Exchange rates

E N D

Presentation Transcript

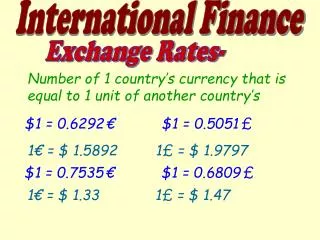

Exchange rates Currencies are bought and sold in the foreign exchange market. The price at which one currency exchanges for another in the foreign exchange market is called the exchange rate. For example, suppose one U.S. dollar buys 0.80 euros, i.e., 80 European cents. Therefore, $1 = €0.80 which means that 1 ____ €1 = = $1.25. 0.80

Thus the euro exchange rate in terms of dollars is just the reciprocal of the dollar exchange rate in terms of euros. Why? 0.80 is the number of euros per dollar, or €/$. If we want to obtain the number of dollars per euro, or $/€, then 1 1 ____ ____ $/€ = = = $1.25. €/$ 0.80

The market for currencies is derived from the international market for goods and services and assets. For example, when Americans buy goods or assets from a foreign country, they must obtain some of the foreign country’s currency in order to make the transaction. This gives rise to a supply of dollars and a demand for the foreign currency in the foreign exchange market. Similarly, when foreigners buy American goods or assets, they must first acquire dollars, which gives rise to a supply of the foreign currency and a demand for dollars in the foreign exchange market.

The demand for dollars The quantity of U.S. dollars demanded in the foreign exchange market is the amount of dollars that traders plan to buy during a given time period at a given exchange rate. Foreign residents demand dollars because of the U.S. goods and services (U.S. exports) and assets (bonds, stocks, bank deposits) the dollars can buy them. The lower the dollar exchange rate (euros per dollar) the greater is the quantity of dollars demanded; the higher the dollar exchange rate, the less is the quantity of dollars demanded:

A currency depreciation is the fall in the value of one currency in terms of another currency. For example, if the dollar falls from €0.80 to €0.75, the dollar has depreciated against the euro by approximately 6%. Vice versa, a currency appreciation is the rise in the value of one currency in terms of another. For example, if the dollar falls from €0.80 to €0.75, this means the euro has appreciated from $1.25 to $1.33 (1/0.75 = 1.33), which is approximately a 6% appreciation.

Why is there an inverse relationship between the quantity of dollars demanded and the price of the dollar in euros? The lower the dollar exchange rate, or in other words the weaker the dollar relative to the euro, the cheaper are American goods and services to Europeans: fewer euros are required to buy a dollar, or, in other words, a euro buys more dollars and therefore more American goods and services. Therefore Europeans demand more American goods and services, and consequently they must buy more dollars in order to buy these goods and services. Therefore the quantity of dollars demanded by Europeans increases.

Factors that shift the demand curve for dollars interest rates in the U.S. and in other countries the expected future exchange rate. Interest rates: The higher the interest rate on U.S. financial assets (bonds, bank deposits) compared to foreign assets, the more U.S. assets will be purchased, both by Americans and by foreigners. What matters is not the level of U.S. interest rates by itself, but the U.S. interest rate minus the foreign interest rate. This gap is called the U.S. interest rate differential.

If the U.S. interest rate differential increases, there will be an increase in the demand for dollars. Foreigners will be more interested in purchasing U.S. assets (and less interested in purchasing their own assets) and therefore, at any given exchange rate, they will be more interested in purchasing dollars. The demand curve for dollars will shift to the right. Expected future exchange rate: The higher the expected future exchange rate, the greater is the expected profit from holding dollars and the greater is the demand for dollars. If people expect the dollar to be stronger in the future, they will buy more dollars at any given current exchange rate and the demand curve for dollars will shift to the right.

The supply of dollars The quantity of U.S. dollars supplied in the foreign exchange market is the amount of dollars that traders plan to sell during a given time period at a given exchange rate. U.S. residents supply dollars in exchange for foreign currency in order to buy foreign goods and services (U.S. imports) and assets (bonds, stocks, bank deposits). The higher the dollar exchange rate (euros per dollar) the greater is the quantity of dollars supplied; the lower the dollar exchange rate, the less is the quantity of dollars supplied:

Why is there a positive relationship between the quantity of dollars supplied and the price of the dollar in euros? The higher the dollar exchange rate, or in other words the stronger the dollar relative to the euro, the cheaper are European goods and services to Americans: fewer dollars are required to buy a euro, or, in other words, a dollar buys more euros and therefore more European goods and services. Therefore Americans demand more European goods and services, and consequently they must sell more dollars, i.e., buy more euros, in order to buy these goods and services. Therefore the quantity of dollars supplied by Americans in exchange for euros increases.

Factors that shift the supply curve of dollars interest rates in the U.S. and in other countries the expected future exchange rate. Interest rates: The higher the interest rate on U.S. financial assets (bonds, bank deposits) compared to foreign assets, the more U.S. assets will be purchased, both by Americans and by foreigners. Again, what matters is not the level of U.S. interest rates by itself, but the U.S. interest rate minus the foreign interest rate, i.e., the U.S. interest rate differential.

If the U.S. interest rate differential increases, there will be a decrease in the supply of dollars. Americans will be more interested in purchasing their own domestic assets (and less interested in purchasing foreign assets) and therefore, at any given exchange rate, they will be less interested in selling dollars in exchange for euros. The supply curve of dollars will shift to the left.

Expected future exchange rate: The higher the expected future exchange rate, the greater is the expected profit from holding off on selling dollars today and waiting for their price to rise in the future; hence the supply of dollars today will decrease. If people expect the dollar to be stronger in the future, they will sell less dollars at any given current exchange rate and the supply curve of dollars will shift to the left. Market clearing equilibrium At the market clearing equilibrium exchange rate, the quantity of dollars demanded is equal to the quantity supplied:

If there is an excess supply of dollars, as there is at an exchange rate of €0.85, this means that at the prevailing exchange rate, because the euro is so cheap and the dollar is so expensive, Americans are buying more goods from Europeans than Europeans are buying from Americans. Therefore, an excess supply of dollars means that the U.S. has a trade deficit (U.S. imports exceed U.S. exports) while Europe has a trade surplus (European exports exceed European imports).

If there is an excess demand for dollars, as there is at an exchange rate of €0.75, this means that at the prevailing exchange rate, because the dollar is so cheap and the euro is so expensive, Europeans are buying more goods from Americans than Americans are buying from Europeans. Therefore, an excess demand for dollars means that the U.S. has a trade surplus (U.S. exports exceed U.S. imports) while Europe has a trade deficit (European imports exceed European exports).

Assuming floating or flexible exchange rates, which means that exchange rates are free to adjust to equilibrium, these trade imbalances are eliminated automatically through competitive market forces. For example, as the dollar exchange rate weakens from €0.85 to €0.80, the quantity of European goods demanded by Americans decreases and the quantity of American goods demanded by Europeans increases, thereby eliminating the excess supply of dollars and also eliminating the U.S. trade deficit and the European trade surplus.

As the dollar exchange rate strengthens from €0.75 to €0.80, the quantity of American goods demanded by Europeans decreases and the quantity of European goods demanded by Americans increases, thereby eliminating the excess demand for dollars and also eliminating the U.S. trade surplus and the European trade deficit. Changes in the equilibrium exchange rate If the demand curve for dollars and/or the supply curve of dollars shift, the market clearing equilibrium exchange rate will change.

Both the supply of and demand for dollars are influenced by the U.S. interest rate differential and by expected future exchange rates. When these influences change, both the supply curve and the demand curve shift, but they shift in opposite directions. For example, suppose there is a decrease in the expected future exchange rate of the dollar. As we have seen, a decrease in the dollar’s expected future exchange rate will cause a decrease in the demand for dollars (a leftward shift of the demand curve for dollars) and also an increase in the supply of dollars (a rightward shift of the supply curve of dollars):

Thus a decrease in the dollar’s expected future exchange rate causes the market clearing equilibrium exchange rate of the dollar to depreciate. As another example, suppose U.S. GDP is increasing while Europe is in a recession. U.S. interest rates would rise because, as we have seen, in a business cycle expansion there is increasing demand for investment funds due to enhanced profit expectations on the part of businesses. European interest rates would fall because in a recession profit expectations decrease and businesses demand less funds for investment purposes. Therefore, the U.S. interest rate differential increases.

As we have see, an increase in the U.S. interest rate differential causes the demand for dollars to increases and the supply of dollars to decrease:

Thus an increase in the U.S. interest rate differential causes the market clearing equilibrium exchange rate of the dollar to appreciate. Exchange rate expectations We have seen that a change in the expected future exchange rate can cause the market clearing equilibrium exchange rate to change. But what causes expectations to change? One of the major factors driving exchange rate expectations is the presence or absence of purchasing power parity (PPP).

PPP means that money buys the same basket of goods and services in different countries irrespective of which currency is used. Thus, for example, if PPP prevails, a dollar buys the same goods and services in Europe, when converted into euros, as it would buy at home. If prices rise in Europe relative to prices in the U.S., assuming no change in the exchange rate, then a dollar, when converted into euros, will buy fewer goods and services in Europe than it does in the U.S. and PPP will not hold.

If prices were to rise faster in the U.S. than in Europe, and again assuming the exchange rate remains constant, then a dollar will actually buy more goods and services in Europe than it would at home, and again the PPP condition would not hold. Thus PPP depends on the aggregate price level in one country relative to that of another country. To determine whether PPP prevails we really need to look at the price level, i.e., the prices of all goods and services, in both countries.

However, as a rough approximation, and to illustrate the meaning of PPP, we will use the The Economist magazine’s “Big Mac index,” which is based on the price of a Big Mac in every different country in which McDonald’s operates. Suppose the dollar-euro exchange rate is $1 = €0.80. Also assume that the average price of a Big Mac in the U.S. is $3.00. In Europe suppose the average price of a Big Mac is €2.70. In this case, PPP does not exist: at an exchange rate of $1 = €0.80, the euro equivalent of $3.00 would be (3 X 0.80 =) €2.40. But a Big Mac in Europe actually costs €2.70, which is the equivalent of (2.70/0.80 =) $3.38.

Thus the dollar has less purchasing power in Europe than it does in the U.S.: the euro is too expensive, the dollar is too cheap. If the euro were cheaper, i.e., if a dollar exchanged for €0.90 instead of €0.80, then PPP would exist. At an exchange rate of $1 = €0.90, the euro equivalent of $3 would be (3 X 0.90 =) €2.70. Now the price of a Big Mac is identical in both countries: $3 will buy a Big Mac in both the U.S. and in Europe. This example illustrates the point that, if PPP does not hold, given the price levels in the two countries, then the exchange rate needs to adjust in order to restore PPP.

In the Big Mac example, prices are higher in Europe than in the U.S., therefore the dollar starts out being too cheap and the euro too expensive. Judged by the PPP standard, the dollar is undervalued and the euro is overvalued. The dollar needs to appreciate (the euro needs to depreciate) in order to bring about PPP. If Europe has a higher inflation rate than the U.S., and the euro exchange rate does not adjust automatically, then the euro will become overvalued (too expensive) relative to the dollar and PPP will not exist. Currency traders would then expect the euro to depreciate and the dollar to appreciate. Why would they expect this?

If prices are higher in Europe than in the U.S., there will be an increase in the demand for dollars, as Europeans buy more American goods, and a decrease in the supply of dollars, as Americans offer less dollars in exchange for euros since they are now less interested in buying European goods. The combined effect of an increase in the demand for dollars and a decrease in the supply of dollars is an increase in the market clearing equilibrium dollar exchange rate, i.e., an appreciation of the dollar (depreciation of the euro).

However, the foreign exchange market is very efficient. Traders in the market will not sit around waiting for the euro to depreciate and the dollar to appreciate. As soon as they realize that PPP does not hold between the euro and the dollar, they will expect the euro to depreciate and the dollar to appreciate. And as we have seen, an increase in the expected future value of the dollar will immediately cause an increase in the demand for dollars and a decrease in the supply of dollars, so that the dollar will immediately appreciate in response to these expectations.

Fixed exchange rates So far we have assumed that the dollar-euro exchange rate is floating or flexible, i.e., free to adjust to equilibrium in response to shifts of supply and demand. However, sometimes the monetary authorities in a country will choose to have a fixed exchange rate. Under a fixed exchange rate regime, the central bank announces an official exchange rate, which need not necessarily coincide with the market clearing equilibrium exchange rate.

Suppose, hypothetically, that the Fed wanted to fix the dollar-euro exchange rate at €0.85 per dollar, which is above the market clearing equilibrium exchange rate of €0.80 per dollar. At an exchange rate of $1 = €0.85, the dollar is overvalued. Normally, under floating exchange rates, market forces would bring the exchange rate back to equilibrium at $1 = €0.80. But the Fed wants to keep the exchange rate at $1 = €0.85. To maintain the overvalued exchange rate of $1 = €0.85, the Fed will need to intervene in the foreign exchange market by buying dollars, which decreases the supply of dollars in circulation:

When the Fed enters the foreign exchange market to buy dollars, the supply of dollars decreases from S0 to S1. The Fed would need to keep buying dollars in order to maintain the market equilibrium exchange rate at €0.85 per dollar. The Fed’s foreign exchange market intervention affects the domestic monetary base and therefore the money supply in the U.S. The dollars that the Fed buys are removed from circulation, which shrinks the domestic monetary base and decreases the overall money supply.

The decrease in the money supply is deflationary: recall from the equation of exchange, M.V = P.Y, that if velocity, V, is stable and real GDP, Y, is constant at the full employment level or potential GDP, then any decrease in the money supply, M, will cause an equal proportional decrease in the price level, P. Thus we can conclude that, for a country’s central bank to keep the currency permanently overvalued, it must create domestic deflation. Deflation, by increasing the purchasing power of the currency, means that the currency would no longer be overvalued at the higher exchange rate.

Alternatively, suppose that the Fed wanted to fix the dollar-euro exchange rate at €0.75 per dollar, which is below the market clearing equilibrium exchange rate of €0.80 per dollar. At an exchange rate of $1 = €0.75, the dollar is undervalued. Normally, under floating exchange rates, market forces would bring the exchange rate back to equilibrium at $1 = €0.80. But the Fed wants to keep the exchange rate at $1 = €0.75. To maintain the undervalued exchange rate of $1 = €0.75, the Fed will need to intervene in the foreign exchange market by selling dollars, which increases the supply of dollars in circulation:

When the Fed enters the foreign exchange market to sell dollars, the supply of dollars increases from S0 to S1. The Fed would need to keep selling dollars in order to maintain the market equilibrium exchange rate at €0.75 per dollar. The Fed’s foreign exchange market intervention again affects the domestic monetary base and therefore the money supply in the U.S. In order to have enough dollars to sell, the Fed will need to expand the domestic monetary base and hence the overall money supply.

The increase in the money supply is inflationary: recall from the equation of exchange, M.V = P.Y, that if velocity, V, is stable and real GDP, Y, is constant at the full employment level or potential GDP, then any increase in the money supply, M, will cause an equal proportional increase in the price level, P. Thus we can conclude that, for a country’s central bank to keep the currency permanently undervalued, it must create domestic inflation. Inflation, by reducing the purchasing power of the currency, means that the currency would no longer be undervalued at the lower exchange rate.

Thus, while under a floating exchange rate regime, the exchange rate itself adjusts to bring about equilibrium in the foreign exchange market (and eliminate trade imbalances – deficits and surpluses – between countries), under fixed exchange rates it is the domestic price level, and therefore nominal GDP, that must adjust instead.