Download

1 / 21

460 likes | 1.29k Vues

Taylor Smith. Bankruptcy and the Altman z-score. Review of Corporate Bankruptcy. Filed under Chapter 7 or 11 of US Bankruptcy Code Chapter 11 calls for reorganization of the company A system for repaying debts is created Often look to keep company moving while going through proceedings

E N D

Taylor Smith Bankruptcy and the Altman z-score

Review of Corporate Bankruptcy • Filed under Chapter 7 or 11 of US Bankruptcy Code • Chapter 11 calls for reorganization of the company • A system for repaying debts is created • Often look to keep company moving while going through proceedings • Many companies have gone through bankruptcy proceedings including: • GM • Chuck E. Cheese • Circuit City Stores

Can we see it coming? • Original work on statistical methods to predict bankruptcy started in the 1930’s • R.A. Fisher developed a technique for discriminant analysis • William Beaver used t-tests to predict bankruptcy (66-68) • Could only study one factor at time • Compared the importance of each factor • Found Cash flow to debt ratio to be most important

Edward I. Altman • Professor of Finance at NYU • Developed the Z-score formula • Predicts the likelihood of a company going bankrupt within 2 years • Published in 1968 • Uses Fisher’s multivariate technique • Compares factors like Beaver’s method • Multiple factors at once

Altman Z-Score • Uses a variety of information from corporate balance and income sheets • Ex. Total Assests, Net Sales, Market Cap etc. • Developed using 66 manufacturing companies • Half had filed for Bankruptcy • Has been restructured to fit other types of companies since then • Cannot fit financial institutions

Multiple Discriminate Analysis • “MDA is a statistical technique used to classify an observation into one of several a priori groupings dependent upon the observation’s individual characteristics.” • Qualitative dependent variables • Tries to make a linear combination of quantitative factors which “best” separate between the groups • i.e. Z=V1X1+V2X2+…+VnXn • V1...n are coefficients • X1…n are independent variables

Altman Z-Score • Variables are actually ratios • 22 variables were originally studied • 5 Categories • Liquidity • Profitability • Leverage • Solvency • Activity • 5 of these were finally chosen • Were the best combination

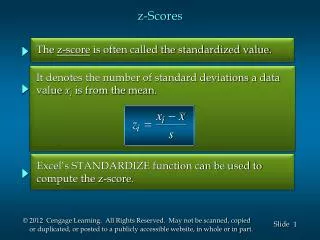

Finally, the Z-score Formula! • Z = 0.012X1 + 0.014X2 + 0.033X3 + 0.006X4 +0.999X5 • X1 = working capital/total assets, • X2 = retained earnings/total assets, • X3 = earnings before interest and taxes/total assets, • X4 = market value equity/book value of total liabilities, • X5 = sales/total assets • Z = overall index

What do these variables mean? • X1: Working Capital/Total Assets • Net liquid assets relative to total capitalization • X2: Retained Earnings/Total Assets • Retained Earnings= total amount of reinvested earnings and/or losses over a company’s lifetime • Reflects company’s age • X3: Earnings before Interest and Taxes/Total Assets • Measures true profitability

Variables continued. • X4 : Market Value of Equity/ Book Value of Total Liabilities • MVE: combined value of all shares of stock • How far assets can decline before the company becomes insolvent • X5: Sales/Total Assets • “Capital-turnover ratio” • Measures ability of assets to generate sales • Least significant when taken individually

We have a formula, we have variables. Now what? • Zones of Discrimination: • Z>2.99 “Safe” Zone • 1.8<Z<2.99 “Grey Zone” • Z<1.80 “Distress” Zone • Likely to go bankrupt in the next 2 years • Score below 1.80 means a company is in financial distress, and likely to declare bankruptcy

Adaptations • Has been adapted to fit different situations • Private Firms • Non-Manufacturer Industrials and Emerging Market Credits • Changes in coefficients, variables, and zones of discrimination

Accuracy of Altman’s Z-Score • Altman reports that his model identified 95% of total first sample correctly • From statements one year before their bankruptcy • When it becomes 2 years, it is 72% accurate • To test accuracy further, he used a second sample • In this sample, the model was 96% correct

Still calculating… Z=1.2(,014434551)+1.4(0.219384237)+ 3.3(0.082801211 )+.6 (2.938304483) +.999(0.605360194 ) Z=3.86 SAFE ZONE!

Comparison • The comparison obviously isn’t perfect • However, there is a general pattern! • A revised version of the Altman Z-Score by Altman, Hartzell, and Peck in 1995 matches bond ratings • Called Emerging Market Score • Calibrated to bond rating, so score is adjusted to how risky a bond is considered

Comparison to another predictive factor: Again, not perfect, but there is the same general trend!

Sources • Altman, Edward I. Predicting Financial Distress of Companies: Revisiting the Z-Score and Zeta Models • Moodys.com • http://www.lawbizmath.com/?p=65 • Finance.yahoo.com/q?s=KFT • Advfn.com • http://en.wikipedia.org/wiki/Altman_Z-score • http://en.wikipedia.org/wiki/Edward_I._Altman