Cost Analysis

This comprehensive overview explores cost analysis in business, highlighting the importance of economic scale, opportunity costs, and competition. It addresses how firms that remain complacent may be driven out of the market by competitors who produce at lower costs. A comparison of accounting and economic costs reveals the hidden expenses that can affect profitability. The text further investigates how short-run and long-run cost functions impact production decisions, emphasizing the balance between fixed and variable costs. Understanding these concepts is crucial for managers seeking to optimize production while maintaining quality.

Cost Analysis

E N D

Presentation Transcript

Cost Analysis Mohammad Arief

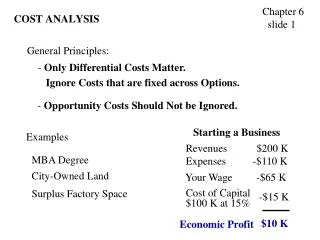

Overview Competitors arise that produce at lower costs Firms that are satisfied with the status quo. Economic Scale Drive them out of business The advantages of a large firm have NOT provided the advantages of flexibility and agility found in some smaller companies Operations Activity. Opportunity Cost Concept Attracting a resource from its best alternative COST Cost analysis is helpful in the task of finding lower cost methods to produce goods and services Managers seek to produce the highest quality products at the lowest possible cost.

Meaning and Measurement of Costs In elementary form COST Refers to the exchangeor transformation of resources takes place. Economics cost Opportunity Cost Information

Accounting vs Economic Cost • Accounting costs involve explicit historical costs. They attempt to use the same rules for different firms, so we can compare firm performance. • Economic costs are based on making decisions. These costs can be both implicit and explicit. • A chief example is that economic costs include the opportunity costs of owner-supplied resources such as time and money, which are implicit costs. • Economic Profit = the difference between total revenues and these totaleconomic costs, implicit opportunity costs as well as explicit outlays. Total Revenues - Explicit Costs - Implicit Costs • Both explicit and implicit costs make economic profit lower than accounting profit

Contrasts between Accountingand Economic Costs • Depreciation Cost Measurement. Accounting depreciation (e.g., straight-line depreciation) tends to have little relationship to the actual loss of value • To an economist, the actual loss of value is the true cost of using machinery • Inventory Valuation. Accounting valuation depends on its acquisition cost • Economists view the cost of inventory as the cost of replacement • Unutilized Facilities. Empty space may appear to have "no cost” • Economists view its alternative use (e.g., rental value) as its opportunity cost • Sunk Costs. Already paid for, or there already exists a contractual obligation to pay

SHORT-RUN COST FUNCTIONS To measuring the costs of producing a given quantity of output, economistsare also concerned with determining the behavior of costs when output is varied over a range of possible values. Cost Function Fixed Cost Variable Cost TC = FC + VC The costs of all the inputs to the production process that are fixed orconstant over the short run Consist of the costs of all the variable inputs to the production process

Short-Run Cost Graphs MC ATC 3. 1. AVC AFC AFC Q Q MCintersects lowest point of AVC and lowest point of ATC. When MC < AVC, AVC declines When MC > AVC, AVC rises 2. AVC Q

AP & AVC are inversely related. (ex: one input) AVC = WL /Q = W/ (Q/L) = W/ APL As APL rises, AVC falls MP and MC are inversely related MC = dTC/dQ = W dL/dQ = W / (dQ/dL) = W / MPL As MPL declines, MC rises Relationships Among Cost & Production FunctionsWhen Factor Markets Are Perfectly Competitive Q prod. functions AP MPL L cost AVC MC cost functions Q

LONG-RUN COST FUNCTIONS Over the long-run planning horizon, using the available production methods and technology,the firm can choose the plant size, types and sizes of equipment, labor skills, andraw materials that, when combined, yield the lowest cost of producing the desired amount of output. Optimal Capacity Utilization Optimal plant size Optimal output for a given plant size Optimal plant size for a given output rate Short-run concept of capacity utilization Reduced average total cost of any given output Will further opportunities for cost reduction cease

ECONOMIES AND DISECONOMIES OF SCALE Refer the condition whereas the proportionally output more faster than input. Economic Scale Technology Finance • Factors • Operating Scales increase • Specialization • Productive mechines • A firm size increase • Obligation offering • Bank loan • Bigger transaction (buying or selling the product)

Which include specialization and learning curve effects • Product-level economies Such as economies in overhead, required reserves, investment, or interactions among products (economies of scope). • Firm-level economies • Economic Scale Which are economies in distribution and transportation of a geographically dispersed firm, marketing, sales promotion, or R&D of multi-product firms • Plant-level economies

Diseconomic Scale • Rising long-run average costs at higher rates of throughput are attributed. • Factors • Individual production plant is transportation costs • Labor requirements • Higher wage rates • Relocation programs may be required to attract the necessary personnel Large-scale plants are often inflexibleoperations designed for long production runs of one product, based often on forecasts of what the target market wanted in the past