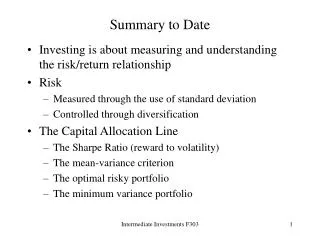

Summary to Date

Learn how to measure and control investment risk through diversification, the Capital Allocation Line, Sharpe Ratio, and optimal portfolio selection methods. Discover the importance of standard deviation and the benefits of diversification in constructing a portfolio.

Summary to Date

E N D

Presentation Transcript

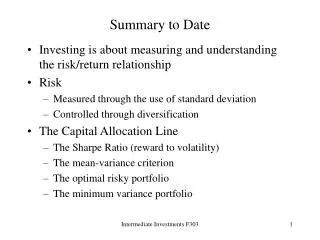

Summary to Date • Investing is about measuring and understanding the risk/return relationship • Risk • Measured through the use of standard deviation • Controlled through diversification • The Capital Allocation Line • The Sharpe Ratio (reward to volatility) • The mean-variance criterion • The optimal risky portfolio • The minimum variance portfolio Intermediate Investments F303

Summary to Date • While the return of a portfolio made up of two assets is simply the weighted average, the standard deviation is only a weighted average if the assets are perfectly correlated • Otherwise, the standard deviation is something less than the weighted average, showing the benefits of diversification! Intermediate Investments F303

The Optimal Risky Portfolio • Optimal Risky Portfolio (p. 200 has an error) WA = (RPA) * (VARZ) – (RPZ)(SDA)(SDB)(RhoAZ) --------------------------------------------------------------------------- (RPA)*(VARZ) + (RPZ)*(VARA) -(RPA+RPZ)(SDA)(SDZ)(RhoAZ) Intermediate Investments F303

The Minimum Variance Portfolio • Minimum Variance Portfolio (p. 197) WA = (VARZ) – (SDA)(SDZ)(RhoAZ) ------------------------------------------------------ (VARZ) + (VARA) – 2(SDA)(SDZ)(RhoAZ) Intermediate Investments F303