Break Even Analysis

Break Even Analysis. Learning Outcomes. By the end of the lesson the students will; Understand the concept of break even analysis Identify the assumptions underlying simple break even Calculate the break even level of output and sales arithmetically Recognise the uses of simple break even.

Break Even Analysis

E N D

Presentation Transcript

Learning Outcomes By the end of the lesson the students will; • Understand the concept of break even analysis • Identify the assumptions underlying simple break even • Calculate the break even level of output and sales arithmetically • Recognise the uses of simple break even

Airbus A380 The Airbus ‘A380’ is the largest civil aircraft ever built. Designed to carry 555 passengers in a three class arrangement. It has one third more seating capacity than a Boeing 747 and is produced by a company called EADS.

Inside the Airbus • Model of a possible first class area. • A model of a bar area on the new airbus. • A model of an onboard duty free. • Other features will include; gymnasium, sleeper cabin, crèche, business centre and a casino.

Timeline of A380 • November 2000 – First A380 order received. Airbus says that it needs to sell 250 of them to break even. • March 2005 – Airbus admits that 270 aircraft needed to break even. • June 2006 – Deliveries delayed by 6 months. • 3 October 2006 – Another 18 month delay (airbus will lose £3.36 billion). • 19 October 2006 – Airbus need £40 billion worth of orders to break even. Break even point now at 420 aircraft only 159 on the books.

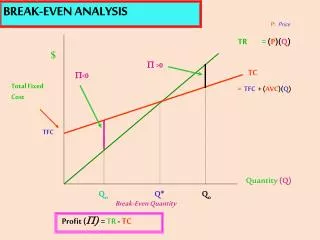

What is Break Even? • Break even analysis investigates the minimum output and sales that a company requires in order for its revenue to cover its costs. • At a zero level of output, the company will incur fixed costs (e.g. buildings and machinery) without any revenue from sales and so will make a loss. As the company begins to produce, it will incur variable costs (e.g. raw materials and wages), but it will also begin to receive revenue from sales. • Assumptions of break even analysis; • The selling price will remain the same regardless of the number of units sold. • Fixed costs remain the same regardless of the number of units of output. • Variable costs will vary in direct proportion to output.

Calculating Break Even To calculate break even the following formula is used; Break Even Output = Fixed Cost (£) Contribution Per Unit (£) Thus a product with a price of £12 and variable costs of £6 will contribute £6 for every unit sold. If fixed costs are £2,500, how many units will need to be sold to break even? Break Even Output = Fixed Cost Contribution Per Unit = 2,500 12-6 = 2,500 6 = 416.666 or 417 1.d.p