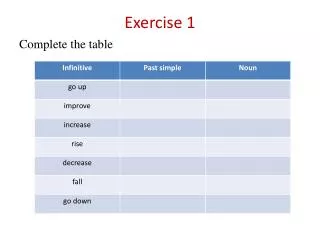

Exercise 1

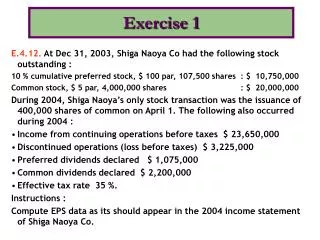

Exercise 1. E.4.12. At Dec 31, 2003, Shiga Naoya Co had the following stock outstanding : 10 % cumulative preferred stock, $ 100 par, 107,500 shares : $ 10,750,000 Common stock, $ 5 par, 4,000,000 shares : $ 20,000,000

Exercise 1

E N D

Presentation Transcript

Exercise 1 E.4.12. At Dec 31, 2003, Shiga Naoya Co had the following stock outstanding : 10 % cumulative preferred stock, $ 100 par, 107,500 shares : $ 10,750,000 Common stock, $ 5 par, 4,000,000 shares : $ 20,000,000 During 2004, Shiga Naoya’s only stock transaction was the issuance of 400,000 shares of common on April 1. The following also occurred during 2004 : • Income from continuing operations before taxes $ 23,650,000 • Discontinued operations (loss before taxes) $ 3,225,000 • Preferred dividends declared $ 1,075,000 • Common dividends declared $ 2,200,000 • Effective tax rate 35 %. Instructions : Compute EPS data as its should appear in the 2004 income statement of Shiga Naoya Co.

Answer of Exercise 1 Net Income Income from continuing operations before taxes $ 23,650,000 Income taxes (35 %) $ 8,277,500 Income from continuing operations $ 15,372,500 Discontinued operations Loss before taxes $ 3,225,000 Less applicable income tax (35 %) $ 1,128,750$ 2,096,250 Net income $ 13,276,250 Preferred dividends declared $ 1,075,000 Weighted average common shares outstanding Period Dec 31, 2003 – March 31, 2004 (4,000,000 x 3/12) 1,000,000 Period April 1, 2004 – Dec 31,2004 (4,400,000 x 9/12) 3,300,000 Weighted average 4,300,000 Earnings Per Share Income from continuing operations $ 3.33 Discontinued operations $ (0.49) Net income $ 2.84 ($ 15,372,500,- $ 1,075,000) : 4,300,000 = 3.33 ($ 2,096,250 : 4,300,000) = 0.49 ($ 13,276,250 - $ 1,075,000) : 4,300,000 = 2.84

Exercise 2 P.4.1. Presented below is information related to American Horse Co for 2004 : • Retained earnings balance, Jan 1,2004 $ 980,000 • Sales for the year $ 25,000,000 • COGS $ 17,000,000 • Interest revenue $ 70,000 • Selling and administrative expenses $ 4,700,000 • Write off of goodwill (not tax deductible) $ 820,000 • Income taxes for 2004 $ 905,000 • Gain on the sale of investments (normal recurring) $ 110,000 • Loss due to flood damage-extraordinary item (net of tax) $ 390,000 • Loss on the disposition of wholesale division (net of tax) $ 440,000 • Loss on operations of the wholesale division (net of tax) $ 90,000 • Dividends declared on common stock $ 250,000 • Dividend declared on preferred stock $ 70,000 Instructions : Prepare a multiple step income statement and a retained earnings statement. American Horse decided to discontinue its entire wholesale operations and retain its manufacturing operations. On Sept 15, American Horse sold the wholesale operations to Rogers Co. During 2004 there were 300,000 shares of common stock outstanding all year.

Answer of Exercise 2 American Horse Co Income Statement For the year ended Dec 31,200 Sales $ 25,000,000 COGS $ 17,000,000 Gross profit $ 8,000,000 Selling and administrative expenses $ 4,700,000 Income from operations $ 3,300,000 Other revenues and gains Interest revenue $ 70,000 Gain on the sale of investments $ 110,000 $ 180,000 Other expenses and losses Write off goodwill $ 820,000 Income from continuing operations before income taxes $ 2,660,000 Income taxes $ 905,000 Income from continuing operations $ 1,755,000 Discontinued operations Loss on operations, net of tax $ 90,000 Loss on disposal, net of tax $ 440,000$ 530,000 Income before extraordinary item $ 1,225,000 Extraordinary loss from flood damage, net of tax $ 390,000 Net income $ 835,000

Answer of Exercise 2 American Horse Co Retained Earnings Statement For the year ended Dec 31,200 Retained earnings, January 1,2004 $ 980,000 Net income $ 835,000 $ 1,815,000 Dividends Preferred stock $ 70,000 Common stock $ 250,000$ 320,000 Retained earnings, December 31,2004 $ 1,495,000 Earnings Per Share Income from continuing operations $ 5.62 Discontinued operations Loss on operations (net of tax) $ (0.30) Loss on disposal (net of tax) $ (1.47)$ (1.77) Income before extraordinary items $ 3.85 Extraordinary loss (net of tax) $ (1.30) Net income $ 2.55 ($ 1,755,000 - $ 70,000) : 300,000 = $ 5.62 ($ 1,225,000 - $ 70,000) : 300,000 = $ 3.85 ($ 835,000 - $ 70,000) : 300,000 = $ 2.55