Schools

Schools. FIR$T. Financial Integrity Rating System of Texas. Eagle Pass ISD 2006 Report September 12, 2006. Rating System of Texas. Financial Accountability. • Fourth Year of Implementation • Created by the Texas Legislature in 2001

Schools

E N D

Presentation Transcript

Schools FIR$T Financial Integrity Rating System of Texas Eagle Pass ISD 2006 Report September 12, 2006

Rating System of Texas Financial Accountability • Fourth Year of Implementation • Created by the Texas Legislature in 2001 • Designed to help improve management of school districts’ financial resources by evaluating their Financial Performance • Evaluates the financial health, stability, and condition of school districts in Texas • Provides Financial Management Performance Rating of school districts for the Texas Education Agency (TEA) Known as “Schools FIR$T”

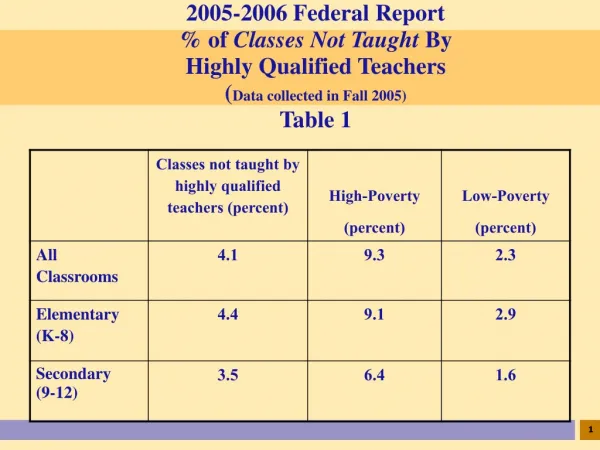

How Much Money Flows Through Texas Public School Business Offices? Amount* Percentage Local $14,942,058,462 42.63% State $12,309,158,320 35.12% Federal $ 2,418,773,992 6.90% Financing -Bonds $ 5,333,850,386 15.22% Capital Leases $ 47,149,266 0.13% Total* $35,050,990,426 100.00% * TEA Statistical Info: FY Ended August 31, 2001 (in billions)

Range of PublicSchool Expendituresin 1,040 Districts LARGEST $1.8 Billion 04-05 EPISD* $104.4 Million SMALLEST $203,896 Note: EPISD is 173rd Largest District (Top 17%) * 2004-05 Annual Financial Report

EPISD Fact Sheet 2004-2005 • Total Enrollment * 13,531 • Campuses 24 • Total Staff * 1,896 • Teachers * 794 (Starting Salary: $33,000) • Payroll Checks ** 58,200 • Governmental Fund Budgets 75 • Total G/L Accounts ** 18,000 • Purchase Orders Per Year ** 9,254 • Total Vendors 8,500 (500 Local Vendors) * 2004-2005 AEIS Report ** Estimated

Defined • Expands the Public Education Accountability System in Texas to include both Academic and Financial Reporting • Comprised of indicators at the district level similar to the current Academic Performance Rating System (AEIS Report)

Financial Accountability Rating System • SB 875, 76th Legislative Session • TEA consulted with Comptroller of Public Accounts • TEA forwarded a Proposal to Legislature in December, 2000 • SB 218 Requires Implementation of this System

Senate Bill 218 • Subchapter I. FINANCIAL ACCOUNTABILITY Added to Chapter 39, Texas Education Code • Section 39.201. Definitions • Section 39.202. Development and Implementation • Section 39.203. Reporting • Section 39.204. Rules

Goals •Achieve improved performance in the management of school districts’ financial resources • Facilitate better uses of financial resources •Demonstrate increased district financial performance

Objectives • Assess the quality of financial management • Publicly report the Rating • Assure the maximum allocation possible for direct instructional purposes • Implement a Rating System that fairly and equitably evaluates the quality of financial management decisions

Objectives (Continued) Make a Financial Rating System that: • Is simple and understandable • Is applicable to all districts • Is based on quantifiabledata • Allows for self administration • Provides an early warning • Is substantially within district’s control • Is zero burden to districts

Data Sources •Annual Financial Reports filed by school district •Public Education Information Management System (PEIMS) Data

District Ratings • Based on 21 Indicators • Failure to pass any of the First 5 (Five) Indicators will result in Automatic Failing: Indicator #1: Deficit Fund Balance in General Fund Indicator #2:Default on Debt Payment Indicator #3: Annual Financial Report not filed within one Month after November 27 or January 28 Indicator #4: Qualified Opinion in Audit Indicator #5: Material Weaknesses in Internal Controls

District Ratings Rating Number of “No” Answers • Superior Achievement 0-2 • Above Standard Achievement 3-4 • Standard Achievement 5-6 • Substandard Achievement More than 6 or No to Default Indicator • Suspended – Data Quality

Sanctions Substandard Achievement Rating may result in assignment of a Financial Monitor or Master to control district finances.

TEA Reports Require: • Distribution of hard copy reports in transitional year of implementation 1st Year: FY 2001-2002 3rd Year: 2003-2004 2nd Year: FY 2002-2003 4th Year: 2004-2005 • Publication on TEA internet site during full implementation • Public Notice Posting of Rating • Public Meeting for discussion of Ratings

Overview of 21 Indicators • (Divided into Five Components) • Critical Indicators (Indicators #1-5) • Fiscal Responsibility (Indicators #6-10) • Budgeting (Indicators #11-14) • Personnel Management (Indicators #15-17) • Cash Management (Indicators #18-21)

Five Critical Indicators (Required for a “Passing Rating”) • Are you Bankrupt? • Did you pay your Bond Payments? • Did you file Reports on Time? • Did you receive a Clean Audit? • Have you kept the District in Financial Compliance?

Critical Indicators • (Indicators #1-5)

Indicator 1 Are you bankrupt? 1. Was Total Fund Balance less Reserved Fund Balance, greater than zero in the General Fund? * Current Result: Yes ** Previous Result: Yes Calculations: * Total General Fund Balance as of 8/31/05 $8,621,972 LESS Reserves $89,784 = $8,532,188 ** Total General Fund Balance as of 8/31/04 $6,509,570 LESS Reserves $204,962 = $6,304,608

Fund Balance Spending • Is for nonrecurring costs. • Is not for paying recurring costs such as payroll, utilities, etc. • Should not be too low or too high.

Indicator 2 Did you pay your Bond Payments? 2. Were there no disclosures in the Annual Financial Report and/or other sources of information concerning default on bonded indebtedness obligations? * Current Result: Yes ** Previous Result: Yes Calculations: * The Annual Financial Report for the year ended August 31, 2005 did not disclose Default Disclosures. ** The Annual Financial Report for the year ended August 31, 2004 did not disclose Default Disclosures.

Did you pay your Bond Payments? • No defaults through 2005 • Ability to pay over time • Debt retirement to utilize Interest & Sinking Tax Rates • I & S Revenues, not too much or too little

Indicator 3 Did you file Reports on time? 3. Was the Annual Financial Report filed within one month after November 27th or January 28th Deadline depending upon the District’s Fiscal Year End Date (June 30th or August 31st)? * Current Result: Yes ** Previous Result: Yes Calculations: * Date Audit Received 12-16-05 (Due Date: 02-28-06) ** Date Audit Received 12-20-04 (Due Date: 02-28-05)

Indicator 4 Did you receive a Clean Audit? 4. Was there an unqualified opinion in Annual Financial Report? * Current Result: Yes ** Previous Result: Yes Calculations: * Unqualified Opinion for 2004-2005 Annual Financial Report ** Unqualified Opinion for 2003-2004 Annual Financial Report

Did you receive a Clean Audit? • Illegal deficit spending • Lack of internal controls • Misappropriation of funds • Co-mingling of Designated Purpose Funds • Failure to meet 85% Requirement • Improper securities by depository

Indicator 5 Have you kept the District in Financial Compliance? 5. Did the Annual Financial Report not disclose any instance(s) of material weaknesses in internal controls? * Current Result: Yes ** Previous Result: Yes Calculations: * No disclosure of Weak Internal Controls included in the 2004-2005 Annual Financial Report. ** No disclosure of Weak Internal Controls included in the 2003-2004 Annual Financial Report.

Have you kept the District in Financial Compliance? • Check and balance system • Internal controls intended to guarantee: –Proper recording of transactions –Legal compliance –Safeguard funds, property & assets against loss

FISCAL RESPONSIBILITY • (Indicators #6-10)

Indicator 6 Are you doing a good job collecting your taxes? 6. Was the percent of Total Tax Collections (Including Delinquent) greater than 96%? * Current Result: Yes ** Previous Result: Yes Calculations: * 2004-05 Total Tax Collections ¸Total Tax Levy = 14,502,130 ¸ 14,850,249 = 97.66% ** 2003-04 Total Tax Collections ¸Total Tax Levy = 13,382,473 ¸ 13,587,674 = 98.48%

EPISD Taxes Collected Current* Delinquent** Total 2005 89.41% 8.25% 97.66% 2004 88.51% 9.97% 98.48% 2003 87.87% 11.10% 98.97% 2002 88.02% 9.63% 97.65% 2001 85.03% 9.77% 94.80% Ninety percent (90%) of school districts state-wide collect 96% of their taxes or more. *Current Collections ¸ Tax Levy = $13,277,294 ¸ 14,850,249 = 89.41%, Total Current **Delinquent Collections ¸ Tax Levy = $1,224,836 ¸ 14,850,249 = 8.25%, Total Delinquent

Indicator 7 Do your numbers match? 7. Did the comparisons of PEIMS Data to like information in Annual Financial Report result in an aggregate variance of less than 4% of expenditures per Fund Type (Data Quality Measure)? * Current Result: Yes ** Previous Result: Yes * The difference was less than zero percent or 0%. ** The difference was less than zero percent or 0%.

Indicator 8 Can the district afford the Debt payment? 8. Were debt related expenditures less than $770.00 per student? * Current Result: Yes ** Previous Result: Yes Eagle Pass ISD had less than $65.69 per student. Calculation: (Function 71 Expenditures – IFA and EDA Allotments) / 2002 Total Students = * $3,632,908 - $2,743,994 / 13,531 = $65.69 ** $8,116,123 - $2,894,377 / 13,385 = $390.12

Indicator 8 EPISD 5-Year Percentage Change in students is greater than 2% Enrollment Growth for Fiscal Year Ending 2005 was1.1% * 5-Year Growth was 8.2% ** Calculation: * 2005 Total Students – 2004 Total Students / 2004 Total Students = 13,531-13,385/13,385 = 1.1% ** 2005 Total Students – 2001 Total Students / 2001 Total Students = 13,531-12,515/12,515 = 8.2%

Indicator 9 Did you follow the rules? 9. Was there no disclosure in the Annual Audit Report of material noncompliance? * Current Result: Yes ** Previous Result: Yes * No Material Non-Compliance included in the 2004-2005 Annual Financial Report ** No Material Non-Compliance included in the 2003-2004 Annual Financial Report

Did you Follow the Rules? • Poor segregation of duties • Records do not reconcile (such as PEIMS and Annual Financial Audit) • Competitive bid violations • Inaccurate and untimely reporting • Fund balance deficit • Expenditures exceed the budget

Indicator 10 Were you able to stay in Financial Compliance? 10. Did the district have full accreditation status in relation to financial management practices? * Current Result: Yes ** Previous Result: Yes * Full Accreditation, No Master or Monitor Assigned for 2004-2005 ** Full Accreditation, No Master or Monitor Assigned for 2003-2004

BUDGETING • (Indicators #11-14)

Indicator 11 Were Students First? 11. Was the Percent of Operating Expenditures Expended for Instruction more than 54%? * Current Result: Yes ** Previous Result: Yes * General Fund Budget: State Average 57.9% and EPISD 55.8% as per 2004-2005 AEIS Report ** General Fund Budget: State Average 51.8% and EPISD 54.2% as per 2003-2004 AEIS Report

Were Students first? •Start above 54% to allow for resignations, unfilled teaching positions, etc? •If too far above 54%, are you overstaffed? •Schools exist to teach students and additional costs serve to provide support. •All “Function 11” Expenditures are included.

Were Students First? Instruction = 55.8% of Expenditures Calculation: Expenditures in General, Special Revenue and Capital Projects Funds (Excluding SSA Fund Codes) in Function 11 and Object Codes 6112-6499/Expenditures in General Fund, Special Revenue Fund (Excluding SSA Fund Codes), Capital Project Fund, Enterprise Fund 701 (Child Nutrition Program), Functions 11-61 and Object Codes 6112-6499 = Current: $55,196,496 / $98,999,806 = 55.8% Previous: $51,982,807 / $92,402,268 = 56.3%

Indicator 12 Did you live within your means? 12. Was the aggregate of Budgeted Expenditures and other uses less than the Aggregate of Total Revenues, other resources and fund balance in General Fund? * Current Result: Yes ** Previous Result: Yes * The remaining aggregate in the General Fund was $6.8 million for 2004-05 FY. ** The remaining aggregate in the General Fund was $8.2 million for 2003-04 FY.

Did you live within your means? •Do not begin with a deficit budget. •Student attendance and tax collections determine revenues. •Put the expenditure brakes on if the previous months are not meeting budgeted expectations. •Just because it is in the budget does not mean it is in the bank.

Indicator 13 Did you borrow enough money for construction? 13. If the district’s Aggregate Fund Balance in the General Fund and Capital Projects Fund was less than zero, were construction projects adequately financed? * Current Result: Yes ** Previous Result: Yes Calculation: Fund Balance in the General Fund as of the Fiscal Year End + Fund Balance in the capital projects fund as of the Fiscal Year End > Standard Capital Fund Margin = * $8,621,972 + $6,039,549 = $14,661,521 > 0 ** $6,509,570 + $7,000,862 = $13,510,432 > 0

Indicator 14 Did you save the overpayment? 14. Was the ratio of cash and investments to deferred revenues in the General Fund greater than or equal to 1:1, or, less than or equal to 0? * Current Result: Yes -126,313 <= 0 ** Previous Result: Yes-178,144 <= 0 Calculation: Cash and Investments in the General Fund / (Deferred Revenue in the General Fund – Property Tax Receivable Net of Uncollectable = * $8,389,588 / ($3,067,654 - $3,193,967) = -66.41 => 1 or 0 => -126,313 ** $7,226,838 / ($2,883,838 - $3,061,952) = -40.57 => 1 or 0 => -178,144