Download

1 / 40

400 likes | 426 Vues

This is a cost that does not change with the amount the firm is producing or selling. Usually expressed in terms of an amount per time (week, Month etc). This can change over time…e.g. the insurance, rent or rates can change BUT not with the amount sold.

E N D

This is a cost that does not change with the amount the firm is producing or selling. Usually expressed in terms of an amount per time (week, Month etc). This can change over time…e.g. the insurance, rent or rates can change BUT not with the amount sold.

Money owed which does not have to be paid back within the next year…a long term bank loan, company stock, debentures.

An amount owing that the business will have to repay in the next year…e.g. an overdraft (repayable when asked for by the bank) trade credit (usually one month).

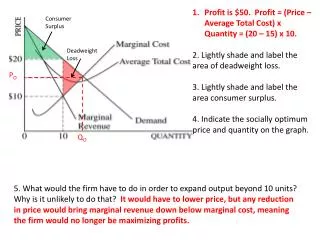

The output at which the firm stops making losses and is about to begin making a profit. It is where the turnover = total cost. You should be able to draw a simple diagram and shade in the areas of profit and loss.

Security for a long term loan from a building society or bank which is used to buy property (or machines). The lender has first claim on the sale of the property up to the point it has got its loan and interest repaid.

Gross Profit x 100 Turnover

This has to be held by the company every year. It gives shareholders a chance to vote about what the company is doing.

Bank overdraft Trade Credit Debt Factoring

This is the total sales revenue of the firm. It is the number of items sold x the price charged per item.

The original owners sell these to raise the money for the business…the buyers have not made a loan to the company but have bought a piece of it. They can vote about what happens and are entitled to the profits. People can sell these on the stock exchange…prices do vary so there is a risk of loss.

These may be given by government to encourage a firm to invest…not a loan as it doesn’t need to be repaid.

If you buy these in a company you don’t become a shareholder and get no cut out of profit and no say in how the company is run. You would get an interest rate on the money you have loaned plus a guarantee about when the money will be repaid…you can always sell these at an exchange if you want the money back sooner… though you might get a lower price…there is a risk.

These are assets which the business has in the form of cash in its tills/ bank or items which will soon become cash…e.g. stocks of goods or debtors (people that owe the business money).

Bank loan Hire Purchase Leasing

This is an estimate or prediction about how a business thinks that money will come in and how it will leave the business. The main aim is to identify times when the business is likely to be short of money…this is a risky time as the business could easily become bankrupt if it is unable to pay its bills. Usually the business will have an overdraft to cover these times.

This is where profit is put back into the business rather than being given as a dividend to the shareholders.

This shows the assets (resources owned by the business) and the liabilities (amounts owing by the business…including the money put in by the owners).

This is the account in which the gross and net profit of the business are worked out…it normally covers one year of trading.

This is where a business needs money for a short period of time and will soon be able to repay it e.g. borrowing to pay wages because the goods made should be sold quickly and the business will get the money back in a short time e.g. overdraft and trade credit.

These are costs that change directly with the amount being produced or sold by the firm…e.g. raw materials, delivery charges.

A cost which usually has to be paid when a firm borrows money.

These are made up of the retained profits of the business over time …and are used by it to keep the company going or to expand.

This type of profit is the Gross Profit minus the expenses (overheads) of the business. Suppose a shop has overheads of £9000, then the type of profit in question would have been £6000: £15000 gross less £9000 overheads = £6000 of this type of profit.

The current assets minus the current liabilities…most businesses would like the current assets to be twice as big as the current liabilities.

The part of the profit paid to the shareholders…usually expressed as pence per share…e.g. 5p per share means that you will get 5p for every share you own.

Net Profit × 100 Turnover If this was 12% then the business would be keeping 12p from every £ of sales.

Someone who the business owes money to…often a supplier who allows one month’s credit on the stock delivered. It is not usual to be charged interest on such trade credit.

The amount of money which has been put into the business…either by the owners/ shareholders or been borrowed by the business.

People who owe money to a business…if they are unable to pay in the end then the debt will have to be forgotten about…it becomes a bad debt. Businesses obviously need to be careful who they give credit to.

Turnover minus the cost of the goods sold e.g. a retailer buys in stocks of clothes for £20000 and sells them for £35000…the profit in question on these sales would be £15000.

Profit made which has not been given to the shareholders as a dividend payment.

Items which are owned and will stay in the business over a long time … e.g. machines, tills, counters, delivery vans etc.

This is what a firm will charge its customers for the goods or service being sold.

Shown in the balance sheet. This is the amount of money that belongs to or is put into the business by the shareholders.

Fixed cost plus the variable cost.

![Target Profit Price = total costs [at Level X] + Target profit](https://cdn3.slideserve.com/6116031/slide1-dt.jpg)