Introduction to Financial Econometrics: Matrix Fundamentals

This document outlines the foundational concepts of matrices in financial econometrics, authored by Otavio Medeiros. It covers essential definitions, including dimensions, vector types, matrix operations, properties, and special matrices like identity, diagonal, and zero matrices. The material also discusses advanced topics such as the rank of a matrix, determinants, inverse matrices, and the steps to calculate them. Understanding these concepts is crucial for applying econometric techniques in financial analysis and modeling.

Introduction to Financial Econometrics: Matrix Fundamentals

E N D

Presentation Transcript

UnB Programa de Pós-Graduação em Administração Programa Multiinstitucional e Interregional de Pós-Graduação em Ciências Contábeis UnB-UFPB-UFRN Financial Econometrics I The Matrix Otavio R. de Medeiros UnB - Financial Econometrics I Otavio Medeiros

Matrices • A Matrix is a collection or array of numbers • Size of a matrix is given by number of rows and columns R x C • If a matrix has only one row, it is a row vector • If a matrix has only one column, it is a column vector • If R = C the matrix is a square matrix UnB - Financial Econometrics I Otavio Medeiros

Definitions • Matrix is a rectangular array of real numbers with R rows and C columns. are matrix elements. UnB - Financial Econometrics I Otavio Medeiros

Definitions • Dimension of a matrix: R x C. • Matrix 1 x 1 is a scalar. • Matrix R x 1 is a column vector. • Matrix 1 x C is a row vector. • If R = C, the matrix is square. • Sum of elements of leading diagonal = trace. • Diagonal matrix : square matrix with all elements off the leading diagonal equal to zero. • Identity matrix: diagonal matrix with all elements in the leading diagonal equal to one. • Zero matrix: all elements are zero. UnB - Financial Econometrics I Otavio Medeiros

Definitions • Rank of a matrix: is given by the maximum number of linearly independent rows or columns contained in the matrix, e.g.: UnB - Financial Econometrics I Otavio Medeiros

Matrix Operations • Equality: A = B if and only if A and B have the same size and aij = bij " i, j. • Addition of matrices: A+B= C if and only if A and B have the same size and aij + bij = cij " i, j. UnB - Financial Econometrics I Otavio Medeiros

Matrix operations • Multiplication of a scalar by a matrix: k.A = k.[aij], i.e. every element of the matrix is multiplied by the scalar. UnB - Financial Econometrics I Otavio Medeiros

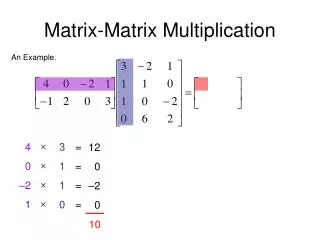

Matrix operations • Multiplication of matrices: if A is m x n and B is n xp, then the product of the 2 matrices is A.B = C, where C is a m x p matrix with elements: • Example: Note: A.B ¹ B.A UnB - Financial Econometrics I Otavio Medeiros

Transpose of a matrix • matrix transpose: if A is m x n, then the transpose of A is n x m, i.e.: UnB - Financial Econometrics I Otavio Medeiros

Properties of transpose matrices • (A+B)+C=A+(B+C) • (A.B).C=A(B.C) UnB - Financial Econometrics I Otavio Medeiros

PROJEÇÕES • Propriedades: UnB - Financial Econometrics I Otavio Medeiros

Square matrices : • Identity matrix I: Note: A.I = I.A = A, where A has the same size as I. UnB - Financial Econometrics I Otavio Medeiros

Square matrices : • Diagonal matrix: UnB - Financial Econometrics I Otavio Medeiros

Square matrices: • Scalar matrix = diagonal matrix, when l1 = l2 = ... =ln . • Zero matrix: A + 0 = A; A x0 = 0. UnB - Financial Econometrics I Otavio Medeiros

Trace of a matrix: If A is m x n and B is n x m, then AB and BA are square matrices and tr(AB) = tr (BA) UnB - Financial Econometrics I Otavio Medeiros

Determinants • matrix 2 x 2: UnB - Financial Econometrics I Otavio Medeiros

Determinants • matrix 3 x 3: UnB - Financial Econometrics I Otavio Medeiros

Determinants • Matrix 3 x 3: UnB - Financial Econometrics I Otavio Medeiros

Inverse matrix • The inverse of a square matrix A, named A-1, is the matrix which pre or post multiplied by A gives the identity matrix. • B = A-1 if and only if BA = AB = I • Matrix A has an inverse if and only if det A ¹ 0 (i.e. A is non singular). • (A.B)-1 = B-1.A-1 • (A-1)’=(A’)-1\ if A é symmetrical and non singular, then A-1 is symmetrical. • If det A ¹ 0 and A is a square matrix of size n, then A has rank n. UnB - Financial Econometrics I Otavio Medeiros

Steps for finding an inverse matrix • Calculation of the determinant: Kramer’s rule or cofactor matrix. • Minor of the element aij is the determinant of the submatrix obtained after exclusion of the i-th row and j-th column. • Cofactor is the minor multiplied by (-1)i+j, UnB - Financial Econometrics I Otavio Medeiros

Steps for finding an inverse matrix • Laplace expansion: take any row or column and get the determinant by multiplying the products of each element of row or columns by its respective cofactor. • Cofactor matrix: matrix where each element is substituted by its cofactor. UnB - Financial Econometrics I Otavio Medeiros

Example 2 x 2 matrix : UnB - Financial Econometrics I Otavio Medeiros

Example • 3 x 3 matrix : UnB - Financial Econometrics I Otavio Medeiros

Matrix differentiation: UnB - Financial Econometrics I Otavio Medeiros

Matrix differentiation: UnB - Financial Econometrics I Otavio Medeiros

Matrix differentiation: UnB - Financial Econometrics I Otavio Medeiros

Linear regression, example 1: Perform a linear regression, given that the data for the dependent variable are 1, 2, 1, 2, 2 and for the independent variable are 1, 2, 2, 3, 3. Solution: Since a = 0.5 e b = 0.5, the regression equation is yt = 0.5 + 0.5xt UnB - Financial Econometrics I Otavio Medeiros

Linear regression, example 2: a firm manufacturing bikes is preparing a project and wishes to find out what is the relationship between bike sales and national income (GDP). In the last 5 years, bike sales increased by 5%, 9%, 5%, 6% and 10%, whereas GDP increased by 2,5%, 4%, 3%, 2,5%, 4%. What is the relationship between bike sales and GDP? UnB - Financial Econometrics I Otavio Medeiros

Example 2: Solution 1 The past relationship between bike sales growth and GDP growth is given by: yt = -0.0204 + 2.826xt UnB - Financial Econometrics I Otavio Medeiros

Example 2: Solution 2 Hint: to avoid working with decimals, we can multiply y and x by 100. To find the correct final result, divide a by 100. b doesn’t change. UnB - Financial Econometrics I Otavio Medeiros

Graph (Excel): UnB - Financial Econometrics I Otavio Medeiros

Goodness of fit: • A measure of the goodness of fit of a regression is the coefficient of determination R2, which is defined as: UnB - Financial Econometrics I Otavio Medeiros

Goodness of fit: • When all the residuals are equal to nil, R2 = 1, meaning that the regression is perfect, with all data points located on the line. • When then R2 = 0, meaning that there is no regression. • Hence, the range for R2 will be: 0 < R2< 1 • Values of R2 close to 1 indicate a good regression, while low values of R2 indicate a bad or inexisting regression. UnB - Financial Econometrics I Otavio Medeiros

Calculation of R2 – Example 1: UnB - Financial Econometrics I Otavio Medeiros

Calculation of R2 – Example 2: UnB - Financial Econometrics I Otavio Medeiros