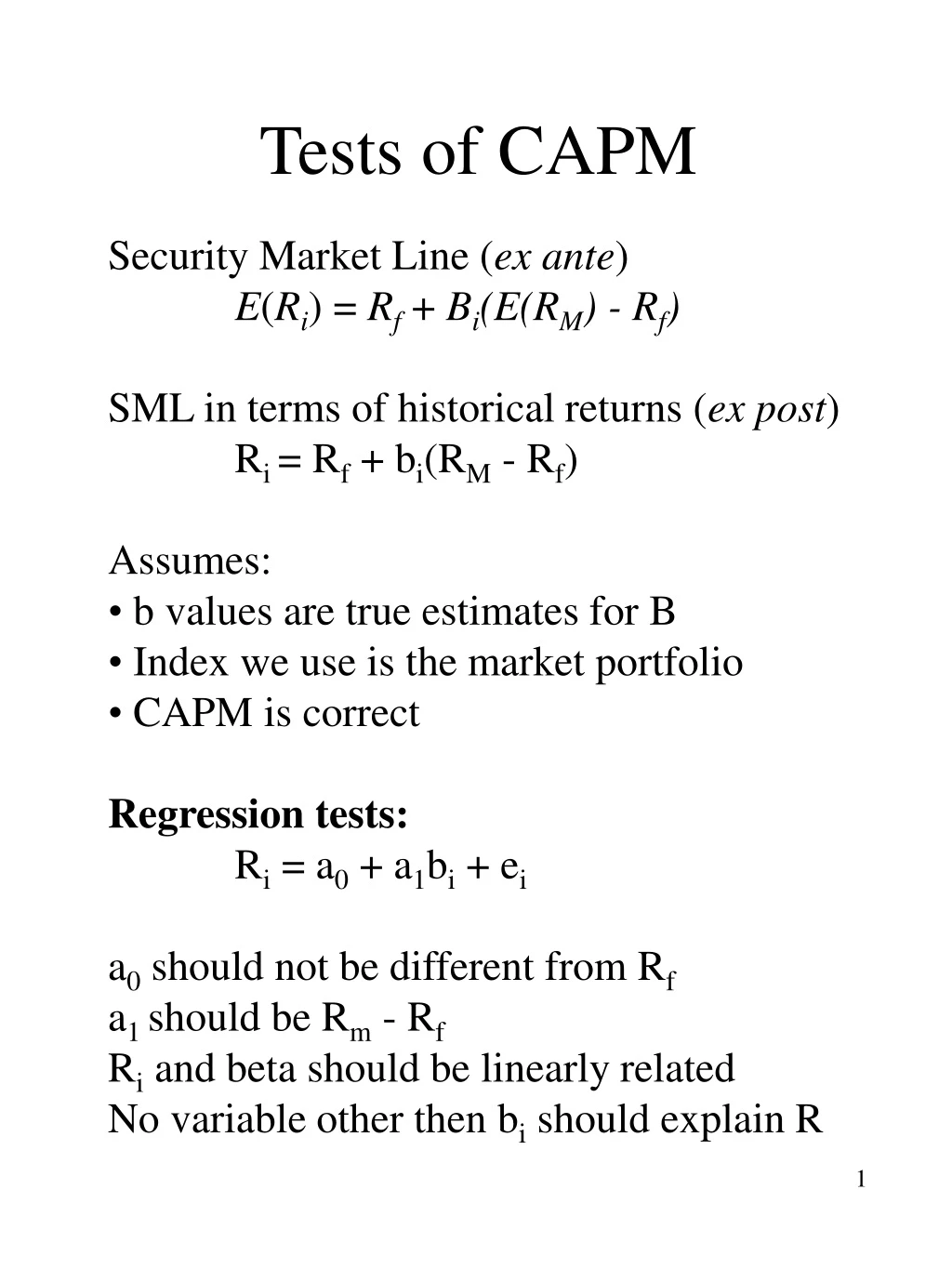

Tests of CAPM. Security Market Line ( ex ante ) E ( R i ) = R f + B i (E(R M ) - R f ) SML in terms of historical returns ( ex post ) R i = R f + b i (R M - R f ) Assumes: b values are true estimates for B Index we use is the market portfolio CAPM is correct Regression tests:

E N D

Tests of CAPM • Security Market Line (ex ante) • E(Ri)= Rf + Bi(E(RM) - Rf) • SML in terms of historical returns (ex post) • Ri = Rf + bi(RM - Rf) • Assumes: • b values are true estimates for B • Index we use is the market portfolio • CAPM is correct • Regression tests: • Ri = a0 + a1bi + ei • a0 should not be different from Rf • a1 should be Rm - Rf • Ri and beta should be linearly related • No variable other then bi should explain R

Tests of CAPM Early Studies: Black, Jensen and Scholes (1972) Fama and MacBeth (1973) Findings: - a0 is higher than Rf, a1 is smaller than RM - Rf - beta is the only measure of risk that explains average returns - The model is linear in beta Recent Studies: Fama and French (1992) Anomalies

Roll’s Critique of CAPM tests - Tests of CAPM are tests of the market portfolio’s mean-variance efficiency - Market portfolio can never be observed - As long as the proxy used for M is ex-post efficient, the betas calculated using this proxy will be linearly related to the returns. - CAPM cannot be used for performance evaluation

Arbitrage Pricing Theory Return generating process: Ri = ai + bi1F1 + bi2F2 + ….+ binFn + ei Taking expectations: E(Ri) = ai + bi1E(F1) + bi2E(F2)+ .+ binE(Fn)+ ei Ri - E(Ri) = bi1(F1 - E(F1)) + bi2(F2 - E(F2)) +... + bin(Fn - E(Fn)) +ei or Ri = E(Ri) + bi1f1 + bi2f2 + ….+ binfn + ei where fj= Fj - E(Fj): unanticipated change in Fj In Equilibrium: E(Ri) = 0 + bi11 + bi22 + .+ binn where 0 = Rf, 1, 2 … n are the risk premiums associated with each factor.

Roll & Ross and their four factors E(Ri) = Rf + Unexp Change in Inflation Unexp Change in Industrial Prod. Unexp Change in bond risk premium Unexp Change in yield curve