Download

1 / 43

430 likes | 954 Vues

Equilibrium Prices and Equilibrium Quantities. Finding the right balance Unit Essential Question: How does economic self-interest contribute to the greater good?. Delaware Standard. Economics 1 Microeconomics

E N D

Equilibrium Prices and Equilibrium Quantities Finding the right balance Unit Essential Question: How does economic self-interest contribute to the greater good?

Delaware Standard • Economics 1 • Microeconomics • Students will demonstrate how individual economic choices are made within the context of a market economy in which markets influence the production and distribution of goods and services.

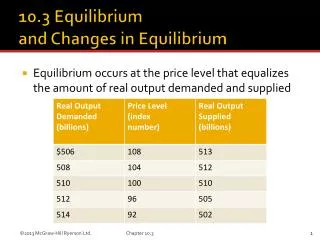

The forces of supply and demand work together to establish a price where the mount of stuff we want is the same as what producers are willing to give us. This MAGIC point is constantly changing depending on market conditions. It is called the EQUILIBRIUM PRICE. • REMEMBER: prices provide information and incentives to buyers and sellers

Lesson Essential Question • In a market, who or what determines the equilibrium price?

Concepts • Demand • Supply • Equilibrium price • Quantity demanded • Quantity supplied • Shortage • Surplus

Economic Principles • Buyers and sellers determine market prices which determine how resources should be allocated. • Prices send signals to buyers and sellers and provide incentives.

But what happens if… • We quickly shift the bowl? • The table the bowl is sitting on is wobbly? • An earthquake strikes and shakes everything? • My cats decide the ball in the bowl is a toy and begin batting it around? I couldn’t resist this cute picture

The answer is… • The ball will move around for a while • But (because of gravity) the ball always wants to come to a rest back in the bottom of the bowl • The entire bowl may now be in a different place or be tilted, but the ball always tries to come to a rest in the bottom • Think of gravity like the natural forces of the market: • It always wants to find equilibrium • But sometimes it might not be able to… I think I just found Equilibrium!

Yo-yos Hundreds of yo-yos

So in the real world the price of yo-yos SHOULD be $3.00. But how does a Target manager know what to price these new yo-yos at? What if she prices the yo-yos at $4.00? (but the equilibrium was actually at $3)

Yo-yos Surplus of 800 yo-yos Hundreds of yo-yos

How would Target get rid of the surplus – the extra 800 yo-yos no one is buying? Correct. Keep lowering the price until the quantity demanded equals the quantity supplied. This would happen at $3 and at 1,000 yo-yos.

What if the Target manager was just guessing at prices and set the actual price at $2.00? (again, the equilibrium price, or the price the market wants to settle at is still at $3.00)

Yo-yos Shortage of 800 Yo-yos Hundreds of yo-yos

Which buyers will get the yo-yos? The buyers willing and able to pay more money will get the yo-yos. Hasbro responds to the higher price by producing more yo-yos. This puts pressure on the price to increase. This happens until we are back at $3.00 and 1,000 yo-yos again (equilibrium).

Only at $3.00 is the quantity demanded equal to the quantity supplied (1,000 yo-yos). Equilibrium is a mutual agreement of consumers and producers. Equilibrium may change though,ifmarket conditions change (like when a determinant of supply or a determinant of demand or both happen)

Lesson Essential Question • In a market, who or what determines the equilibrium price?

Plotting Demand for and Supply of Frisbees Millions of frisbees

Part F • Uh-oh!!! • The cost of plastic increases. Plastic is a main ingredient (input) when making frisbees. • This will change the supply of frisbees because Hasbro can’t make as many frisbees for the same amount of money any more.

Plotting Demand for and Supply of Frisbees Millions of frisbees

Part G • Uh-oh again!! • Lots of people lose their jobs or have to take pay cuts. This means they have less income and it means demand will decrease as a result because they will not be as willing and/or able to buy things. • With our new supply curve and equilibrium, what will happen with a new demand curve also?

Plotting Demand for and Supply of Frisbees Millions of frisbees

The new or final equilibrium is labeled E3. • It is the price where the new quantity supplied is equal to the new quantity demanded. • What happens to Equilibrium Price? This example just happens to be back at our original price, but in the real world it may be at a new higher or new lower price than the original. Price might be indeterminant. • What happens to Equilibrium Quantity? It decreases AGAIN to 100million frisbees.

Lesson Essential Question • In a market, who or what determines the equilibrium price?

Review • What tends to happen to price if it is above equilibrium? • What do we call this situation? • What tends to happen to price if it is below equilibrium? • What do we call this situation?

More review For each of the following situations, predict the 1) change in the equilibrium price and equilibrium quantity of turkeys and 2) explain your reasoning (what determinant happened and why did things change?). Draw the graph to illustrate your answer!

TURKEYS Price Quantity

Turkey is called a “health food” by the U.S. Surgeon General as eating turkey is found to reduce your risk of cancer, diabetes and heart disease.

TURKEYS Price Quantity

Really look at what just happened. It seems good that turkey is now found to be healthy. And maybe it is good! BUT…the price of turkey increases. It’s true that a larger quantity will be supplied and purchased, but only by those people who can afford it at the higher prices. Great for turkey farmers! That will leave some people (demanders) out! Or you may have to give up something else to keep buying the expensive turkey. Or you could just quit turkey cold turkey. Get it??

New situation…so back to your original turkey graph (assume the Surgeon General said nothing!) • New technology is developed by UofD’s agricultural science department that helps turkeys breed faster. (ok, don’t laugh!)

TURKEYS Price Quantity

Again, think about it. More turkey will be produced, but if you look at the graph, it is at a lower price. Good for you and me right? Yes, as consumers. But not if you own a turkey farm that can’t continue to supply turkey at that low price. More turkeys are supplied but by fewer producers. This means some people might lose their jobs. Are the lost farm jobs offset by the lower price of turkeys to society?

New situation…so back to your original turkey graph • The federal government, under pressure from whack-o’s, abolishes Thanksgiving and makes it illegal to celebrate the holiday. (notice they didn’t say you couldn’t grow turkeys)

TURKEYS Price Quantity

This time you tell me what is going on… Less demand = Lower prices. Less turkeys produced. Not such good news if you are a turkey farmer again!

Lesson Essential Question • In a market, who or what determines the equilibrium price?