Demand Curve Notes

Demand Curve Notes. DEMAND Defined:. Demand : In economic terms, demand is the amount of a good or service that a consumer is willing and able to buy at all the various possible prices during a given time period. When represented graphically, DEMAND is the whole curve itself.

Demand Curve Notes

E N D

Presentation Transcript

DEMAND Defined: • Demand: In economic terms, demand is the amount of a good or service that a consumer is willing and able to buy at all the various possible prices during a given time period. • When represented graphically, DEMAND is the whole curve itself

Quantity Demanded • Quantity Demanded: the amount of a good or service that a consumer is willing and able to buy at each particular price point during a given time period. • When represented graphically, QUANTITY DEMANDED is the individual points on the curve

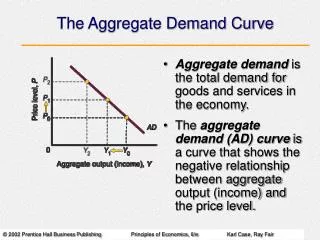

THE DEMAND CURVE The Demand Curve ALWAYS slopes this way

The Law of Demand • Law of Demand: states that an increase in a good’s price causes a decrease in the quantity demanded; and that a decrease in price causes an increase in the quantity demanded. • In a free-enterprise system, price is the main variable affecting Quantity demanded.

Purchasing Power • Purchasing Power: the amount of money, or income, that people have available to spend on goods and services. • Usually, as one’s purchasing power increases, their Demand will increase for a particular good/service as well.

Determinants of Demand • Determinants of Demand: Factors, OTHER THAN PRICE, that create more or less demand for a product or service. • These will shift the entire demand curve to the Left (less demand) or the Right (more demand). • ***A price change will only change the Quantity Demanded***

Determinants of Demand • Consumer Tastes • Ex. Bands, endorsements, “Going Green” • Number of Consumers (market size) • Embargos, New Technology can create new markets while hurting others. (Cell phones - Landline)

Determinants of Demand • Income • More $ = More likelihood of spending (Beef vs. Steak Problem) • Consumer Expectations • (Expecting a Raise, predicting future prices) • Prices of Related goods • Substitute & Complimentary

Price of Related Goods • Substitute Goods – A consumers tendency to switch to a lower priced, but similar product. (Butter vs. Margarine) • Complementary goods – Goods that are commonly used with other goods (Peanut Butter & Jelly) • ***Only 1 market will experience a Demand curve shift…..the other experiences a price change or Quantity Demanded

Practice • In groups of 2-3, imagine that you are the officers of a school club…..To raise money for your club, you are selling tickets to a dance. Your task is to think of ways to increase ticket sales without lowering the ticket prices….. • Come up with as many ideas as you can think of for ALL FIVE DETERMINATES OF DEMAND to shift the Demand Curve for dance tickets to the Right - - - - - - - - - - - - - >

Elasticity of Demand • Elastic Demand - When a small change in price GREATLY Changes the Quantity Demanded • The Demand Curve looks almost horizontal • These goods are Not Necessities • These goods have many substitutes

Elasticity of Demand • Inelastic Demand - When a change in price causes LITTLE or NO change in Quantity Demanded • The Demand Curve looks almost Vertical • These goods are more need based • These goods have few/no substitutes • These goods are very cheap (Salt or Soap)

Price Elasticity of Demand • PEoD = • (%Change in Quantity Demanded)/(%Change in Price) • To Calculate %Change in Quantity Demanded: • [Qdemand(new) - Qdemand(old)] / Qdemand(old) • To Calculate %Change in Price: • [Price(new) - Price(old)] / Price (old) • Price Elasticity deals in Absolute Values

Price Elasticity Practice • Consider the following figures. • Price Quantity Demanded $9 150 $10 110 What is the Price Elasticity of this Product?

Price Elasticity of Demand • PEoD = • (%Change in Quantity Demanded)/(%Change in Price) • To Calculate %Change in Quantity Demanded: • [Qdemand(new) - Qdemand(old)] / Qdemand(old) • To Calculate %Change in Price: • [Price(new) - Price(old)] / Price (old) ============================= Step 1: [110 - 150 = -40] / 150 = .26667 Step 2: [10 - 9 = 1] / 9 = .1111 Step 3: (-.26667) / (.1111) = -2.4005 Answer: 2.4005 is the Elasticity of this good.

Price Elasticity of Demand • * If PEoD > 1 then Demand is Price Elastic (Demand is sensitive to price changes) • * If PEoD < 1 then Demand is Price Inelastic (Demand is not sensitive to price changes)